There is very little I am sure about in this market, except that the bull market in bonds is over. A lot of people disagree with this view - but that’s fine by me.

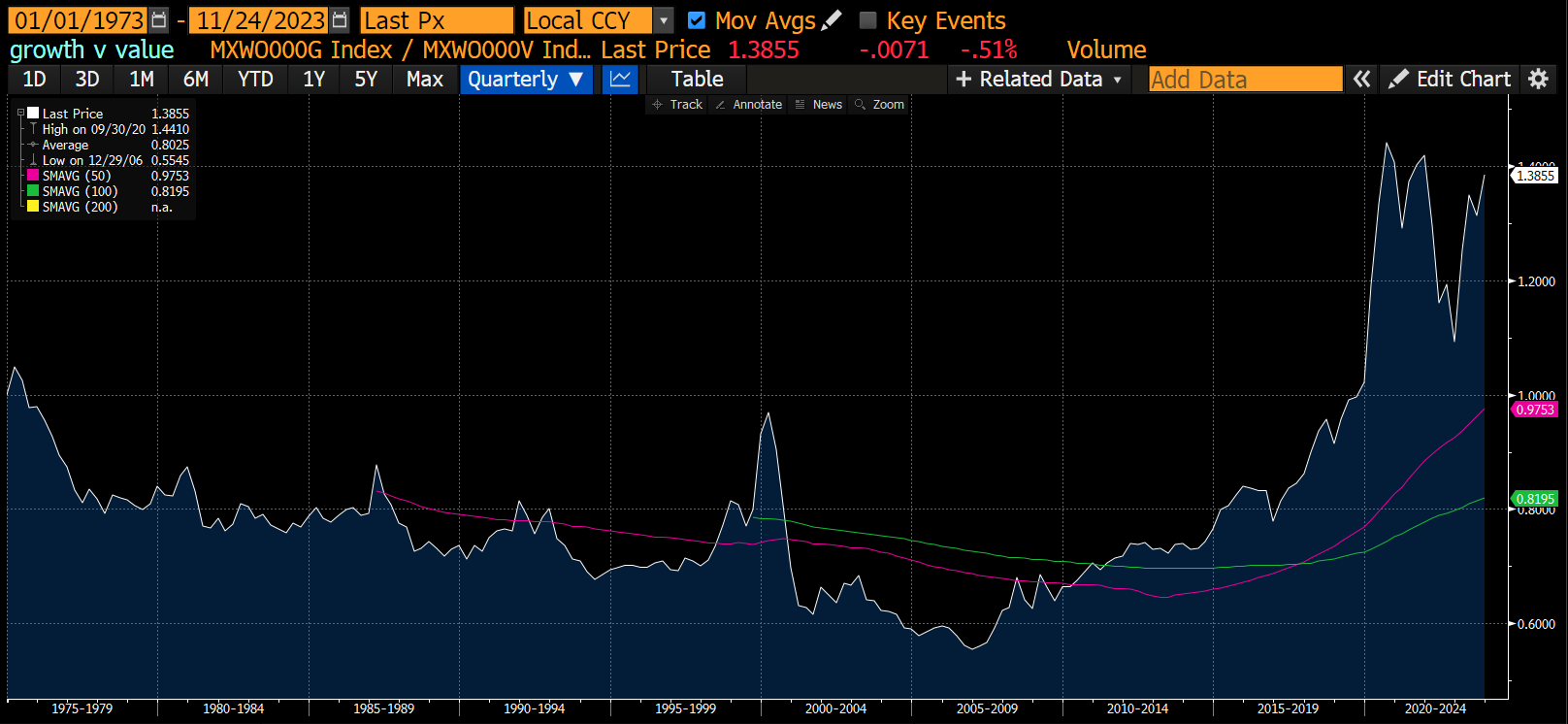

The “chat” from analysts and other market observers was that the change in bond markets, would herald a long awaited change in market leadership. I also thought this would be the case, but after threatening to happen in 2022, 2023 has seen the usual suspects outperform again. Using MSCI definitions, growth stocks continue to outperform value.

The chart above stuck me as odd, as I would have thought a fund like ARKK Innovation ETF was by definition a “growth” investor. But ARKK has not bounced.

MSCI definitions of growth versus value tend to use things like book value. One of the cheapest sectors in the US is banks, and as Michael Hartnett from BOA shows, they are at 80 year lows relative to the market.

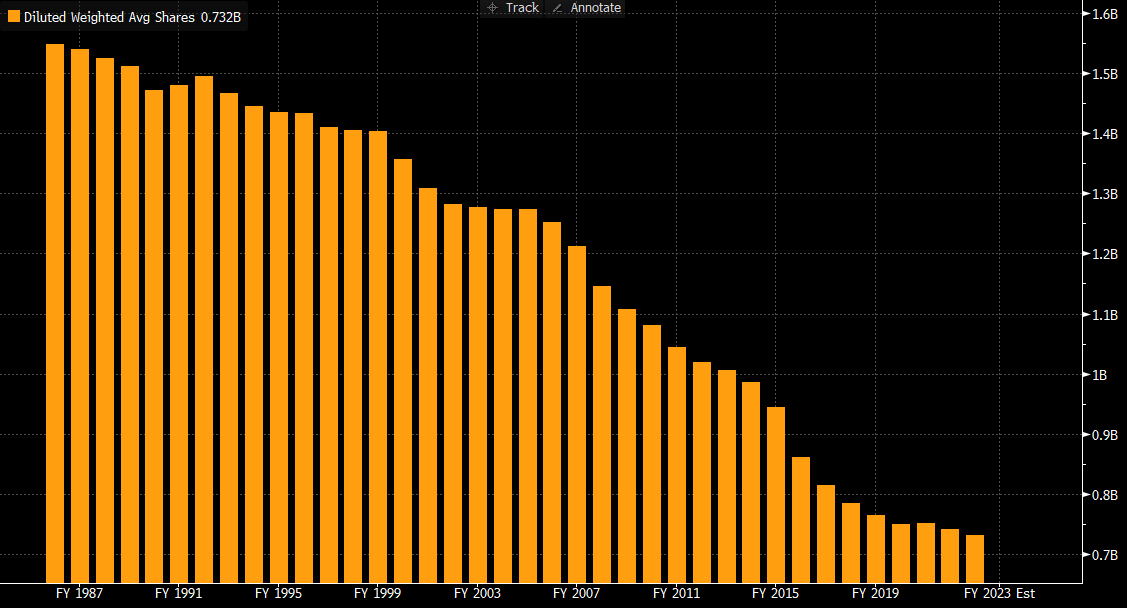

Why are banks so poor? Partly because they are forced to hold equity. Share buybacks are relatively rare among banks. But in the broader market, tech in particular, share buybacks are the norm. This is one of the big changes in markets over my investment career has been the transformation of equity markets from a place where capital is raised, to a place where capital is returned. The simplest way to show this is taking the market capitalisation of the the S&P 500 and dividing it by the price of the S&P 500. During the dot-com bubble companies generally sold shares, but in the 15 years since the GFC (with the exception of Covid) shares outstanding has fallen.

The main way that capital is returned is share buy backs. I had two concerns over share buy backs. The first is that in its extreme form, corporates would end up with negative equity. That is debt on the balance sheet far exceeded assets on the balance sheet. McDonald’s, for example, has gone from USD 15bn of equity in 2012, to negative USD 5bn today.

The decline in share out standing started in 1990s, but has accelerated in recent times. It is the acceleration of share buybacks that has driven the decline in equity.

McDonald’s has always been an investment grade borrower even with a much more geared up balance sheet. To simplify, I compare McDonald’s earning yield to US 10 year bond yield plus a 20% premium. In line with analysis on Apple and Microsoft, it did make sense to buy back shares aggressively from 2008 to 2022. But no longer. But just like in the early 1990s, the pace of buyback has slowed, but not reversed. My expectation that higher rates might expose a negative equity McDonald’s to downside risk has been proven wrong.

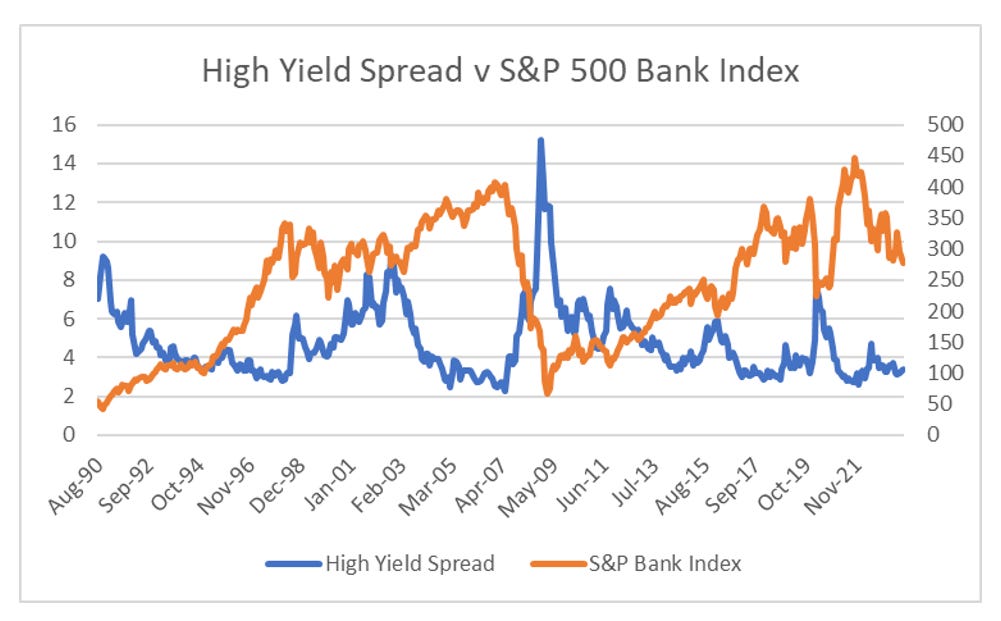

I am beginning to wonder if the disintermediation of banks, and particularly investment banks means that equity is no longer necessary for large corporates? Or to put in in other words, having banks at the centre of the financial system meant that other participants also needed equity. I am going to refer to my work on clearinghouses, please go here if you want to know more about clearinghouses. Pre GFC, clearinghouses were participants in financial markets, but they were not the main players. Banks much preferred to trade with each other, as it was cheaper, and clearinghouses were given the leftovers. In practice this meant if banks were doing badly, then credit would also do badly. Looking at the S&P Bank Index versus high yield spreads, you can see that falling spreads and bank equity performing well were, and when spreads widened, banks did badly. In 2022 and 2023 banks have been poor, but spreads have barely moved. Why?

Post the GFC, clearinghouses were pushed to the centre of the financial system. This has created a host of other problems, but solved the problem regulators wanted solve, which was having financial problems at banks become problem for the economy. The performance of the Nasdaq in the face of the bankruptcy of SVB probably marks a success for the reform.

Even JP Morgan could not compete with the volumes that major clearinghouses now complete.

Clearinghouses are platforms with government mandated businesses. Unlike banks, which lend and can take losses, and stop intermediating in markets, clearinghouses are only concerned with liquidity. When losses do occur - their losses are very limited (see my clearinghouse work for more detail). Clearinghouses have very serious problems, but as we have seen central banks are happy to provide market liquidity when necessary. The UK bond market (Gilts) is a recent example. LME and nickel is another.

What this implies to me is that large multinationals, which are overwhelming listed in the US, have largely escaped the confines of the international banking markets. By issuing corporate bonds, they can access capital readily, and with the assurance that governments will always provide liquidity via clearinghouses. I can understand why governments have embraced this strategy, as after the GFC and Eurocrisis, voters did not want any more recessions. Voters now want more equality, rising wages and less corporate friendly policies seem a given to me. Smart corporates might want to start building equity again, but that’s just my view.