Generally speaking the fund management community thinks of the dot com boom and the housing bull markets as “bubbles”. Looking at US net worth to GDP, the dot com bubble say net worth to GDP rise form 375% to 450% from 1995 to 2000. And the housing bubble saw it rise from 400% to 475% of GDP. This current cycle has seen “the bubble” rise from 400% to 600% and is till at 560%. With US equities back at all time highs, hard to argue that “the bubble” has burst.

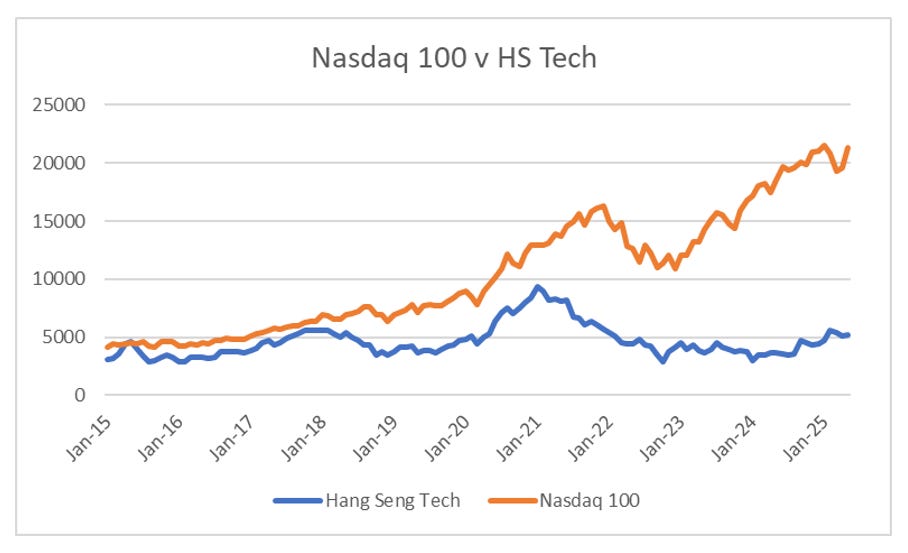

The top of the dot com bubble saw gold outperform the Nasdaq. Something that started to happen this year. If you were thinking in terms of a “tech bubble” there have been plenty of reasons to think we were at the top. When Chinese tech stocks got regulated to low growth in 2021, I assumed a similar outcome awaited US stocks. This has not happened.

When Deepseek came out with a low cost AI agent, I thought the whole AI stack would need to reprice lower. Nvidia weakened for a while, but has now touched all time highs again.

When I read about Mark Zuckerberg doing a USD14bn aquihire I think we must be near a top of a bubble. But I thought similar things when he bought WhatsApp for USD 18bn - which now looks like a bargain.

What I think all of this has in common is the ever widening power of the Silicon Valley idea of blitzscaling. While Amazon is a powerful example of the power of growing rapidly first, and profits later, from an investing perspective, Softbank is another great example. Masayoshi Son only wanted companies to grow rapidly. The 99% market value lost from 2000 to 2002 did not dissuade him from this style.

The question I am asking myself is that every corporate and every investor now understands the blitzscaling methods. Palantir on 107 EV/Sales is not a bubble, but the huge losses it racked up, and the building of product that can rapidly rolled out to the US government is intensely valuable. There is also a reflexive nature to the blitzscaling model. The company with the largest market capitalisation is most likely to be able to invest the most to capture the most market share in the future.

This is where the Blitzscaling ideology gets hard for me. When I look at the cloud/data centre area, I can find plenty of stocks indicating that there is a potential overbuild coming. Equinix is a data centre REIT - and has highlighted slower growth in the short term. Stock is down 20% this year.

But on the other hand, newly listed CoreWeave which is building even more data centres has quadrupled from its listing in March. Which one is correct? Or has the market decided they want CoreWeave to be the blitzscaler here and realise hyper growth using its shares as a currency for growth? Its potential acquisition of Core Scientific would underscore this idea.

What I am trying to say, is that talk of a bubble is probably wrong. The huge dislocation between “growth” and “value” stocks reflects corporates and investors pricing in the success of blitzscaling. The trend change in growth versus value investing has been profound. And betting against this has been largely career ending.

One of the features of the blitzscaler model is that the amounts being invested into new areas has soared. Mark Zuckerberg is throwing large amounts of money at catching up in AI. Google which is very exposed to a potential shift to Chat GPT and other AI systems is spending even more. As far as I can tell Open AI does not make money, and given the appearance of DeepSeek, is not likely to in the short to medium term. But what we can see with Nvidia share price, this has not stopped ever increasing levels of Capex. As Amazon or Tesla has showed investors - you need to be with the growing and investing company no matter what. So where does it end? Well in China it ended with government regulations to reduce the pricing and market power of the leading tech companies. In many ways this is similar to the US government acting against Microsoft during the first dot com boom.

I used to think increased competition and falling prices would end this investing model. But on that basis I would need to be short Tesla, which is still priced as growth stock, even as sales growth has slowed and margins have fallen, and Chinese competitors like NEO have been destroyed. Tesla has not been a short.

Where does that leave me? Well away from the “blitzscaling” companies - markets have behaved much as I thought they would. Higher interest rates have acted as a weight on valuations and earnings. Blitzscalers however continue on their merry way. Spotify certainly now trades as the dominant stock in its area.

Companies like Uber and DoorDash, that seemed likely to suffer margin pressure from higher wage costs have both soared this year, even as near competitors (Lyft and Delivery Hero) have languished. A sign that the blitzscaling model has triumphed in this area as well. Blitzscaling is a problem for my style of investing - as I tended to like an industry, rather than trying to pick one stock. I would take weakness in Nio, Lyft, Delivery Hero as signs of problems in the industry - when in fact, it was a signal to buy the leader. The logic of this is that perhaps the Nasdaq is now the risk free asset - as the component stocks are now economically and politically untouchable blitzscalers. I launched Brumby Capital because I thought a pro-labour move in politics would be inflationary, which would put pressure on interest rates to move higher, and this would put pressure on equities. The beginning of 2025 saw a strong move higher in gold/nasdaq - but as of today, it has probably reversed half the move, and near the 200 MDA.

The problem with investing in the blitzscalers here is entirely political as I can not find a problem with their business models. The create a lot of share holder value, but relatively little taxation revenue. This continues to reduce the tax base, while adding to wealth inequality. China acted against this, and there is little question that the Chinese Community Party is in charge. There generally also seems to be far more competition in the Chinese tech space - which is leading to far more competitively priced tech. More competitive tech space, and lower prices has seen a huge gap open up between US and Chinese bond yields. At what point does the concentration of wealth in blitzscalers become a political problem? It seems inevitable to me - but timing is a key issue.

Blitzscaling being inflationary makes sense to me. The blitzscaler model is deflationary to start with, but once dominance is established, prices rise radically, and effective competition is virtually eradicated. For me, this is a “MARKET” problem if gold is outperforming stocks - and not a problem when stocks are outperforming gold. Given the bounce back in stocks - we stand again at a precipice. 2025 looked like a top to me - but perhaps we need an even more extreme move. On current trends, we should know which way the political wind is blowing soon.