I am going to talk about McDonald’s which I thought looked a good short about 10% lower than where it is today. But before that, just a quick explanation for the slightly different format. I am about to enter the karting season, which means I will be on the road with my oldest son a lot more. It will be much easier for me to do this on an iPad rather than lugging my laptop everywhere. So this is my first effort to see if I can produce a decent post via laptop and mobile exclusively. Please do comment on any problems you find with this post.

McDonalds. There is a paid post that goes into detail why I like McDonalds as a short (full disclosure - I am short). As a rule, I do not like being short stocks that have taken out all time highs. One of the first trading rules any fund manager learns is that strength should be bought, and weakness sold.

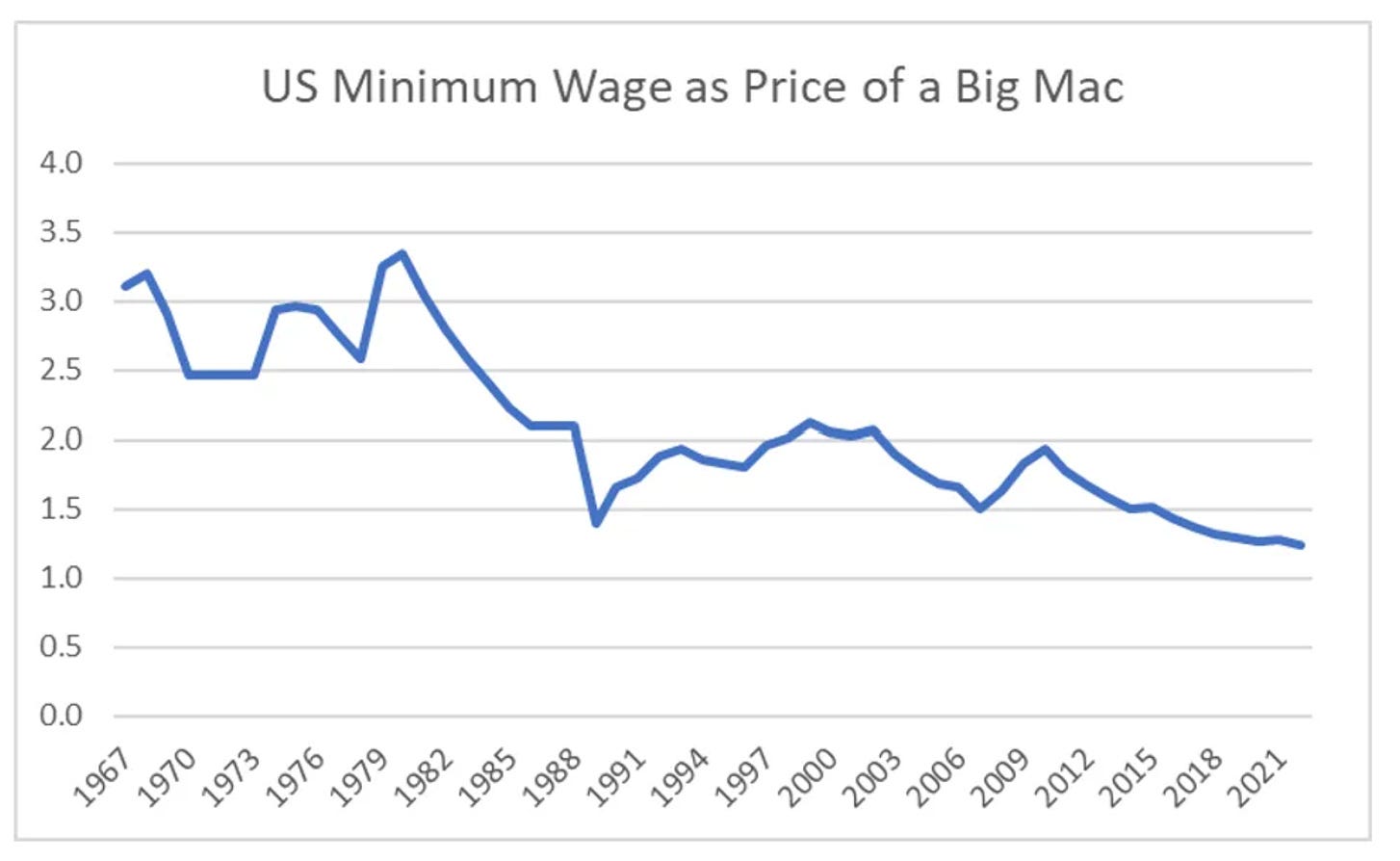

There is a lot more detail on why I want to short McDonalds - and you can see it at the “What to Short Sell - Part 3”. But one key part is that US wages (as proxied by minimum wages) has not kept up with the price of a Big Mac. My belief is that this is turning higher, and that fast food chains are entering a period of structural decline.

There is plenty of evidence that this is indeed playing out. McDonalds for years had very good relations with its franchisees, but in recent years it has moved to a move aggressive profit seeking behaviour.

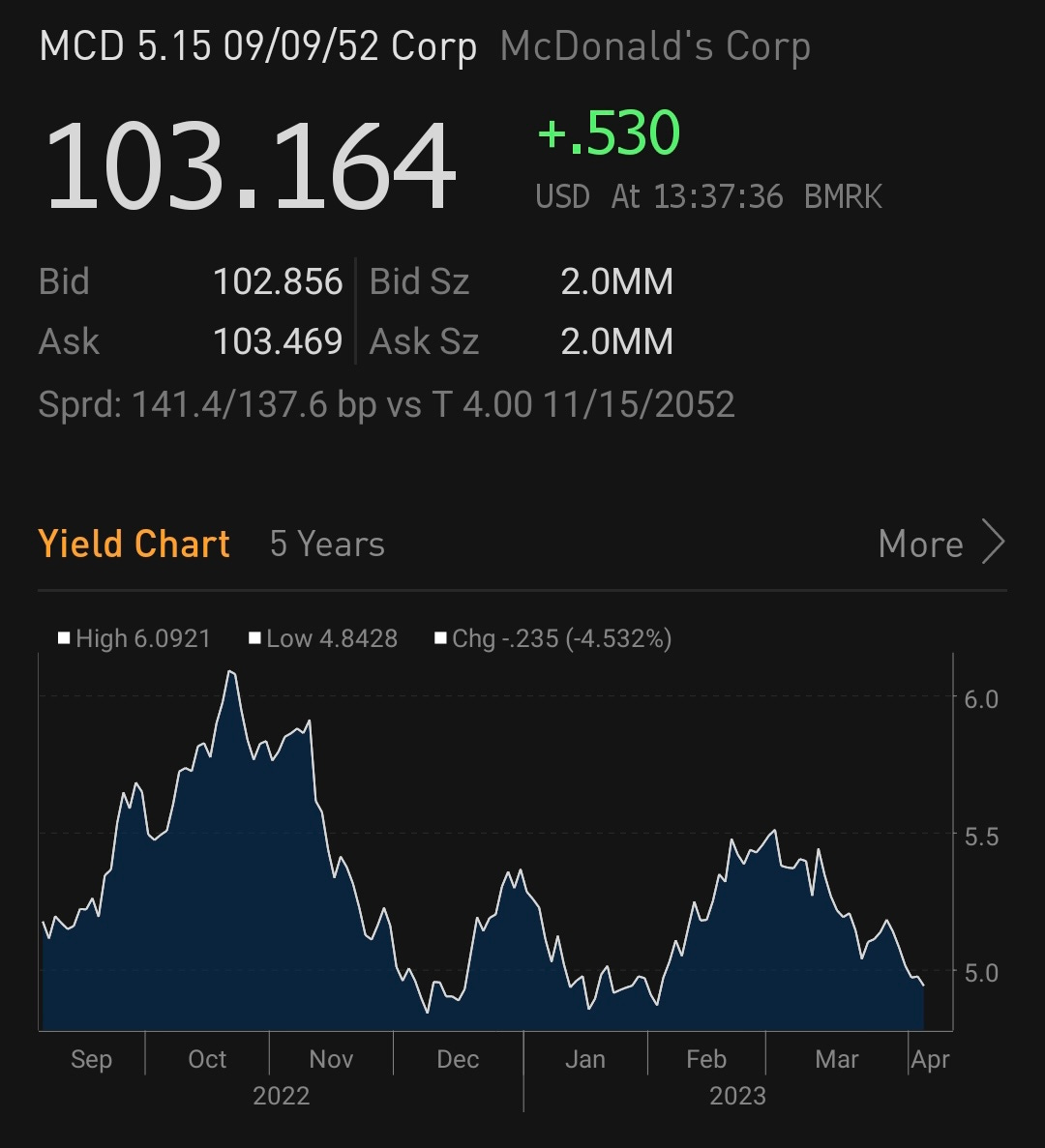

This week has also seen McDonalds announce layoffs, at the corporate level rather than at franchisee level. All of this would seem a business that has a few problems, and yet it trades at all time highs. When a stock does not fall on bad news, this normally means it’s a buy. So what is going well for McDonalds? A rally in the bond market and compression in spreads has seen the McDonalds 30year bond fall from 6% late last year to 5% today. Given that McDonalds aggressively buys back stock - this is very supportive of its equity valuation.

The McDonalds corp as it is currently structured is not affected by the profitability (or lack thereof) of its franchisees. In fact, it is deliberately structured to benefit from sales growth, not profit growth. In an inflationary environment, this makes McDonald’s very attractive. The core of the short idea is that politicians and regulators will seek to “share the pain” of franchisees with McDonald’s corporation. After recent bail out of Silicon Valley Bank corporate depositors, and various shenanigans at clearinghouses, I have my doubts that regulators even know how to punish corporates anymore.

So what to do? Well the two trading rules mentioned above, would tell me to cover the position. But I have one rule that I have yet to mention. If a position if going against you, but the portfolio as a whole is making money, then be patient. I have many inflation trades held against my short book, which are working surprisingly well. The idea was that if US regulators and politicians continue to bail out Wall Street, then inflation would rear its head again. And so far, so true.

Ironically, a collapsing McDonald’s share price would make me much more optimistic about the US, as it would show a political system that is still capable of acting in the interests of the majority, rather than the few. I still have hope that the US can turn things around - so I will hold on a for a bit longer. But this really is hope winning out over experience.