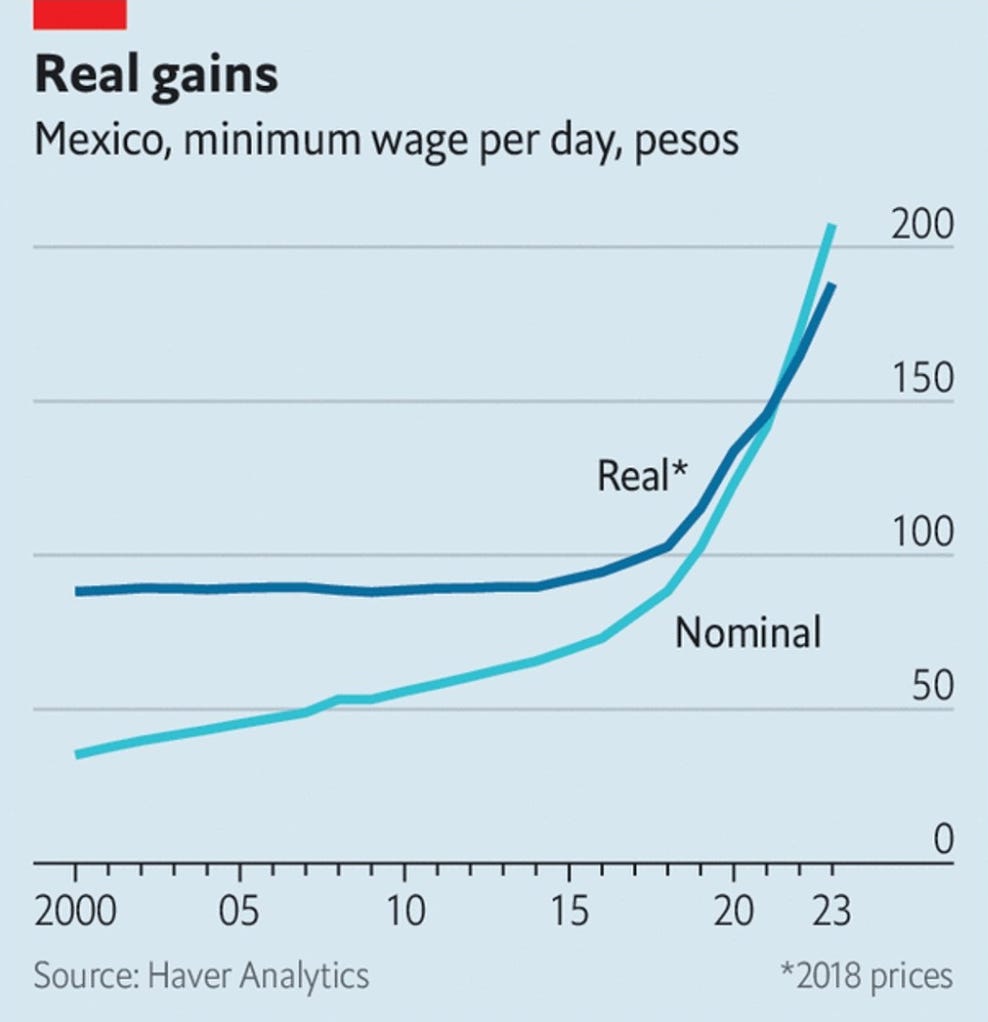

One of the core ideas of a pro-labour world is that governments are now in the position to raise real wages if they so choose. Tariffs, protectionist policies, capital controls, are all back on the policy table. Both China and the US use these policies, so there is no reason why anyone else cannot. In December 2018, Mexico elected Andrés Manuel López Obrador as president. The change in real wages in Mexico under his presidency has been staggering.

Without question Mexico has benefited from the US-China trade war. Mexican exports have surged since Covid.

Despite surging real wages, Mexico has kept inflation under control. The most recent reading of 4.3% is well within some of the lowest readings seen in modern Mexican history.

But to generate real wage growth, you need a strong currency. And for that you need a hawkish central bank. In Mexico, interest rates have risen to over 11%, the highest level since 2000.

But in 2000, Mexican interest rates rose to try and keep the currency stable. In 2023, Mexican interest rates are increasing even as the currency strengthens.

So a strong currency, with rising wages and high interest rates would be negative for profits, but this would be countered by decent economic growth, and rising top line. I assumed this would lead to a stagnant stock market. Which is pretty much what we see.

In contrast Japanese wages have only just recovered to 2008 levels in yen terms

In USD terms, Japanese workers are at new lows, with yearly wages at roughly USD 26,000.

The big difference being that the BOJ continues to run negative interest rates policy, and a weak yen policy. In contrast to Mexico, we would expect the Japanese stock market to be surging. This is what we see.

Japanese policies seem even more extreme when compared to near neighbour South Korea. South Korea like Mexico has been raising the minimum wage.

And to defend the currency has raised interest rates.

Which has led the stock market, Kospi, to be stagnant, just like Mexico.

If Korea has also moved to definitive pro-labour policies do we see any other macro changes? Well for one thing, South Korean holding of US treasuries are starting to fall.

One of the interesting take away from this analysis is that if Japan did enact real pro-inflation policies - like raising minimum wages, or strengthening unions power, the implication would be a strong Yen and stagnant stock market, but rising yields. I wonder if Japanese politics has the capacity to surprise just at the UK surprised the world with Brexit, and the US surprised the world with Trump?