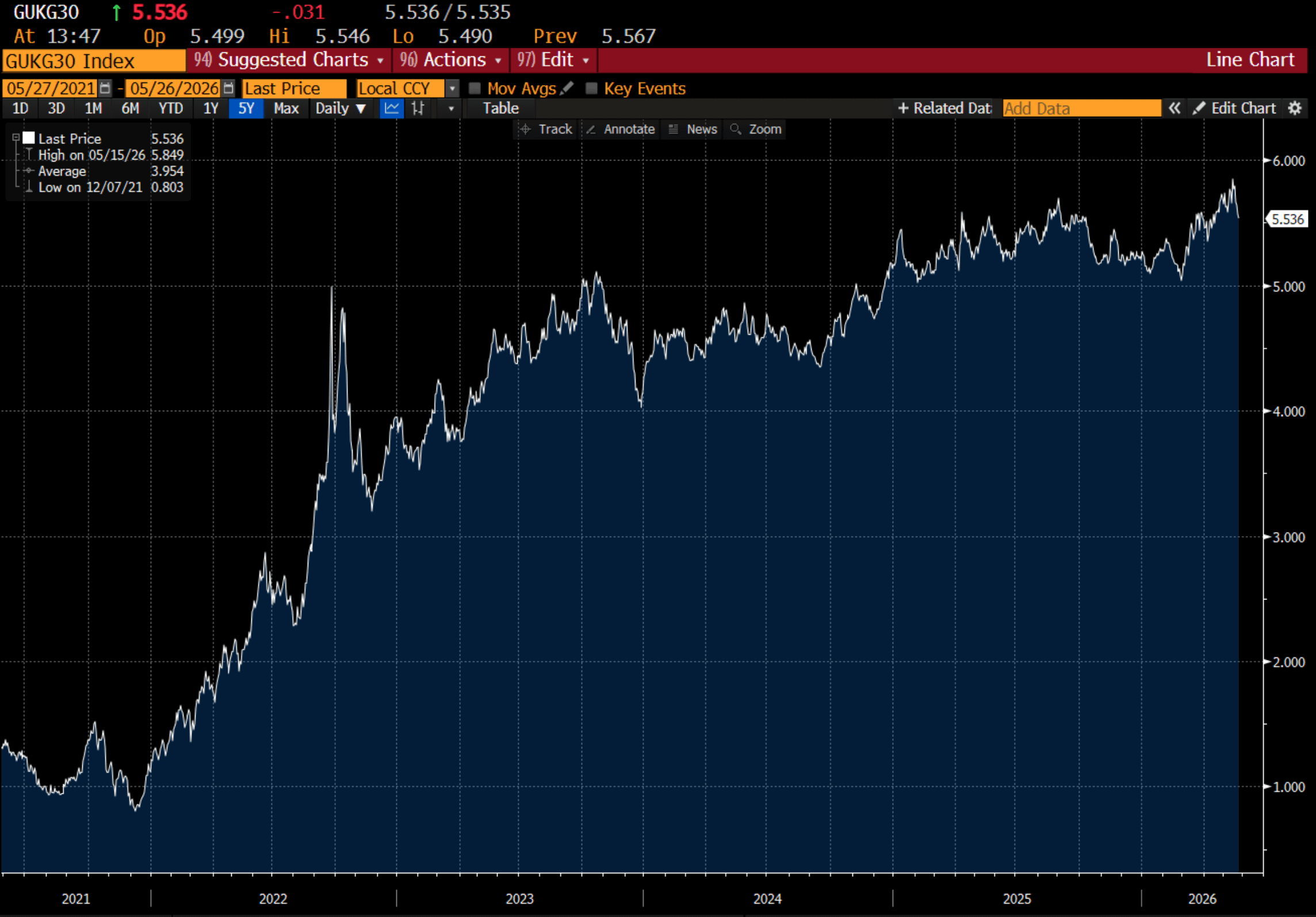

The original thinking behind the Pro-Labour trade was that politicians everywhere were being forced to address imbalances in the economy. The main one was sky high property prices. After the GFC, another property crash was off the political cards more or less. This left politicians with only one choice, raise wages while keeping property prices flat in nominal terms. This issue, as I saw it, was that rising wages would have an upward bias on property prices, so yields would have to be quite high to keep property in check. In the UK, 30 year bonds yields have indeed risen substantially.

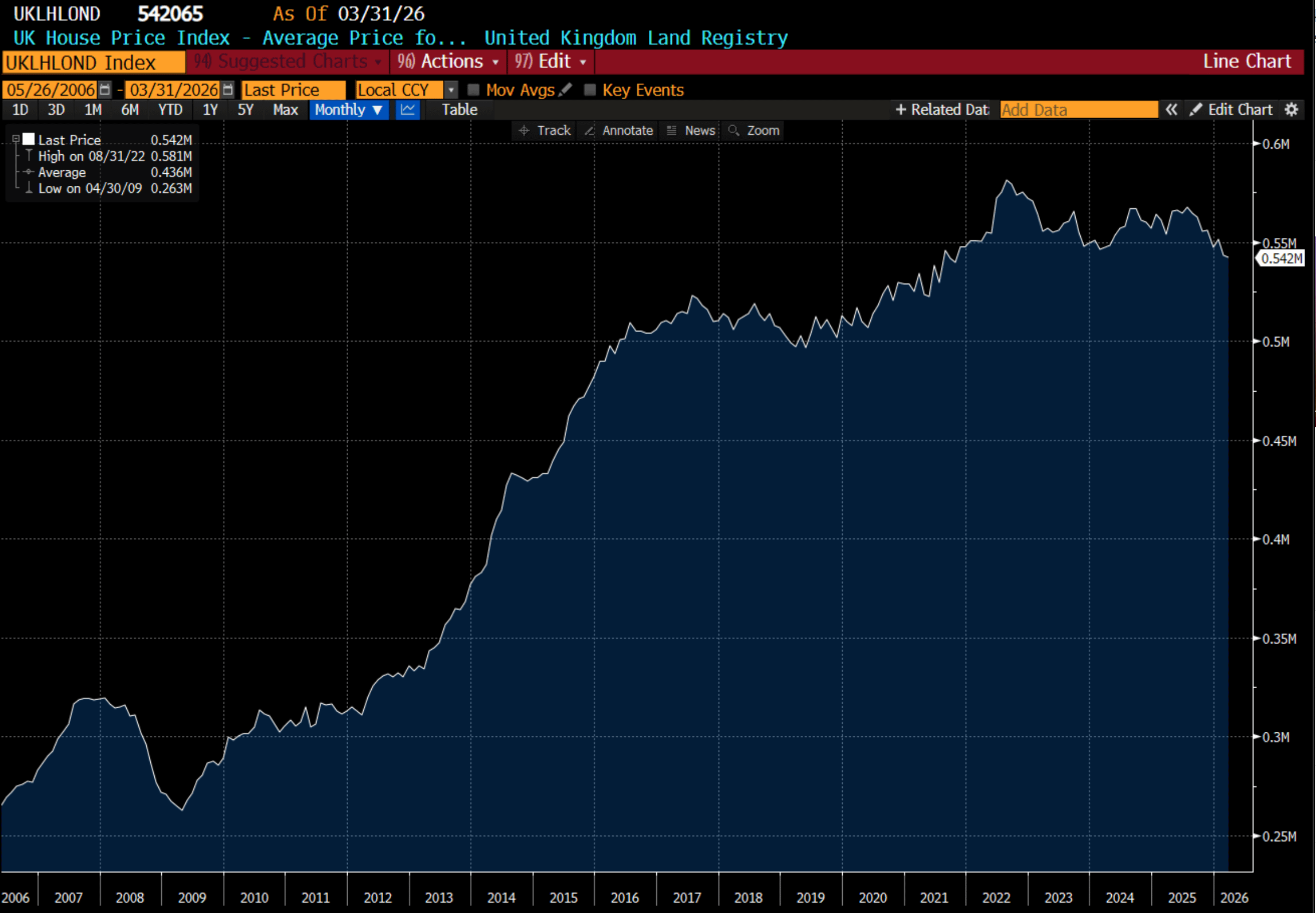

And London house prices have stagnated.

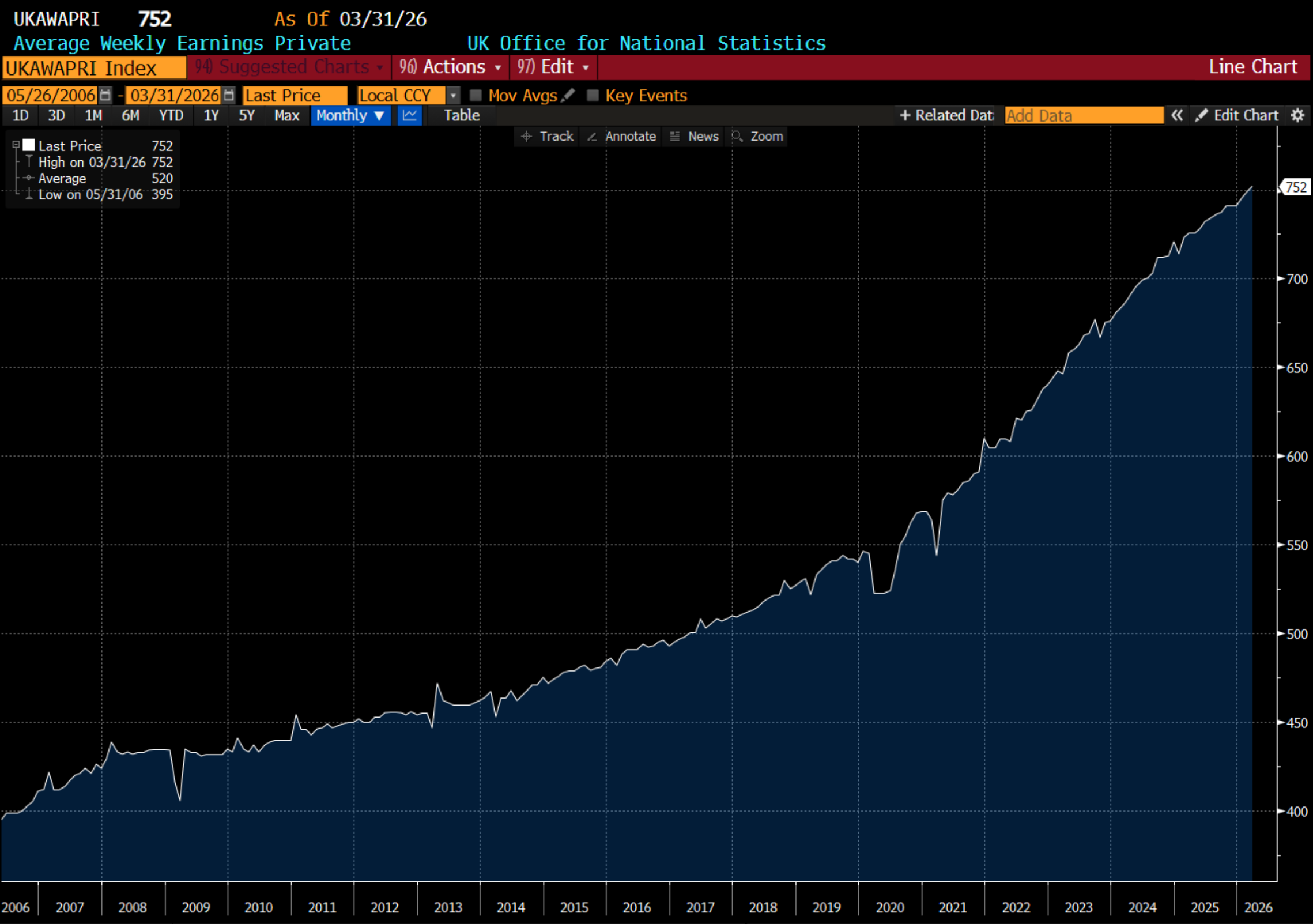

And UK wages have surged.

Broadly speaking, this has generally been repeated across the western world. I also assumed private equity would struggle in this world of higher wages and higher interest rates. The Invesco Global Private Equity fund has confirmed that view.

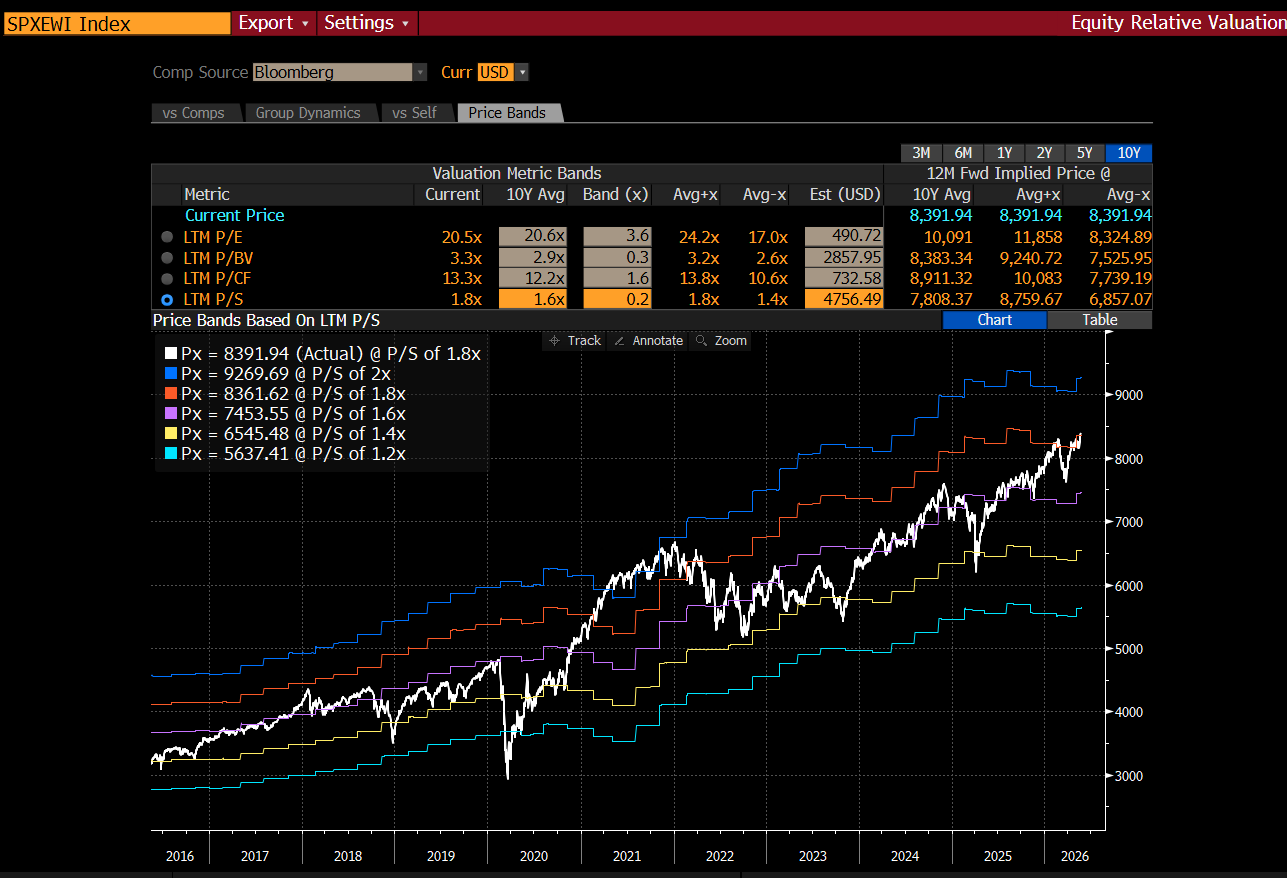

So far so good. I had assumed that higher yields would also put a dampener on equity valuations, like we saw in 2022. On this matter, I could not be more wrong. Using price to sales as a valuation metric, stocks have gotten more expensive, not cheaper.

If you use an equal weight index, you could maybe argue there has been a slight de-rating, but it is pretty flimsy.

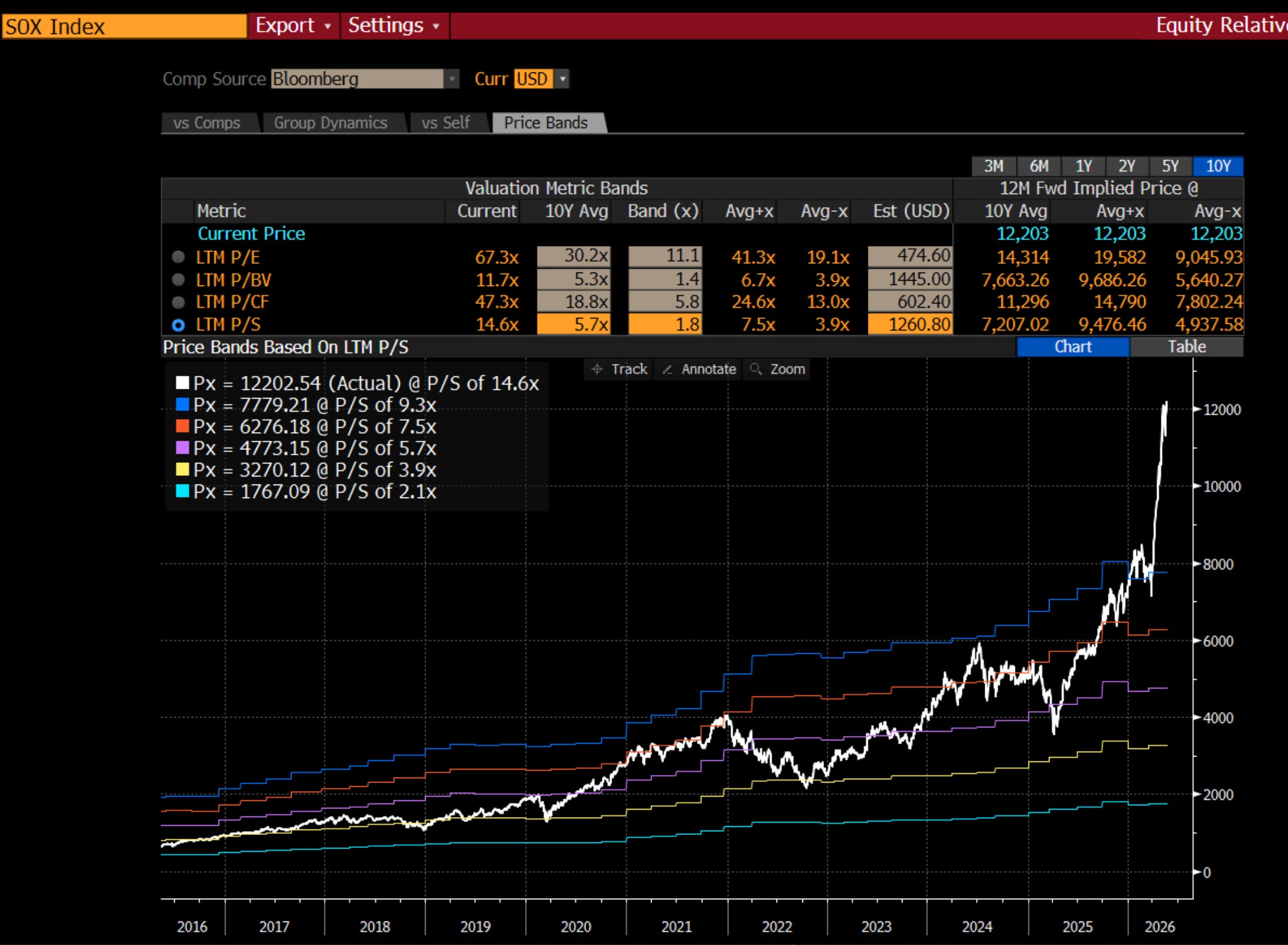

The place to be has been semiconductors. If dominates both the S&P 500 and momentum indices.

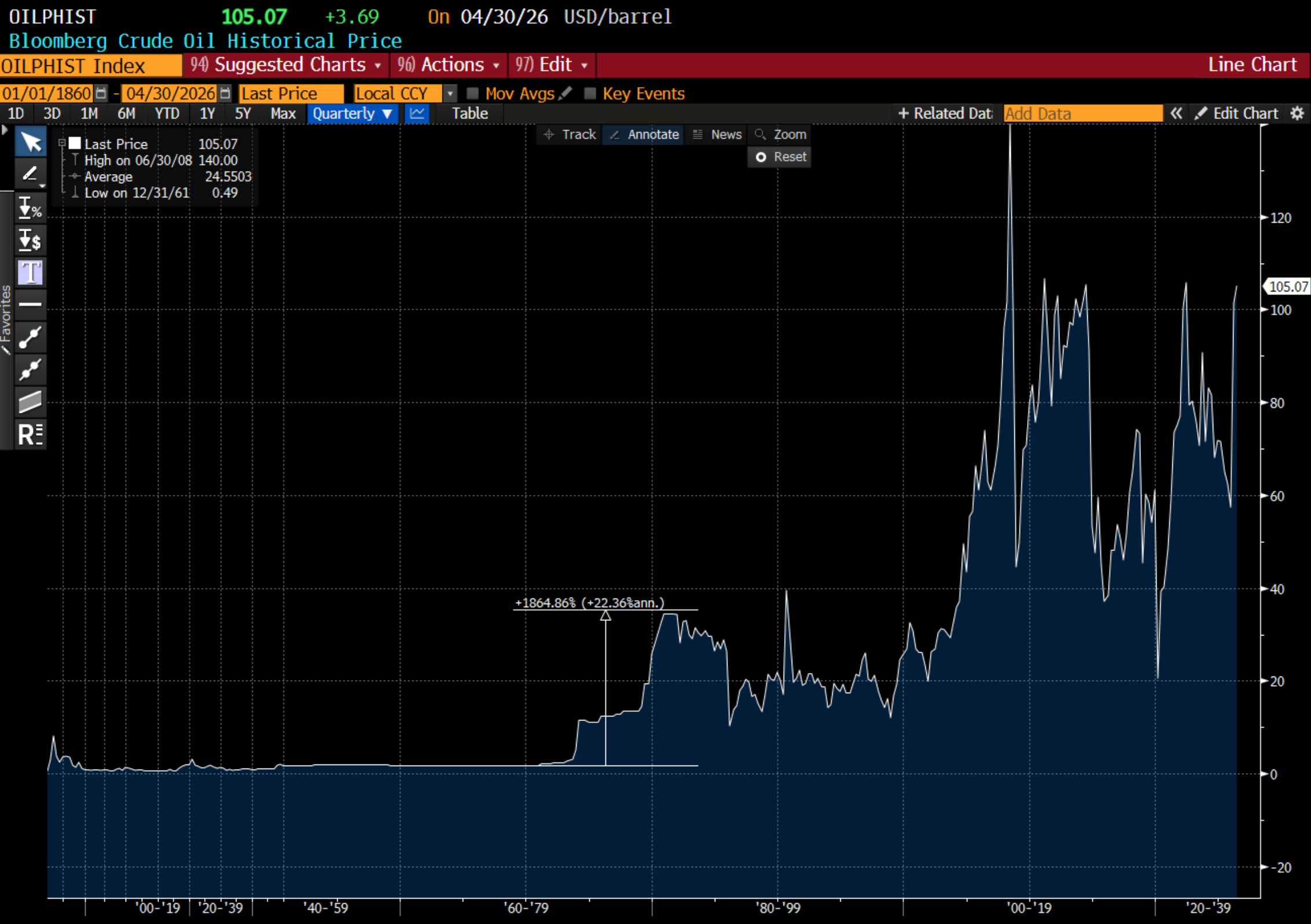

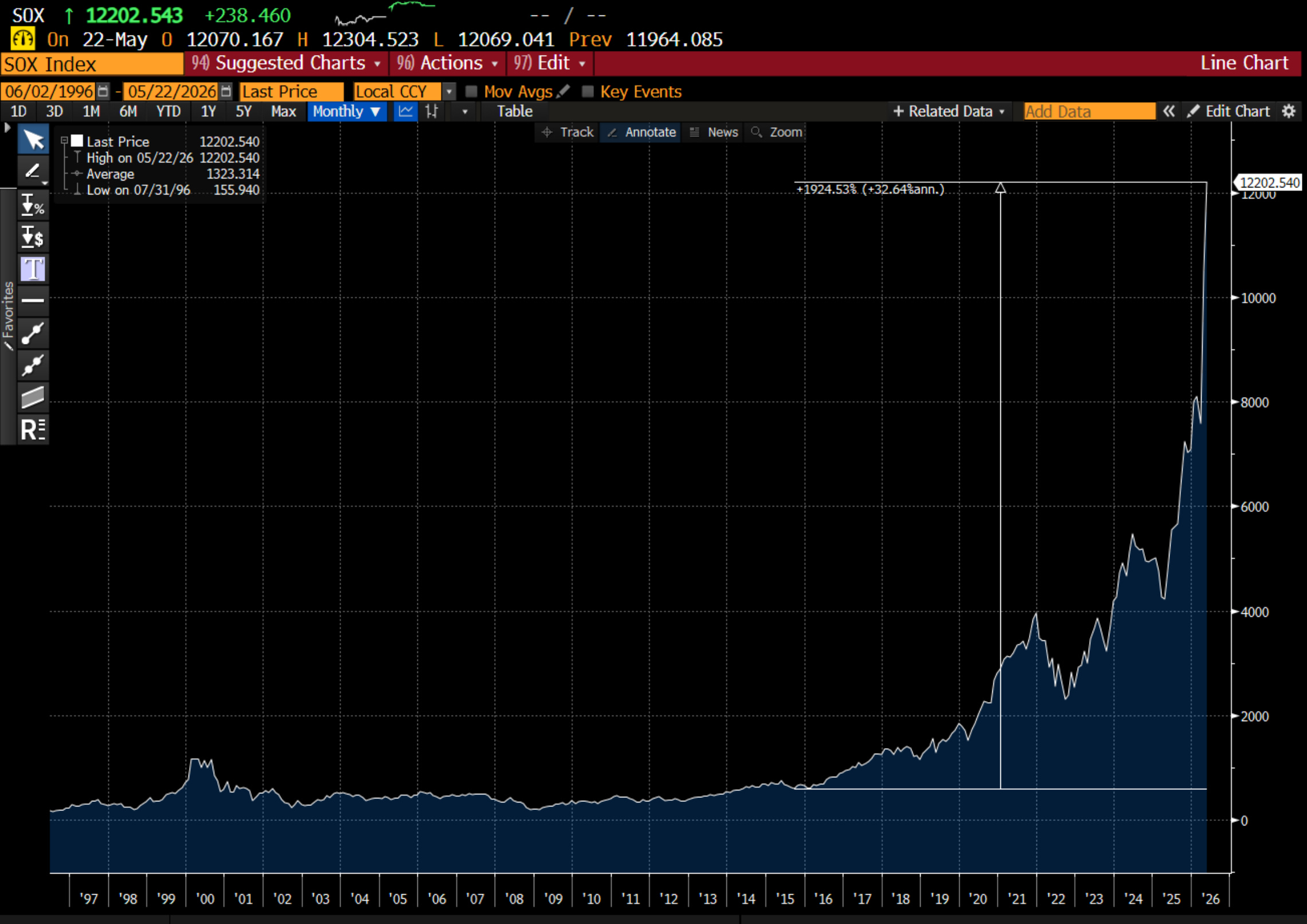

Weirdly, AI almost now makes a direct connection between wages and semiconductor prices. The higher wages go, the more corporates are incentivised to use compute, rather than labour. Whereas oil was the substitute for labour (or oil prices moved with rising wages) in the 1970s, semis now seem the substitutes for labour in 2020s. Oil rose 1800% during this era, as the market worked out the “right” price for oil.

Semiconductors have done even better than that.

If the analogy between oil and semis hold, then the market breaks only when politicians decided that rising unemployment to break inflation is a political winner. I don’t know when that is.