For various reasons I have been having discussions about gates. A gate for an investment fund is pretty common these days - as it seen as a way to protect investors from themselves. It is so common that is just usually added into many investment fund articles. Personally, I hate gates. I have on occasions had opportunities to impose gates, and have turned them down. When I took over the management of the Horseman Global fund, we had redemptions of well over 80% of assets - but chose not to gate. The only time I can think a gate might make sense maybe in time of total crisis, like GFC or Covid, when there is no liquidity anywhere - but even then your investors will likely have other concerns so a gate makes little sense. But gates tend to be standard parts of most funds these days - but my advice is for most fund managers to be extremely cautious in using them.

In the midst of the on/off war in Iran, and an epic AI boom, and all sorts of other shenanigans, you may have forgotten that private credit funds have been gating their clients.

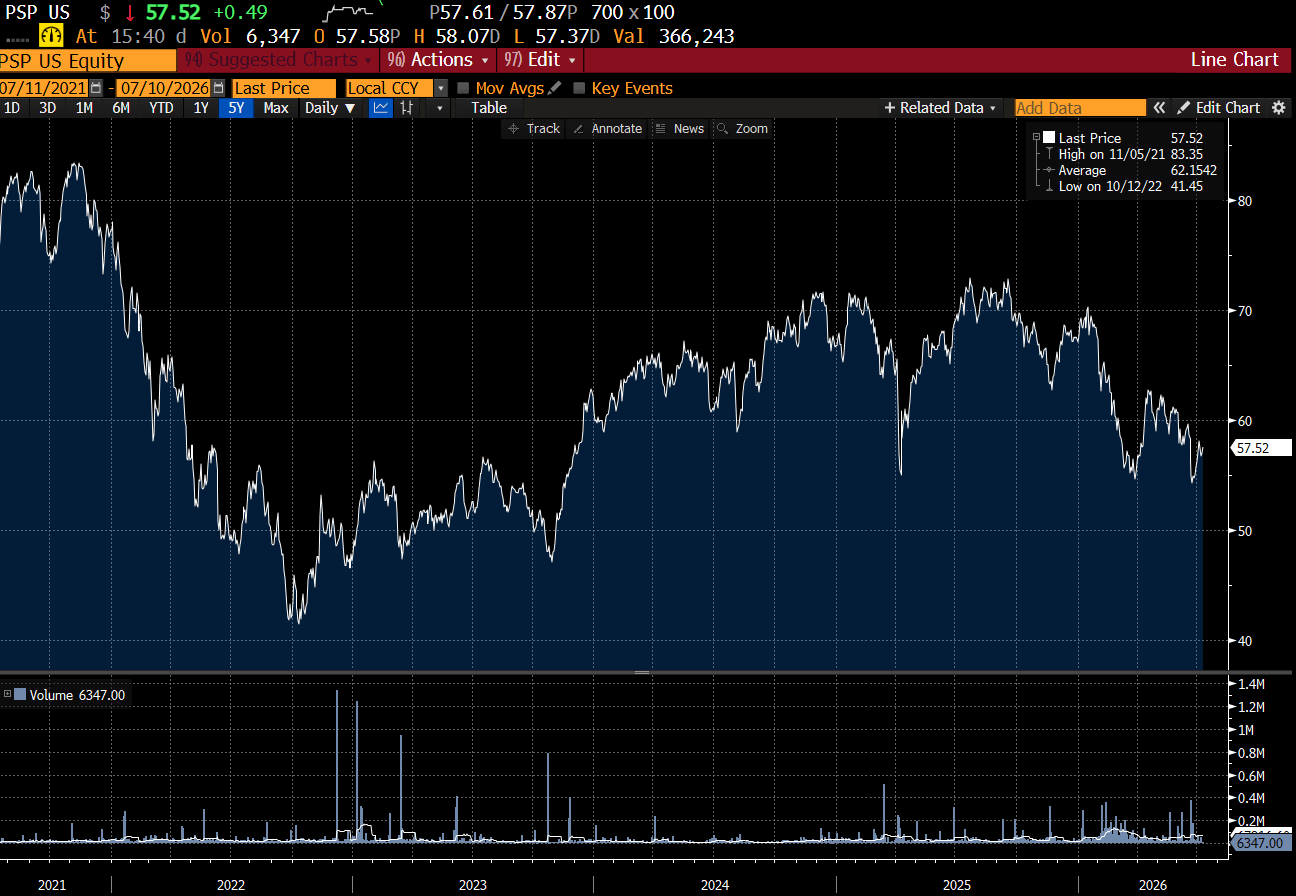

And this gating has been why the Invesco Listed Private Equity ETF (PSP US) (many private equity firms do private credit as well) has been poor on both an absolute and relative basis.

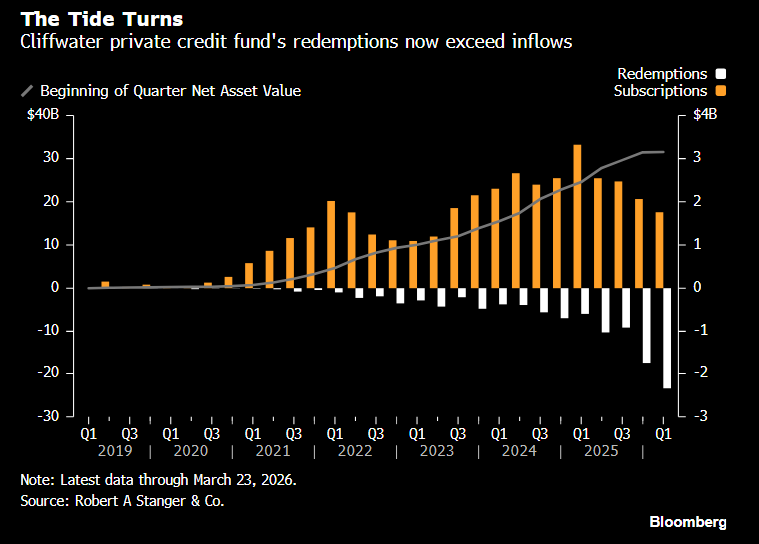

For me, once you gate a fund, it pretty much a dead product. Fund management is a trust game - and if people want their money back you should give it to them. And once you gate, you create terrible incentives for other investors. Gating means or implies you have a bunch of assets that cannot be priced or sold. And for investors who have not asked to redeem, they start asking themselves some difficult questions. Will the fund manager have to sell the liquid positions to meet redemptions, leaving the fund only with illiquid assets? The answer is almost certainly yes in my experience. And does anyone want to then invest into this fund, with only illiquid assets that cannot be priced? Not really. Cliffwater is a good example of this phenomenon.

And with more money going out that coming in - you would wonder if that NAV is correct.

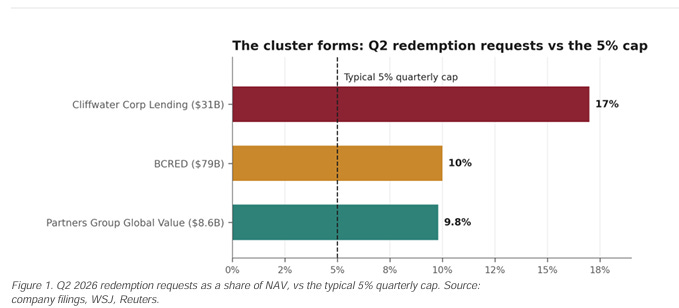

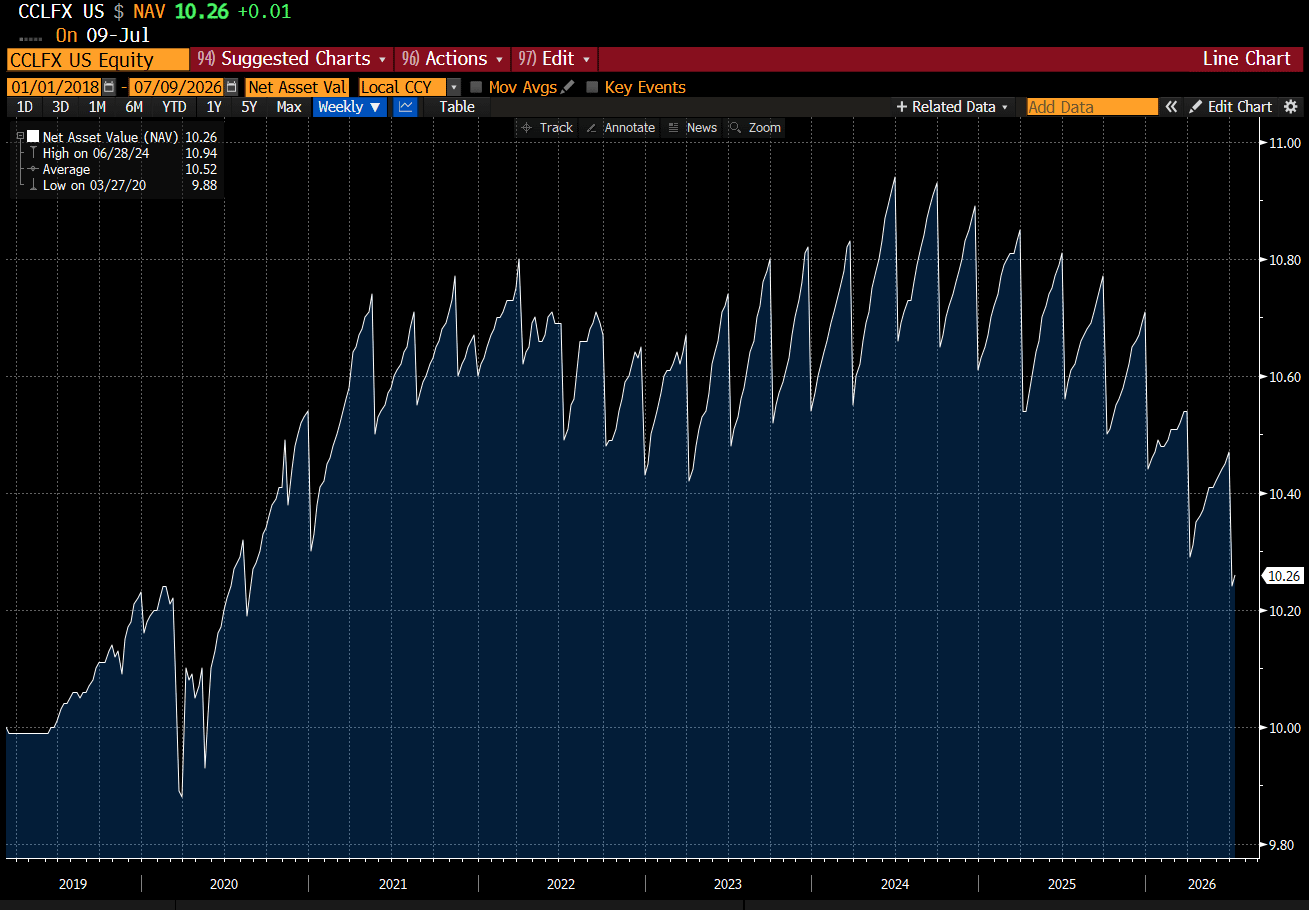

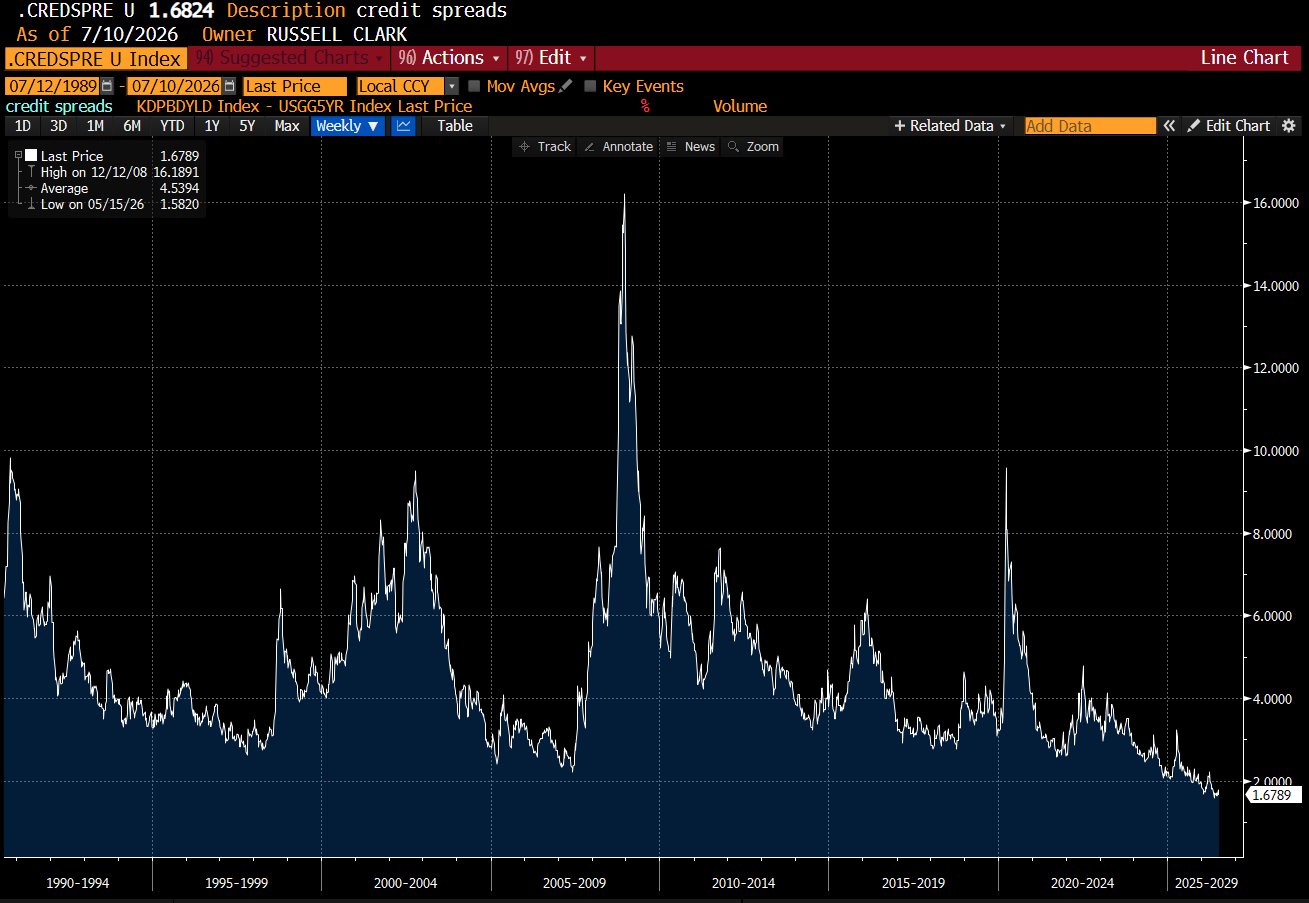

Cliffwater has capped redemption at 5% of assets, despite have 17% redemptions. Following the logic laid out above, this looks to be a dead product. Who would put money in this now? The one thing I find very odd about this is that Cliffwater is getting into trouble when high yield spreads are at all time lows.

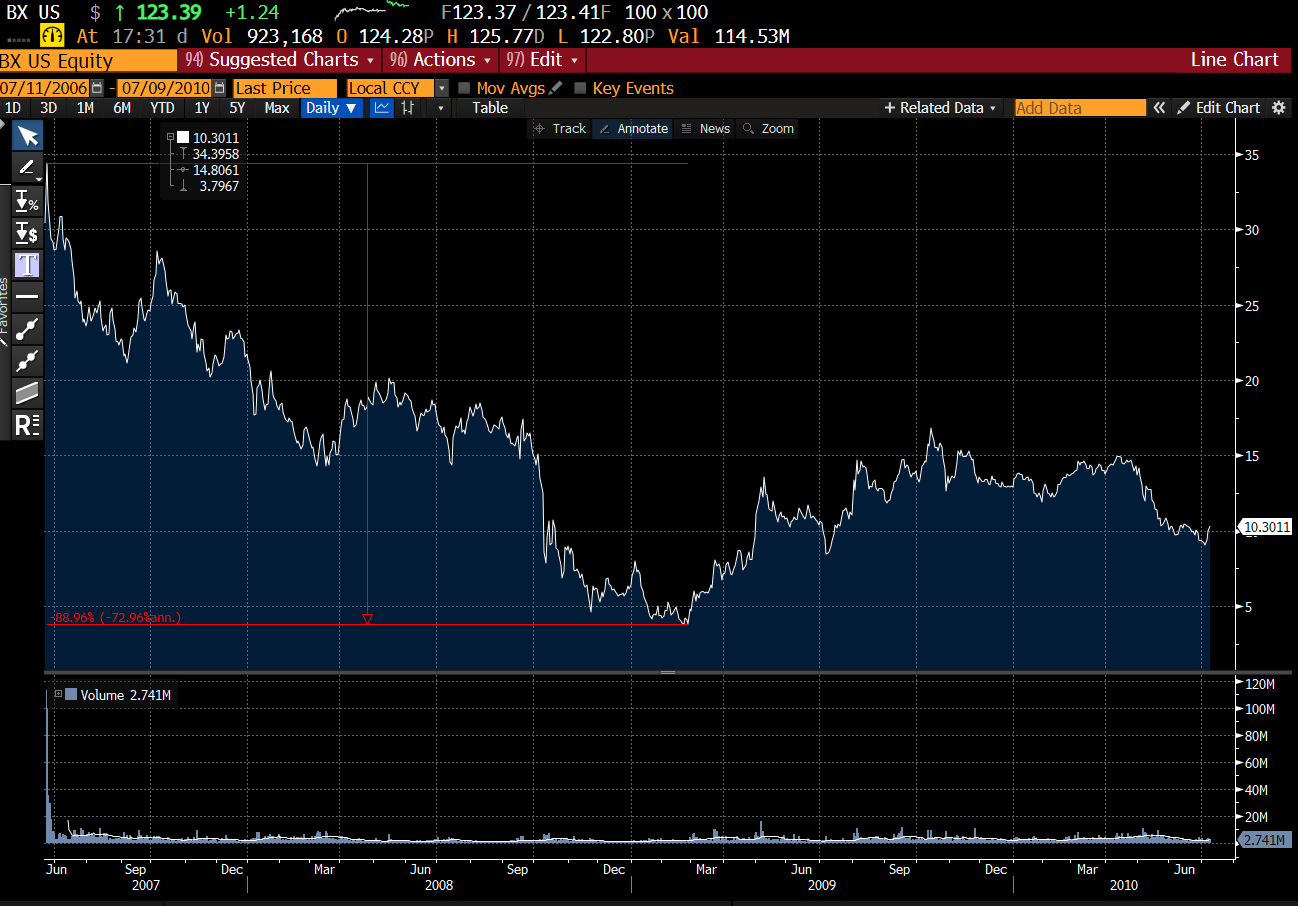

For reference - Blackstone listed in 2007, just before credit spreads blew out - and fell 90%.

One wonders what private credit would actually do in a recession?!?

Anyway, the point of this notes are gates are bad, and there is almost never a good reason to use one, and using one will likely make a bad situation worse.