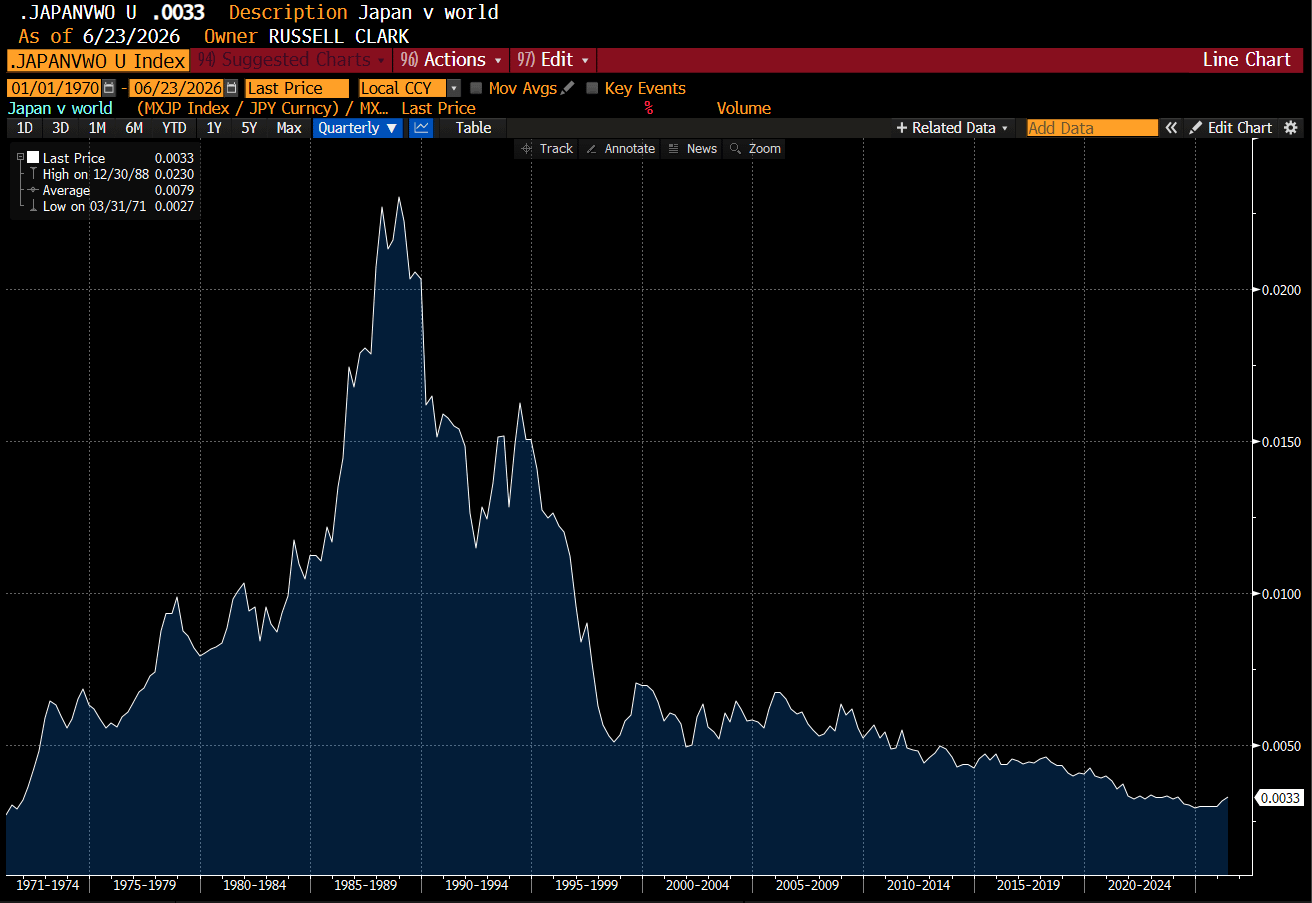

Before the Nasdaq - there was the Nikkei. I was lucky enough to first live in Japan in 1991 as a high school exchange student. If you had told me at the time, that Japan was heading for 30 years of relative decline, I would have not believed you. But that has been the case. MSCI Japan versus MSCI World is a tale of neglect and decline.

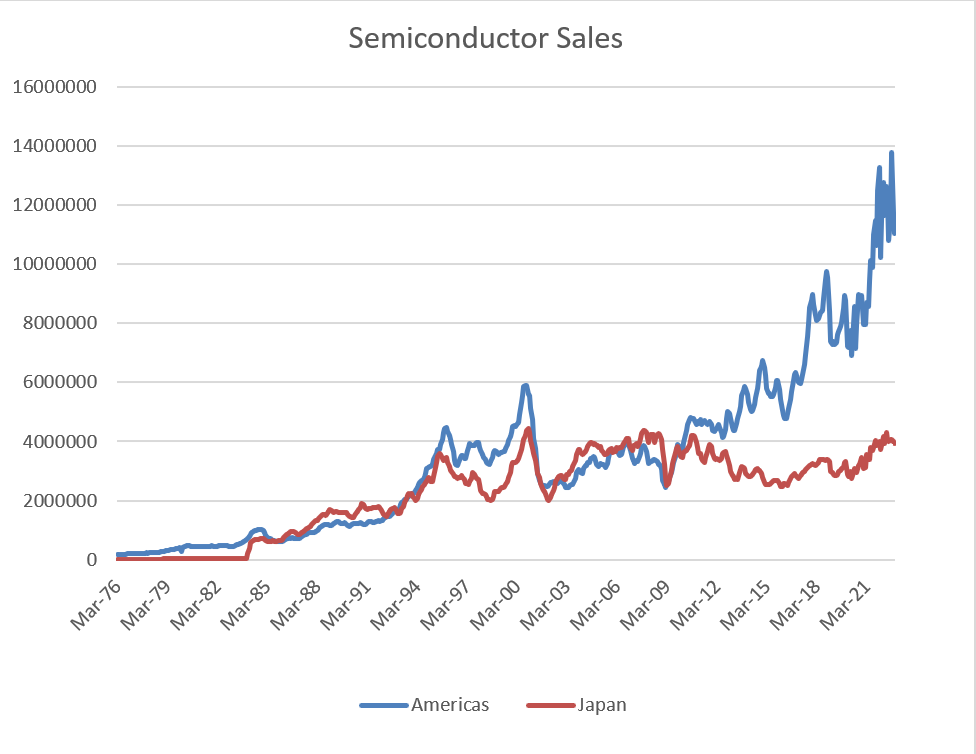

I have a great deal of respect for Japan and Japanese people. But the Japanese economic story since 1991 has constantly felt like one of missed opportunities. Japan led the mobile phone market in the early 1990s. In 1996 I got my first mobile phone in Japan was cheaper and better than the Nokia brick I bought in 2000, and yet, Nokia, Apple and Samsung dominated this market. Going back even further, the Japanese OWNED the semiconductor market in 1980s, generating more sales than the US. But since then, they have been in decline.

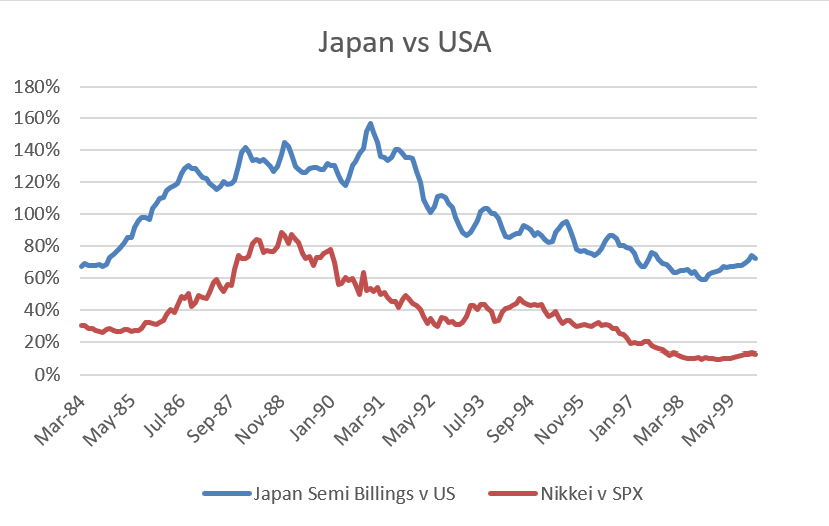

For an old report, I made a very nice chart, showing the relative performance of Japanese sales compared to the US, pretty much tracks Nikkei underperformance. In a way, it links semiconductor sales to market dominance - something we are seeing again today.

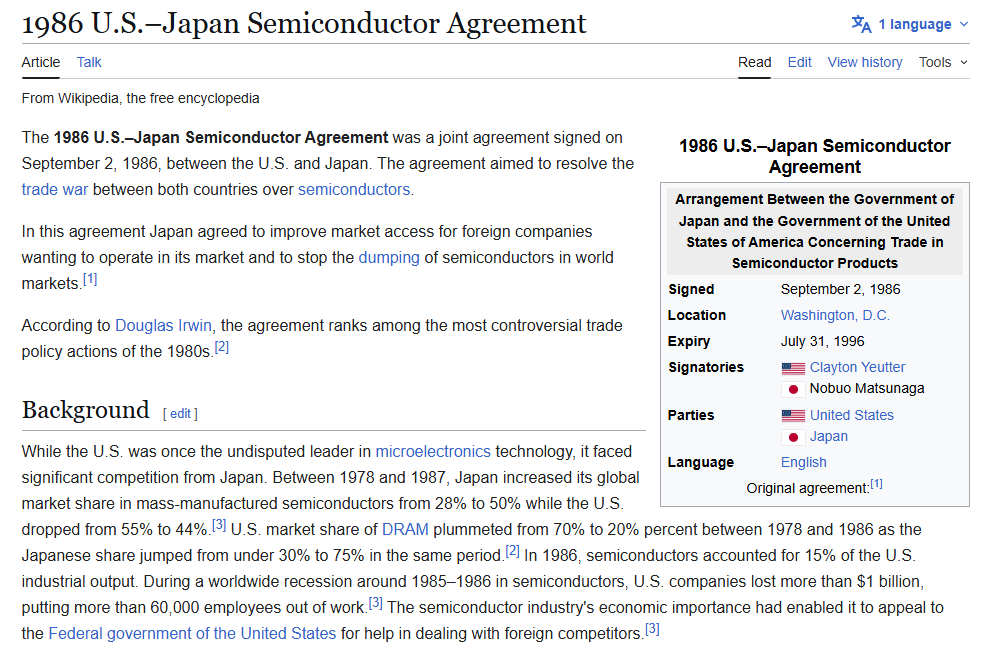

For a long time, I like many other people, blamed the Japanese for their monumental economic fumble. But in this new era we live in, my thoughts on Japan are changing. I am starting to think Japan committed a form of corporate harakiri, mainly to placate the USA. In 1986, Japan basically agreed to stop competing with US semiconductor companies.

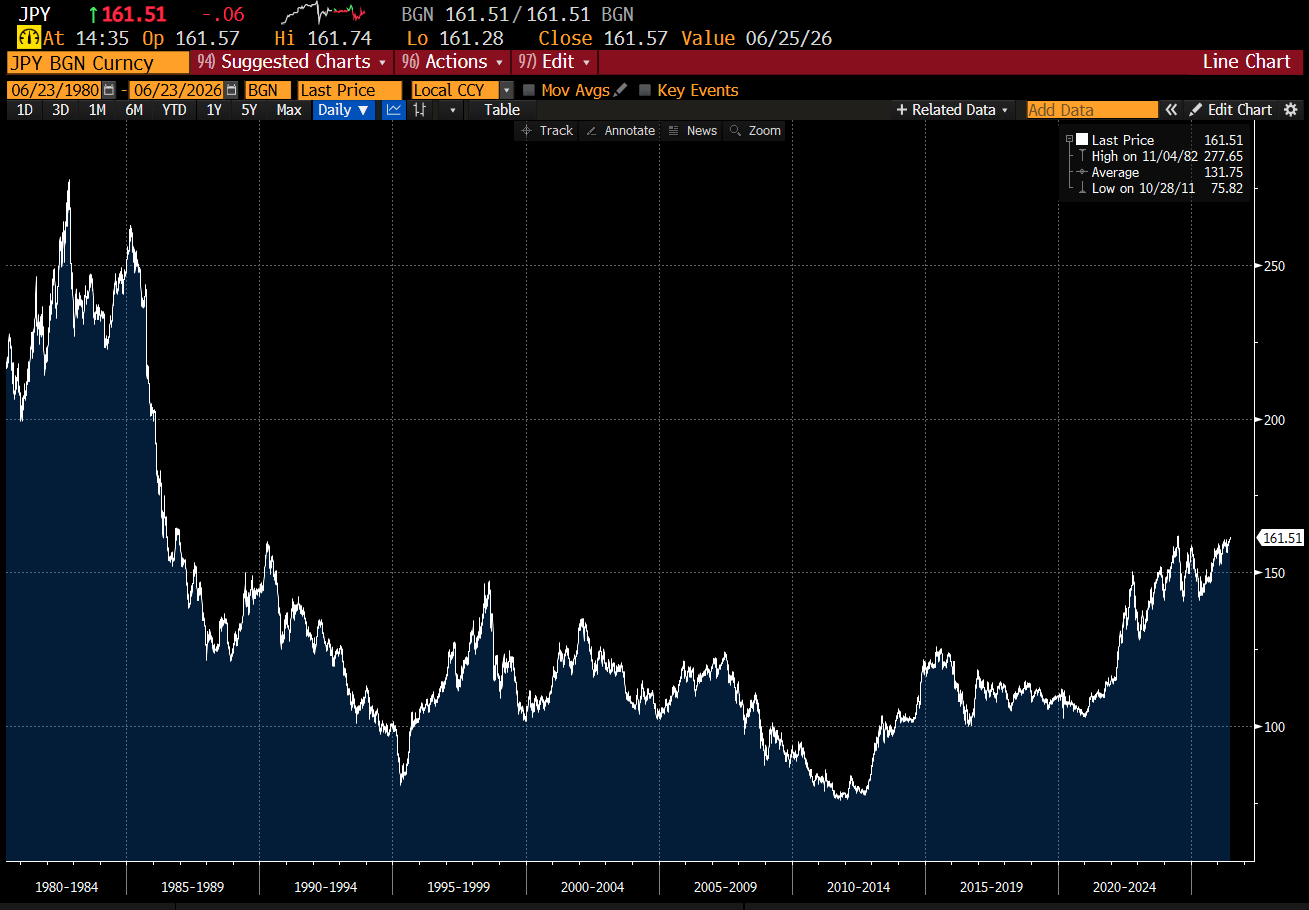

It was also around this time, Japan agreed a steep appreciation of the Yen in the Plaza accord.

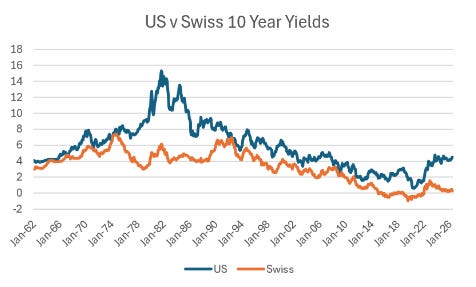

In many ways, it seems that Japan chose to accommodate the US by choosing to stop investing in Japan. Given the outcome of the last time Japan had confronted the US, this is entirely understandable political, if not economic, decision. But there are two things, I want you to take from this analysis. First off all, its was politics, not markets that bought Japan undone. And secondly, the political agreement of 1986, and the Yen appreciation of 1984 should have stopped the Japanese market stone dead, but the Nikkei did not top out until 1989, as Japan unleashed a credit bubble to offset its now obvious industrial problems. The reason I am talking about all this, is that I see a similar set up in the US. I know many people see the US “value creating” machine as unstoppable, and that is totally understandable if you look at just current business and economic trends, but when I look at political trends, the top looks in. I know I am going to regret writing this, as I will be inundated with email and charts showing how dominant the US in tech, market cap, and all other markets. But that is all backward looking. I will start with the easiest areas to see US topping, and move on from there. First of all, is the rejection of US treasuries as reserve assets. I continue to see the weaponization of treasuries as a huge own goal by the US. And this can be seen in the divergence of treasury yields from Swiss bond yields.

Under the Trump administration, NATO allies can no longer take it for granted that the US will offer military security. This has led to allies greatly increasing military spend, which was a Trump administration aim. The huge long term downside for the US is that allies are now developing competing and often cheaper technologies. The DAPRA model that has served the US so well, is now being rolled out globally. In my view, stocks like Lockheed Martin reflect this long term deterioration in their outlook.

Finally US policy on taxation, AI and other issues have revived industrial policy in the rest of the world. As mentioned in a recent post, the most ardent free trading nation in the world, the UK, will no longer allow its tech companies to be bought by the US. DeepMind would not be sold to Google today, and ARM would not be sold to Softbank. Politically, these changes are being made today, but it will take some time to feed through the system, just as it took time to feed through to Japanese asset markets. But they will come. For those with a sense of history, the rise of Socialism felt unstoppable post World War II, but slowly but surely the US and other free nations worked to undermine the USSR. The normalisation of relations between the US and China probably marked the beginning of the end, which started in 1970s, but took until the end of the 1980s to be fully realised. The rest of the world can see that reliance on the US is no longer a tenable political model, and are beginning down the road to sovereignty. If the political process has begun, when does the market recognise it? Maybe it has already. Japan seems to be outperforming US equities again, bond spreads are widening against Switzerland, and gold is still doing better than treasuries. The irony is that the US forced Japan into decline. The US seems to have chosen decline - but perhaps that is why US politics is so febrile. The liberal trade order than made the US so successful it no longer a vote winner, and so nationalism is the political driver of the day. But US nationalism drives nationalism elsewhere, and undercuts the system that has made the US the leading nation it is today. In my thirty years of adulthood, I have seen Japan top out, and now bottom out. I wonder if I will still be around for the bottom in the US.