Gold has been pretty weak this year since it peaked back in February. I liked gold ever since Russian foreign reserves were frozen. For me, this would drive other big nations to diversify away from treasuries, and for China this could only mean gold. I also took the view that gold would do poorly if US yields rose enough, so have been bearish on TLT. This trade did look overbought earlier this year, but has smashed through the 200MDA.

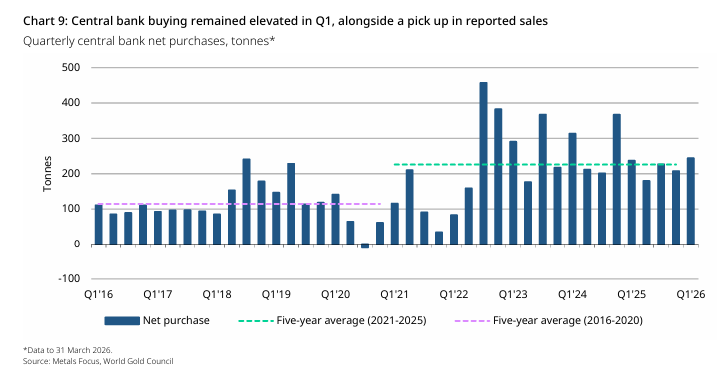

The idea that central banks would buy more gold has been borne out by the data. And to be brutally honest, nothing has changed in the US to change this dynamic.

People talk that Warsh has ended the dollar debasement trade, but the funny thing is there has been remarkably little dollar debasement to end. Gold tends to do well when Asian currencies are strong - something we have seen relatively little off. Asian currencies remain at low points, and look distinctly undervalued.

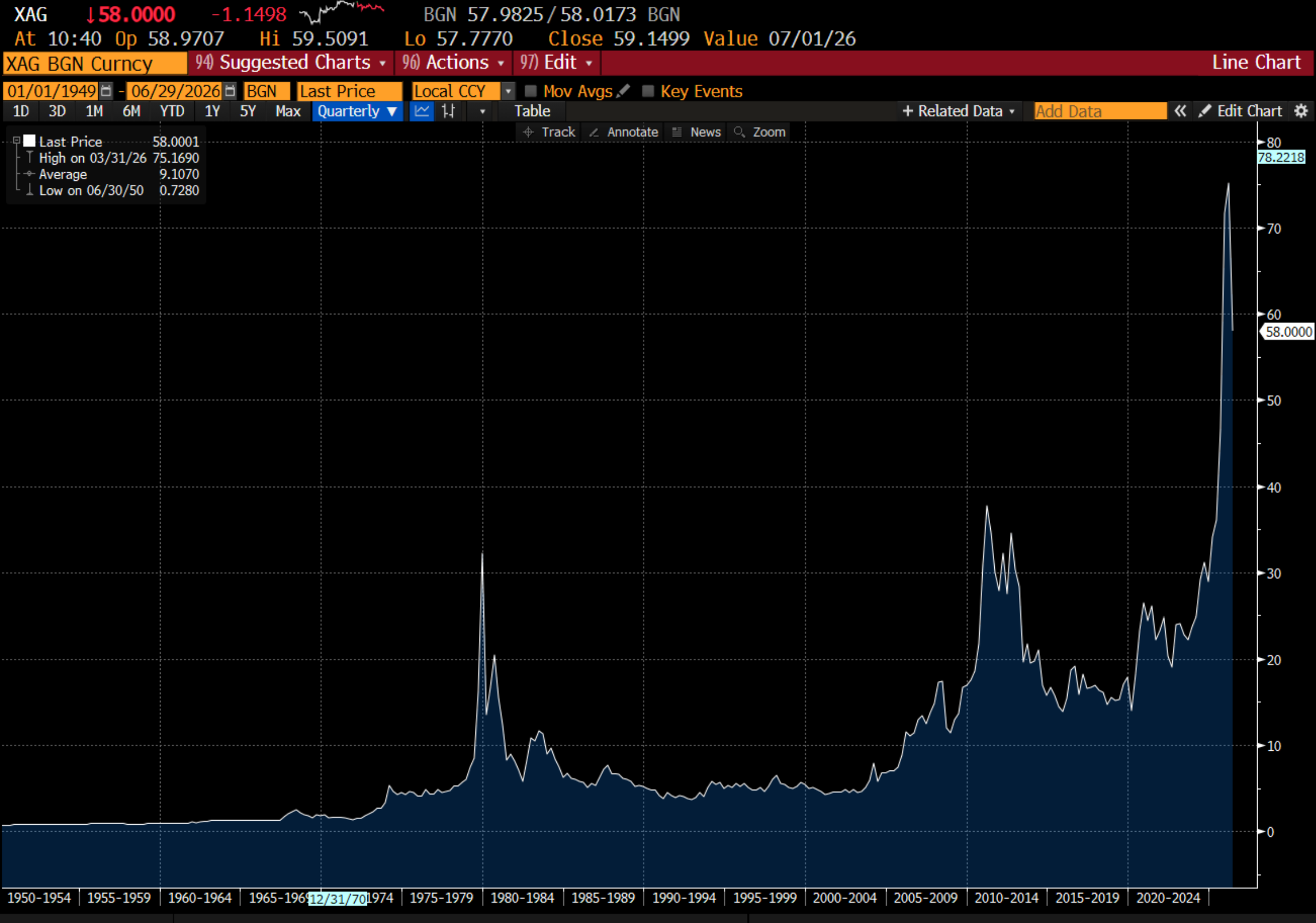

A more valid concern was that retail investors were overly bullish and leveraged long. I could see that more clearly in silver than in gold. Silver does not have central bank buying behind it, and is a much more easily manipulated market. But I did worry that a top in silver tends to mark a top in gold as well.

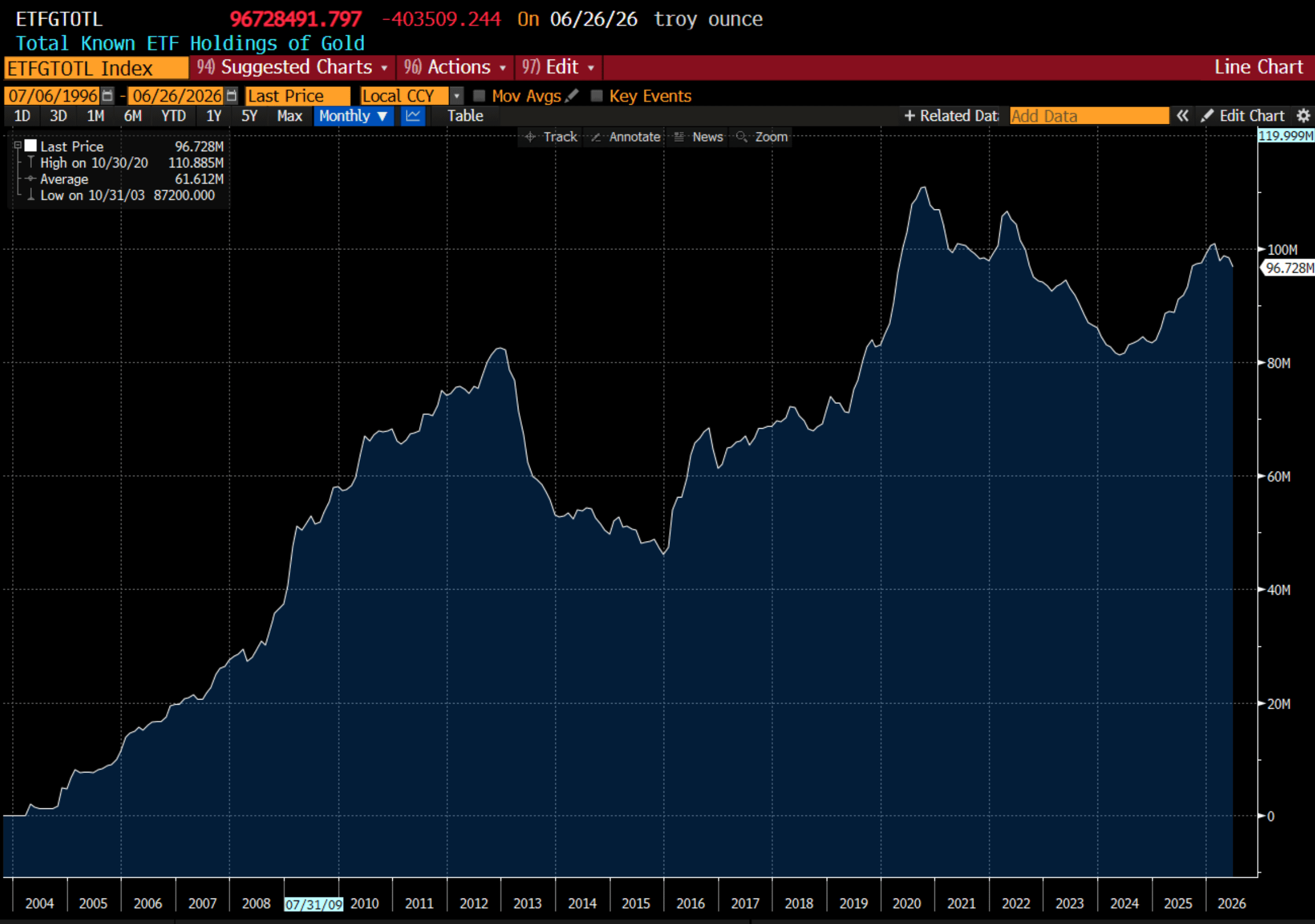

The problem was when I looked at gold ETF holdings, I did not really see any frenzy at all. Holding were still below levels seen in 2020.

Plainly something did not add up. And over the weekend I had a think, and I think I have worked out what’s going on.