I get asked who in financial markets do I read? The answer is not many people. For some reason, people with not much to actually say will pad out their comments with all sort of superfluous gunk (quoting ancient Greek history or alluding to some esoteric science are classic signs of a time wasting financial writer). But if I do read someone, and they made me money, then I will keep reading their stuff. GS research has made me money, and Chris Woods out of Jefferies, have both made me money. As of the moment, they are on opposite sides of the AI trade - so I will lay out the bull and bear case for you.

The AI boom is driven by a huge increase in Capex by the AI scalers. Bloomberg has provided an estimate of the spend.

Basically we are in peak acceleration of AI spend, with 2026 seeing capex rise by USD344bn to a total of USD 833bn. But the forecasts still have capex rising to 2032.

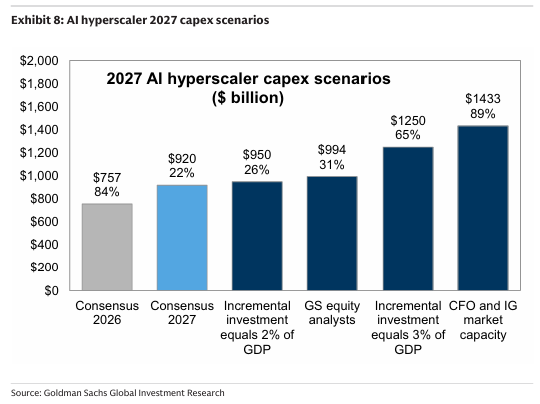

But GS are arguing that market may be too bearish, and capex grows even more in 2027.

And essentially saying big capex booms have been larger in the past.

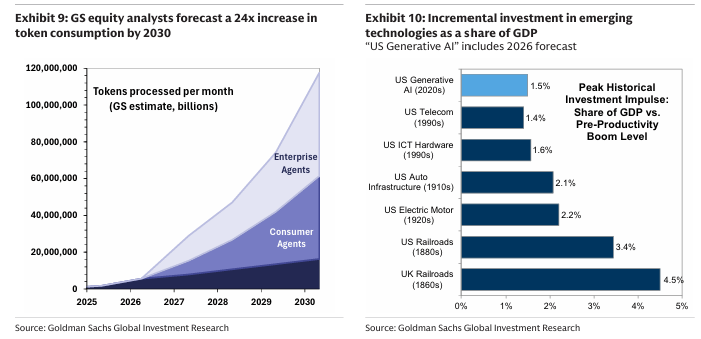

AI is a transformative technology, so capex can be even larger than market expects. And that is the bull case.

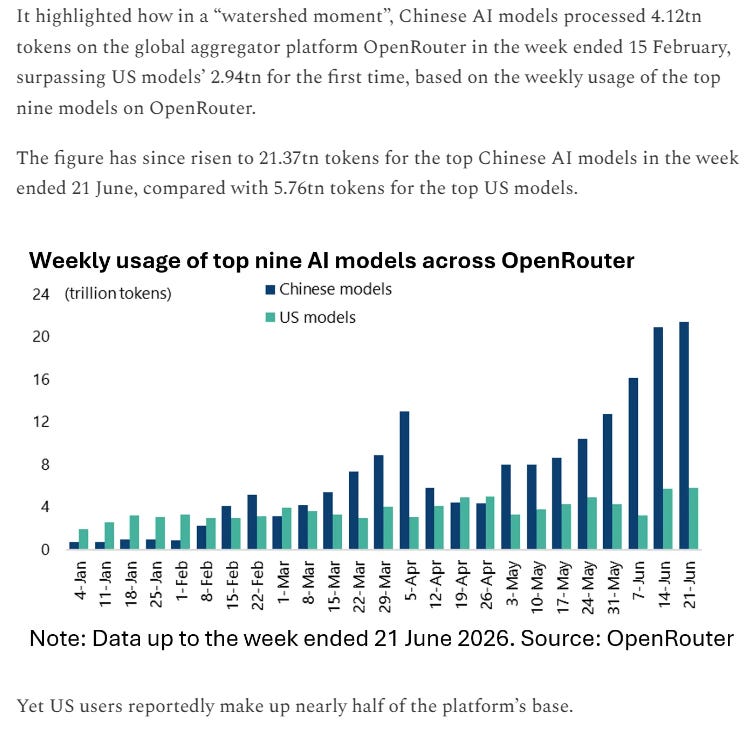

Chris Woods has come out with the bear case. He looks at OpenRouter data, which is a website that allows you to access multiple AI models. What Chris is saying is that Chinese AI models are now dominating US models.

Or in essence, what “free markets” have always done, let the low cost producer take market share. And this has been highlighted by numerous people, that Chinese AI models are very cheap. The cheapness of Chinese AI is in part driven by the cut throat competition of Chinese tech companies. The Hang Seng Tech index bares no resemblance to the Nasdaq.

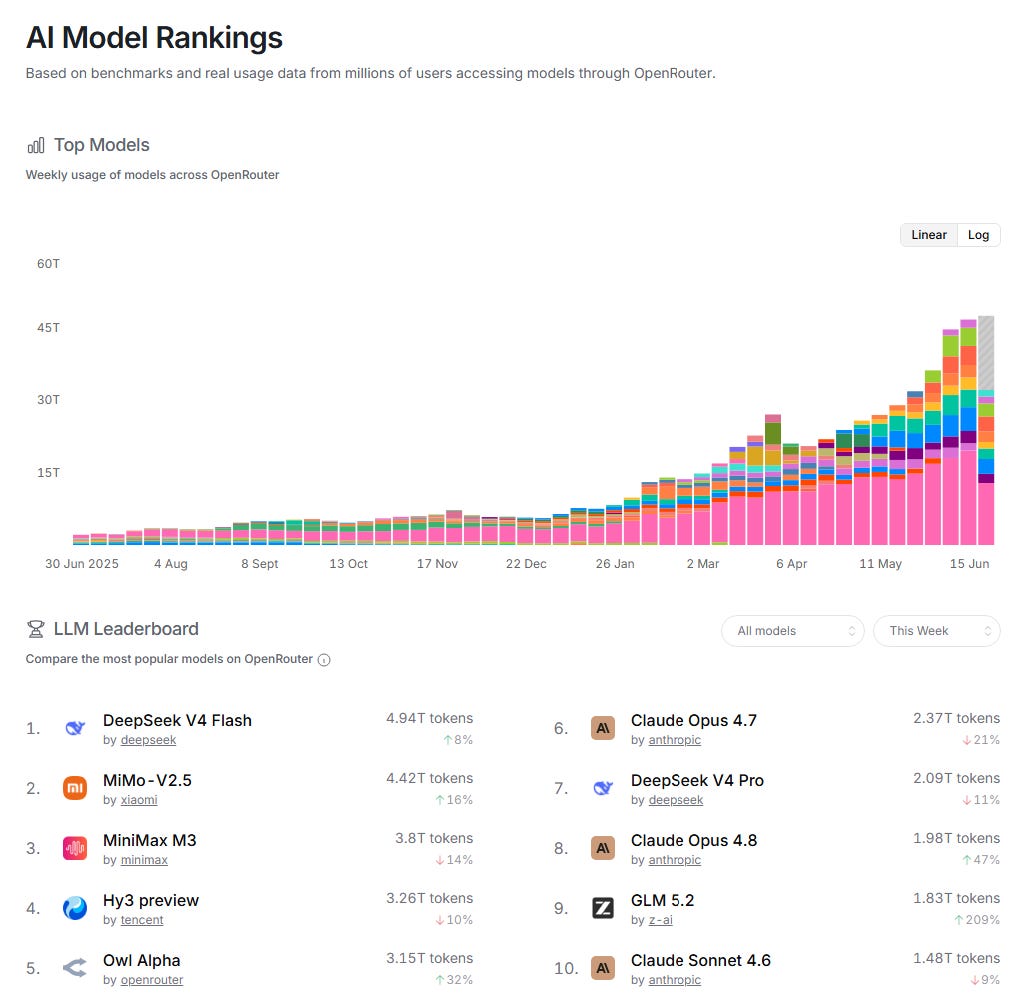

The key point that Chris is making is that half of OpenRouters users are in the US, which implies that US customers are opting for Chinese AI models. Here are the most recent top 10 models.

So Xiaomi, Tencent and minimax are all listed, and their shares are near cycle lows. And that is your bear case - cutthroat Chinese competition in AI will undercut the big US models.

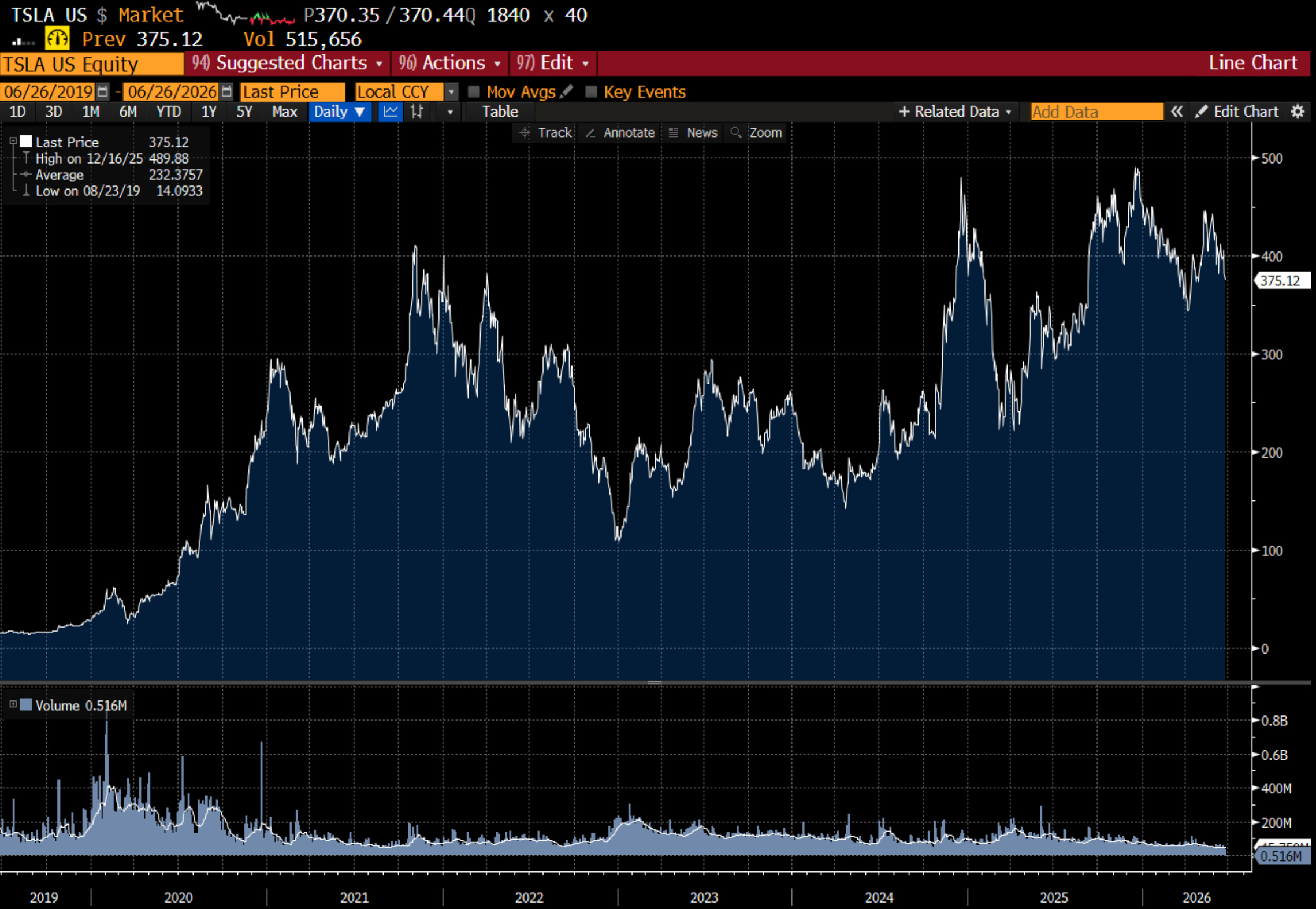

So now time for a wealth warning. I thought Chinese EV competition would hurt Tesla earnings. And it has, earning expectations for Tesla in 2026 have fallen from USD 7.50 a share in 2023 to less than USD 2.00 a share today.

Collapsing earning expectations have had almost no effect on Tesla stock price.

Politically, I understand this paradox. President Trump has based his electoral success around defending American businesses. Chinese AI might be cheaper, but how many big US businesses can realistically use Chinese AI? And it seems at odds with the revenue numbers we are hearing out of Anthropic.

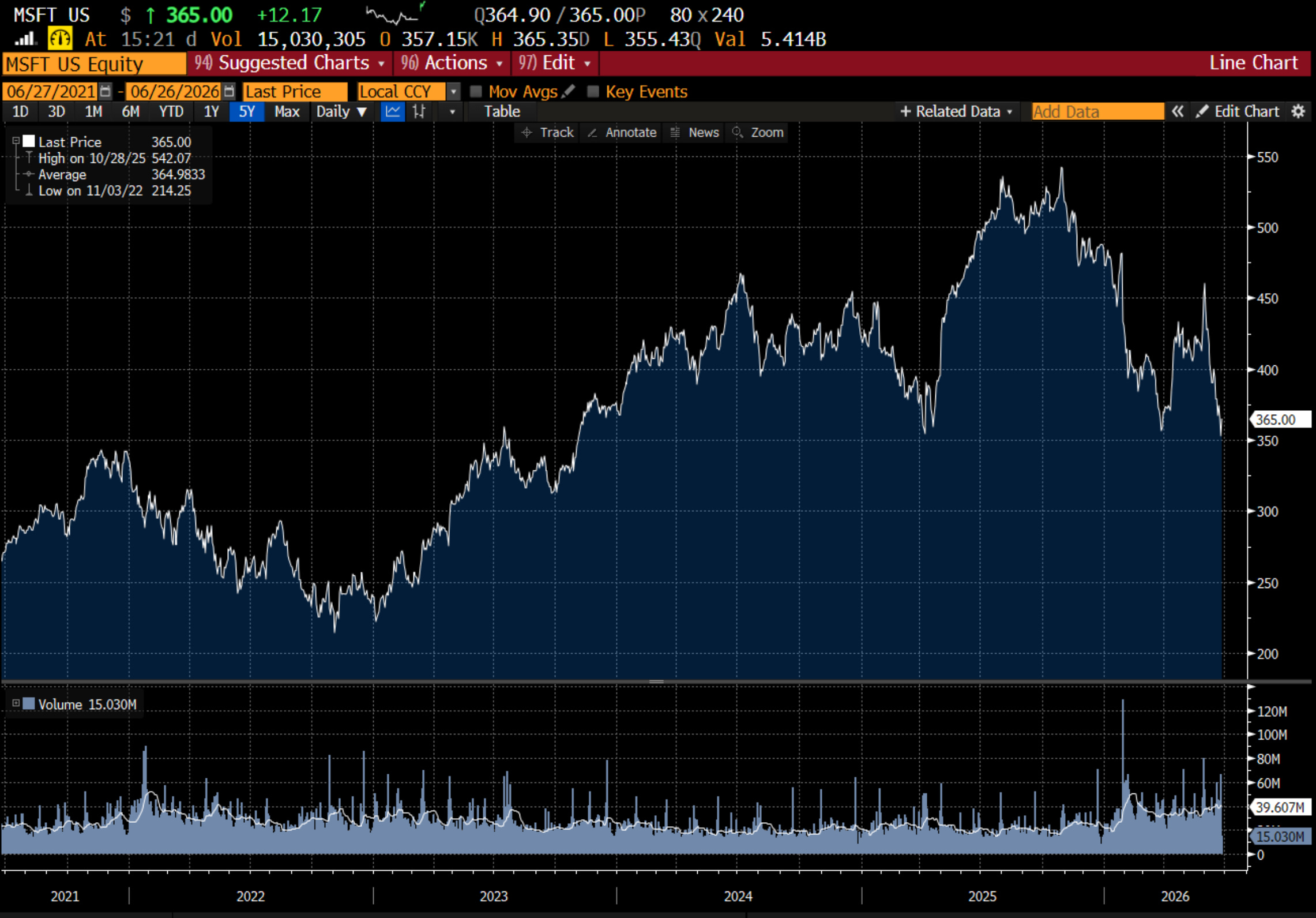

And here lies the problem - I respect GS, and they are bullish, and I respect Chris Woods, and he is bearish. What I will say, is that the amount of leverage being applied to the AI trade means you probably need the market to price in some of Chris Woods bearishness first. Or what I am saying you can be tactically bearish - but you would need some other signal to get really beerish on AI. You need one of the hyperscalers to quit - and cut capex. That might happen - but usually the market forces this by crushing share prices. Only Microsoft comes close to fitting that description.

And my guess is that Microsoft is suffering from its software business looking exposed, rather than its Capex. If politics in the US has not changed - my guess is that Chinese AI will comes under more political pressure going forward. And perhaps that is why Chinese AI is trading so poorly.