If you wanted to get bearish on the whole AI trade - then you could look at Meta, Microsoft and Oracle share prices and say that the market is taking a dim view of AI. All have been lacklustre recently.

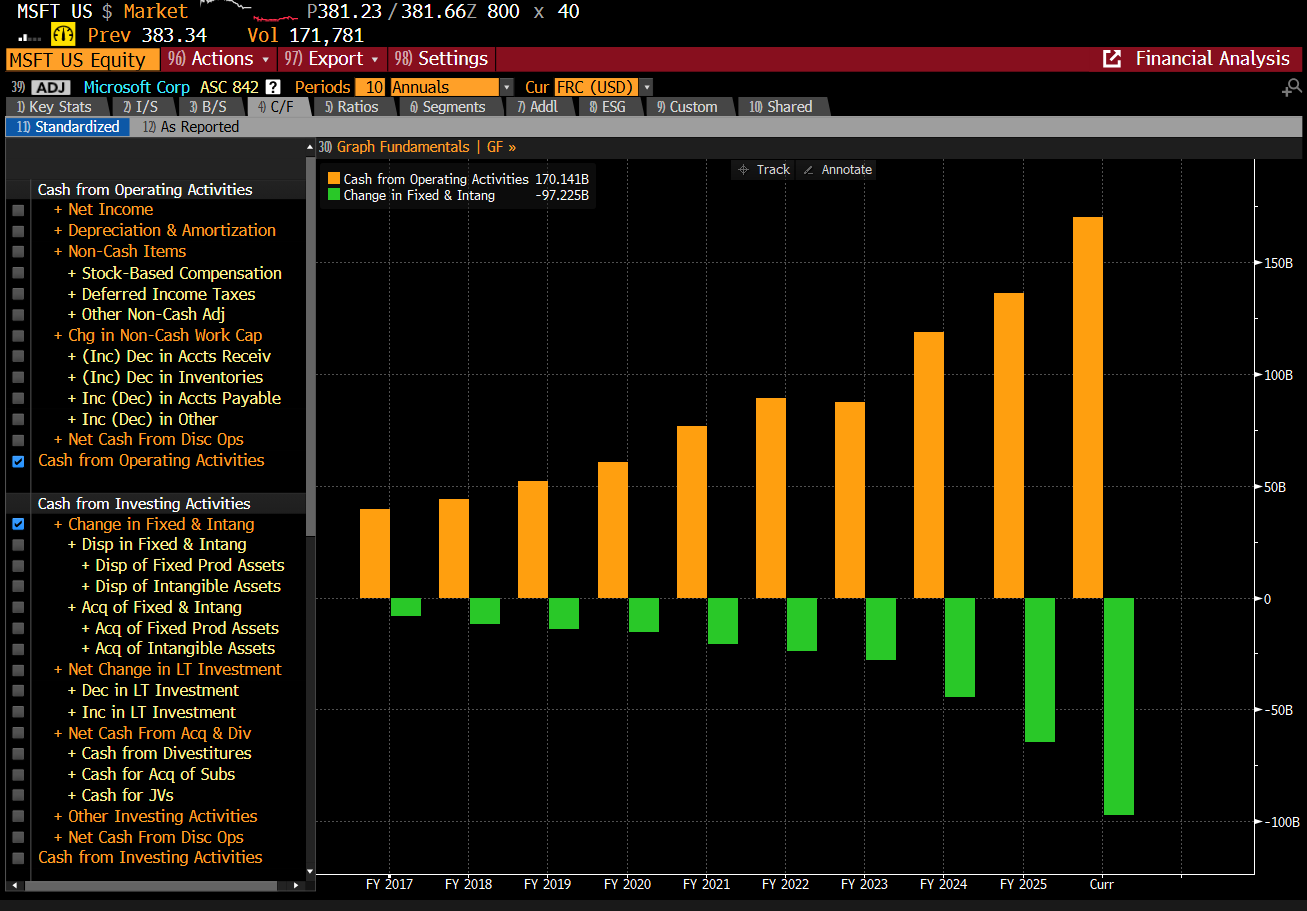

There is no mystery to their share price weakness. All are investing heavily in data centres, and so free cash flow after capex is falling. Microsoft it a good example.

All of the above is factual. Share price has been weak as investment has grown. What does it mean - well that is where the analysis comes in. There are various options. The first I would call the traditional Wall Street MBA version - “Maximum Bullish Always” which would centre around exploding demand, and capex is needed to keep up with demand, and would see current share price weakness as a buying opportunity.

The second style of analysis is also MBA, but a macro/short seller interpretation so “Maximum Bearish Always”. In this analysis, the weakness is hyperscalers is direct analogy to the dot com bubble, where the internet stocks weakened first. The analogy here is internet stocks like Amazon topped out late 1999, and then hardware stocks like Cisco followed with a lag, as the internet stocks cut spending. In this analogy, now is the time to be shorting memory stocks, as hyperscalers have topped out.

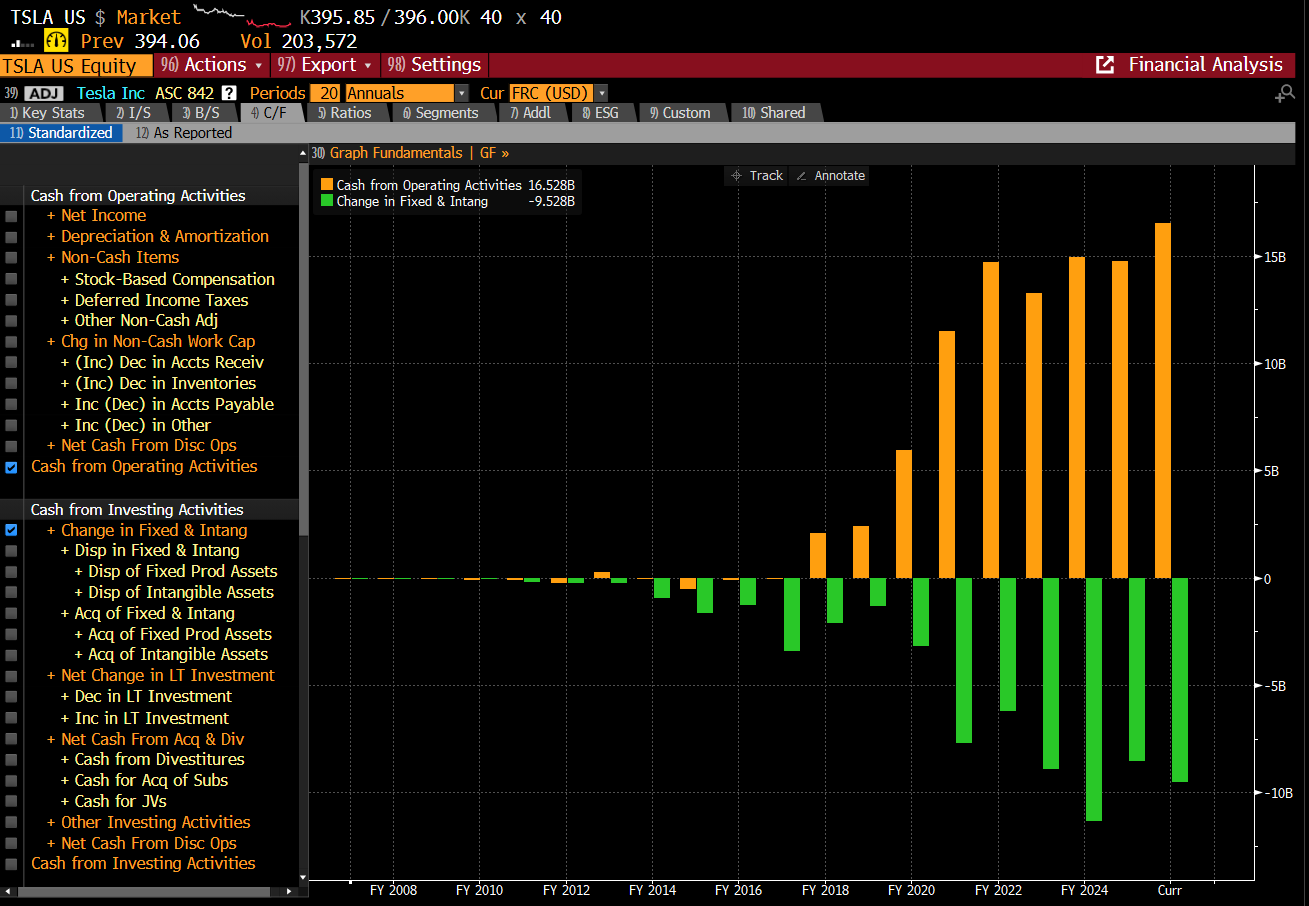

For me, both these analyses seem wrong to me. What I see is that AI is booming, but it is also a threat to existing tech companies. Probably the biggest threat comes from SpaceX. Elon Musk has been a disruptive entrant in payments (PayPal), autos (Tesla), rocket launch (SpaceX) and telecommunications (Starlink). If I saw Elon entering my industry, I would also become super defensive as well. In this case, I would be trying to push up the cost of entry AND secure infrastructure to try and keep xAI from becoming a serious competitor. Unfortunately for the existing players, SpaceX was able to list, and Elon will about to keep investing. As a reminder, Tesla invested far more than cashflow and was the biggest short in the market for years before finally taking off.

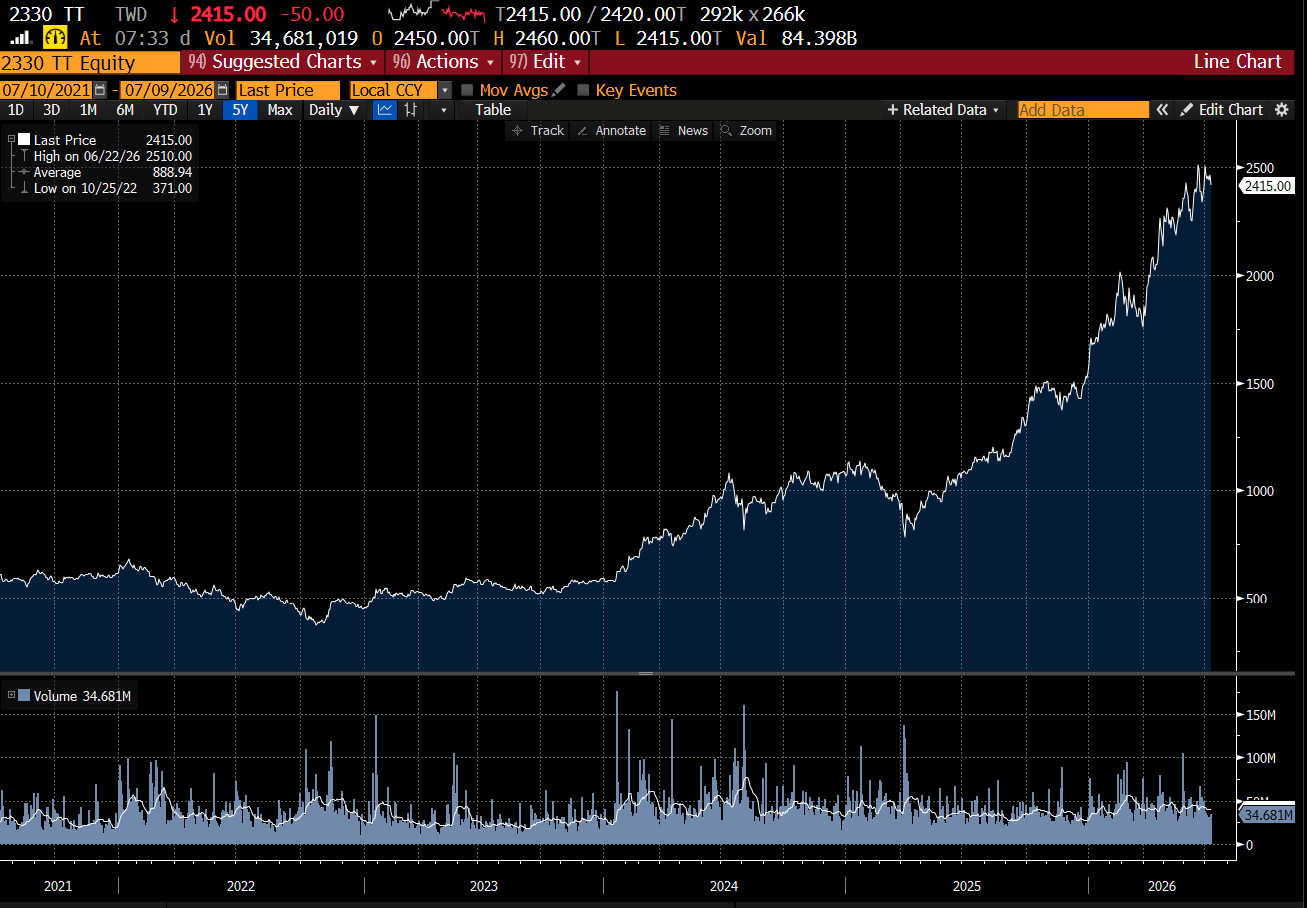

So Russell’s non MBA read of the AI market is that hyperscaler’s shares are weak not because AI is a failure, but because a powerful new player has entered the industry. I admit the rise of leveraged semi ETFs, like MUU make memory stocks volatile - its hard for me to get too bearish when TSMC is near all time highs.

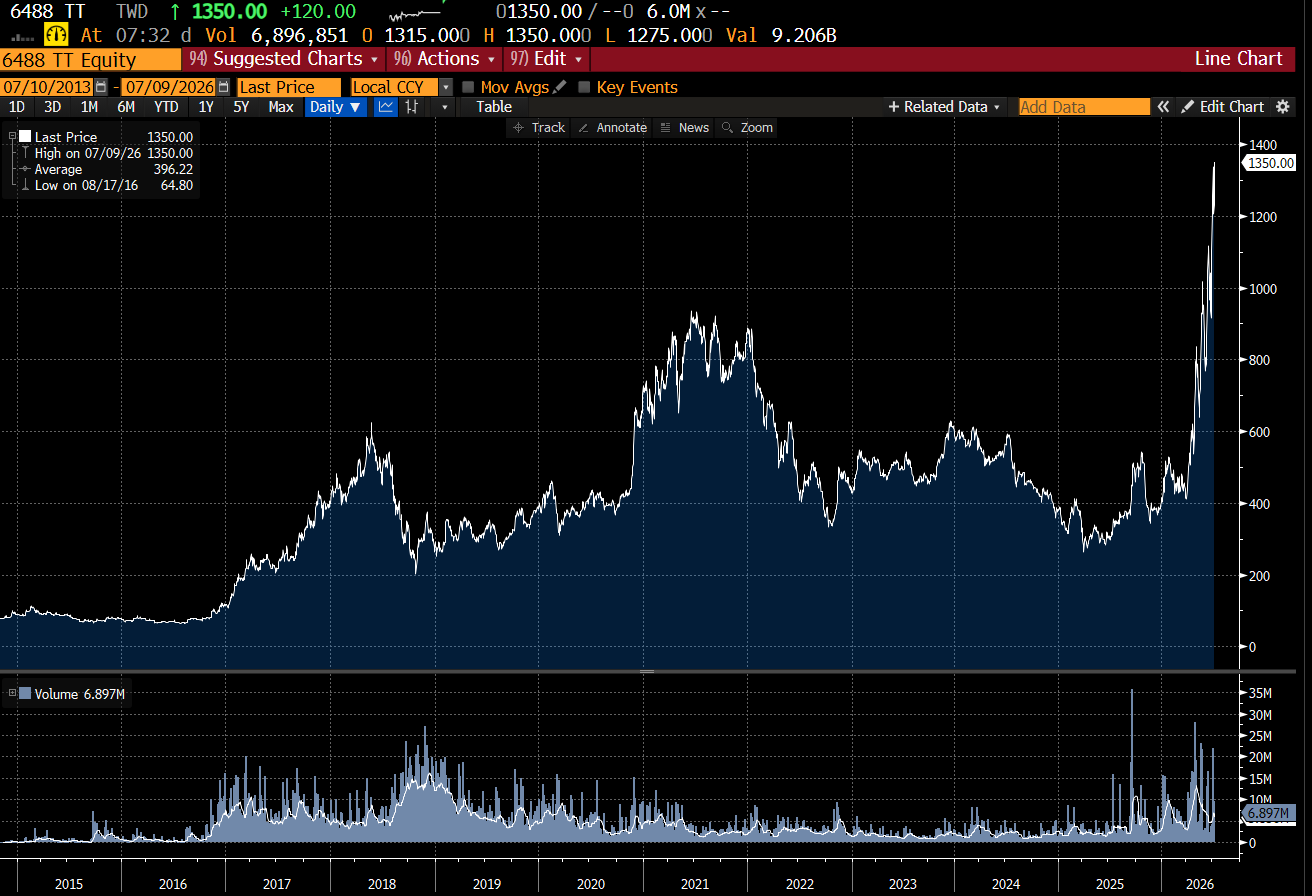

Or when Taiwan listed wafer company, Global Wafers is at at all time highs.

If Microsoft, or Meta or Oracle were suddenly to cut capex - yes that would be bearish for semiconductors, but it would probably be even more bearish for these hyperscalers. It would be boosting short term cashflow at the expense of long term market share. What I think is very telling was that in the dot com boom, credit spreads starting rising in 1998, but the dot com bubble did not burst until 1999/2000. Currently credit spreads are at all time tights - which suggests the cash will keep on flowing to drive the AI trade.

If you want to be bearish, legacy hyperscalers are probably the best bet - not AI infrastructure.