In my first stint as a macro hedge fund manager, I used to obsess over capital flows into and out of Japan. When the capital was flowing out - you wanted to buy, and went it was flowing back, you wanted to sell. I now realise I was studying the symptoms of a pro-capital world, but having only lived in a pro-capital world, how would I know any different? But now we live in a pro-labour world, and symptoms have changed. Capital is no longer getting build, up but being run down.

I think the easiest way to understand it is that in a pro-capital world, we were creating huge pools of capital, and Japan was creating the largest pools. In fact, Japanese pools of capital were so large, the BOJ and the government had to go out of their way to force capital out of Japan. Hence, NIRP, QE and YCC were all invented in Japan.

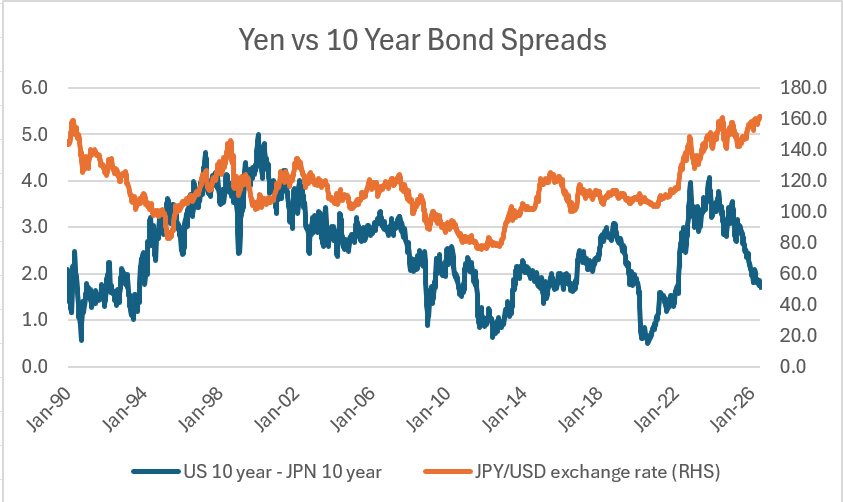

One feature of this was that whenever US 10 yields fell, the spread to JGBs would fall, and the Yen would rally. This was a feature of markets from 1994 to maybe 2020. But since then, the spread between JGBs and treasuries have collapsed, but Yen continues to weaken (see my posts on “long Yen as new Widowmaker”)

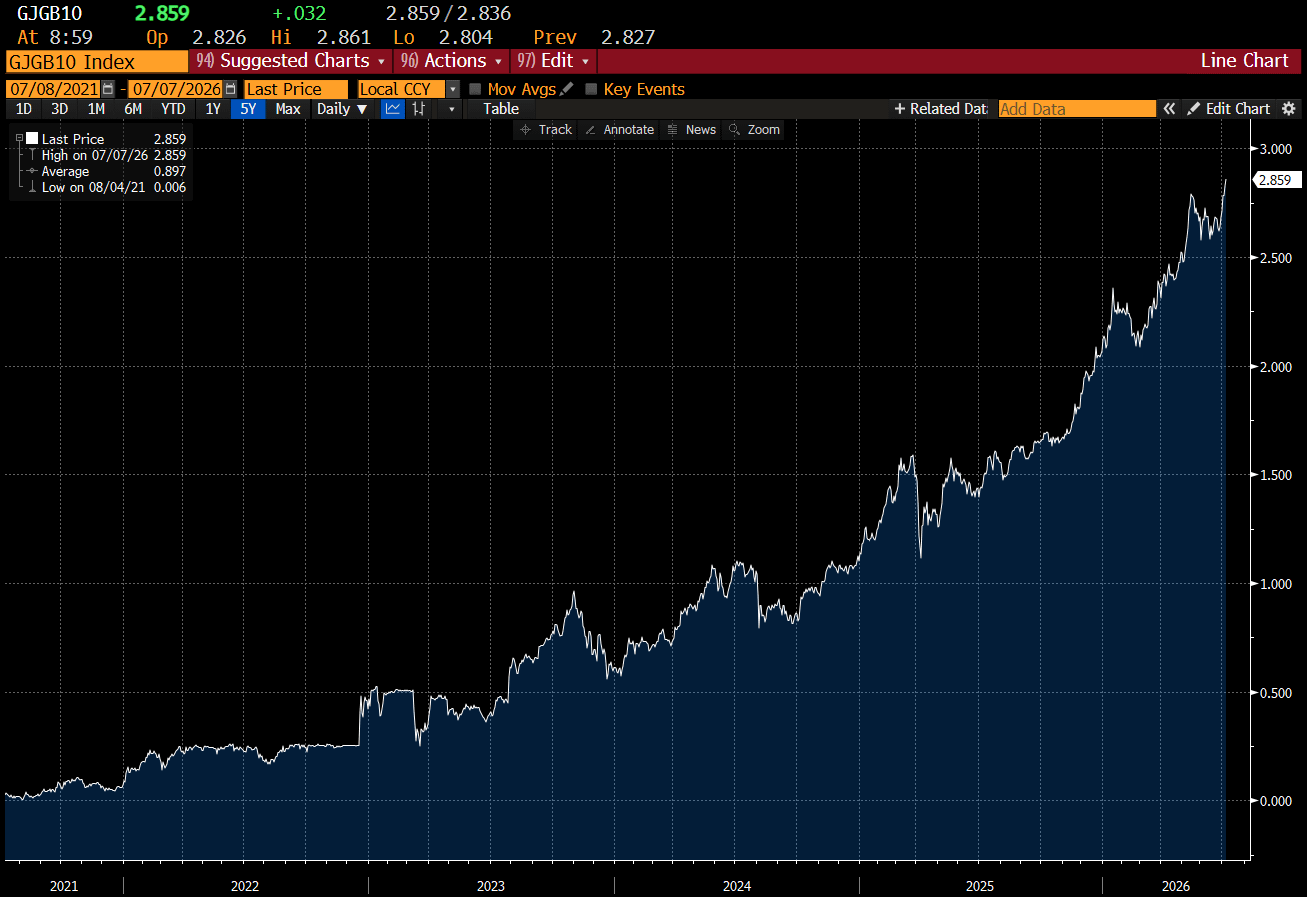

If we break out the spread line above in to its components, then what we have is the yield on the Japanese 10 year rising rapidly.

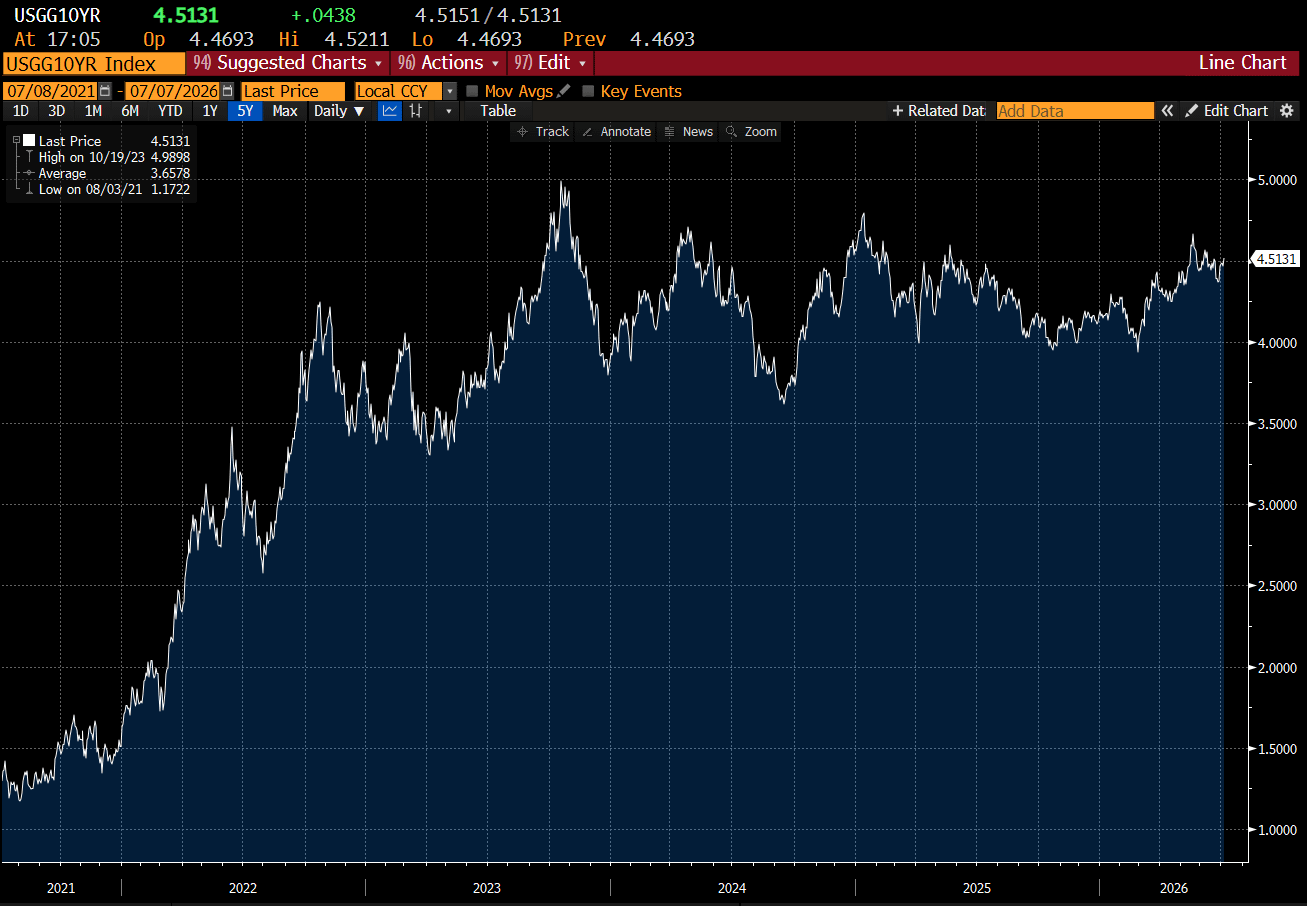

While Japanese yields are rising, the US 10 year has been stuck in a range since 2023 now. This seems a bit odd, as Japanese have far more savings than the US. It feels like higher Japanese yields should drive higher US yields. But over the last two years, nothing.

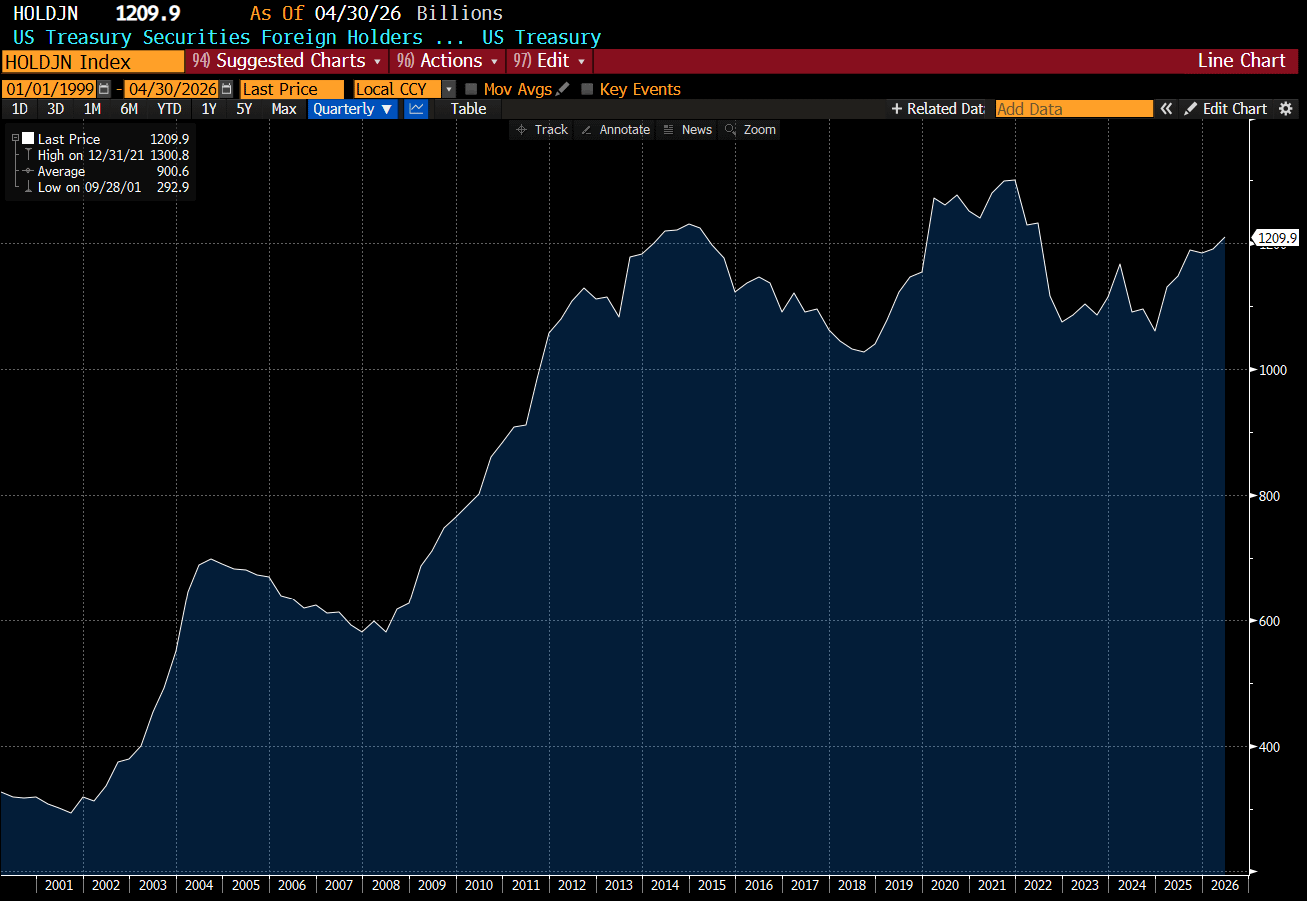

If you believe in my pro-labour theory, what the market is saying is that inflation, and the rise of populist politics is causing investors to reduce idle cash balances to a minimum. Another big change is that governments do not buy treasuries as foreign reserves, but buy gold instead. Corporates do not hoard cash, but spend it. And so capital is getting scarce. For Japan, I think we are getting ready for the other shoe to fall. And that is, Japan needs to start selling treasuries if it wants the currency to appreciate. Japan holds the majority of its foreign reserves as US treasuries. It is the largest holder at USD 1.2 trillion.

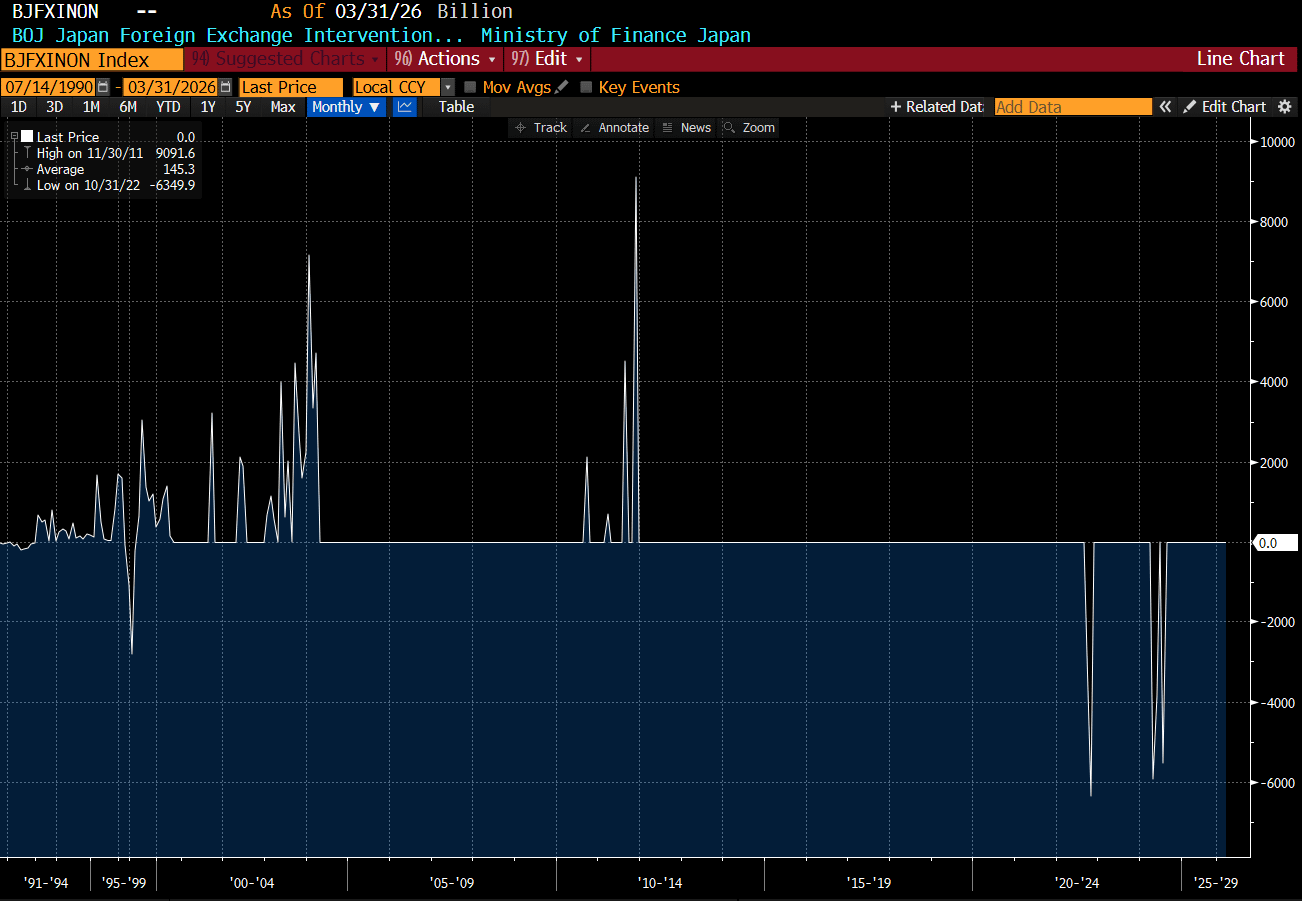

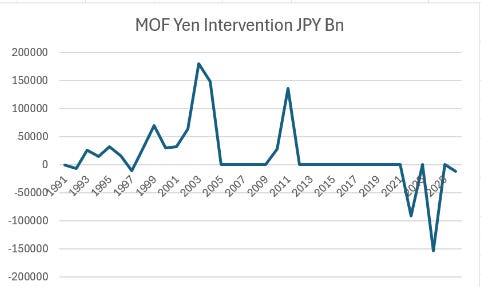

If you wanted just one graph to explain the new world order, the BOJ foreign intervention graph is a pretty good one. They used to have to sell Yen and buy USD. Now they need to sell USD and buy Yen.

The Ministry of Finance has a similar graph, although not loaded on Bloomberg. In 1998, during the Asian Financial crisis, Yen was weak against the USD, but very strong against other Asian currencies - which is why we see some Yen buying then. But the flip from USD buying to Yen buying in recent years is extreme.

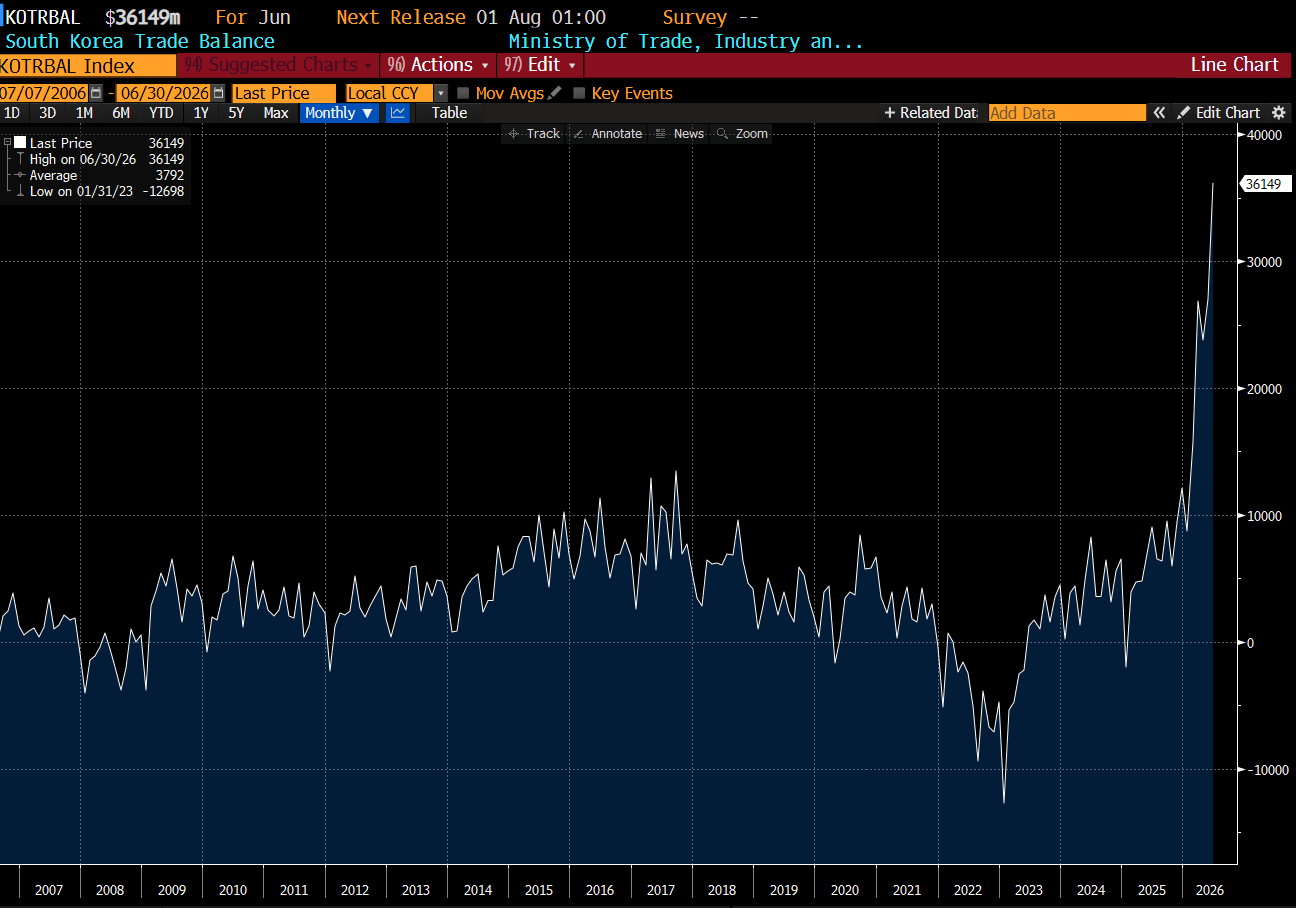

So the shift from a pro-capital to a pro-labour world is leading Japan to sell foreign assets. It is also leading to rising interest rates in Japan. You could argue that Japan now runs an overall trade deficit, and so this is why we are seeing a changing dynamic. The problem with that view, is that Korea, a country that has similar economy to Japan has record trade balance.

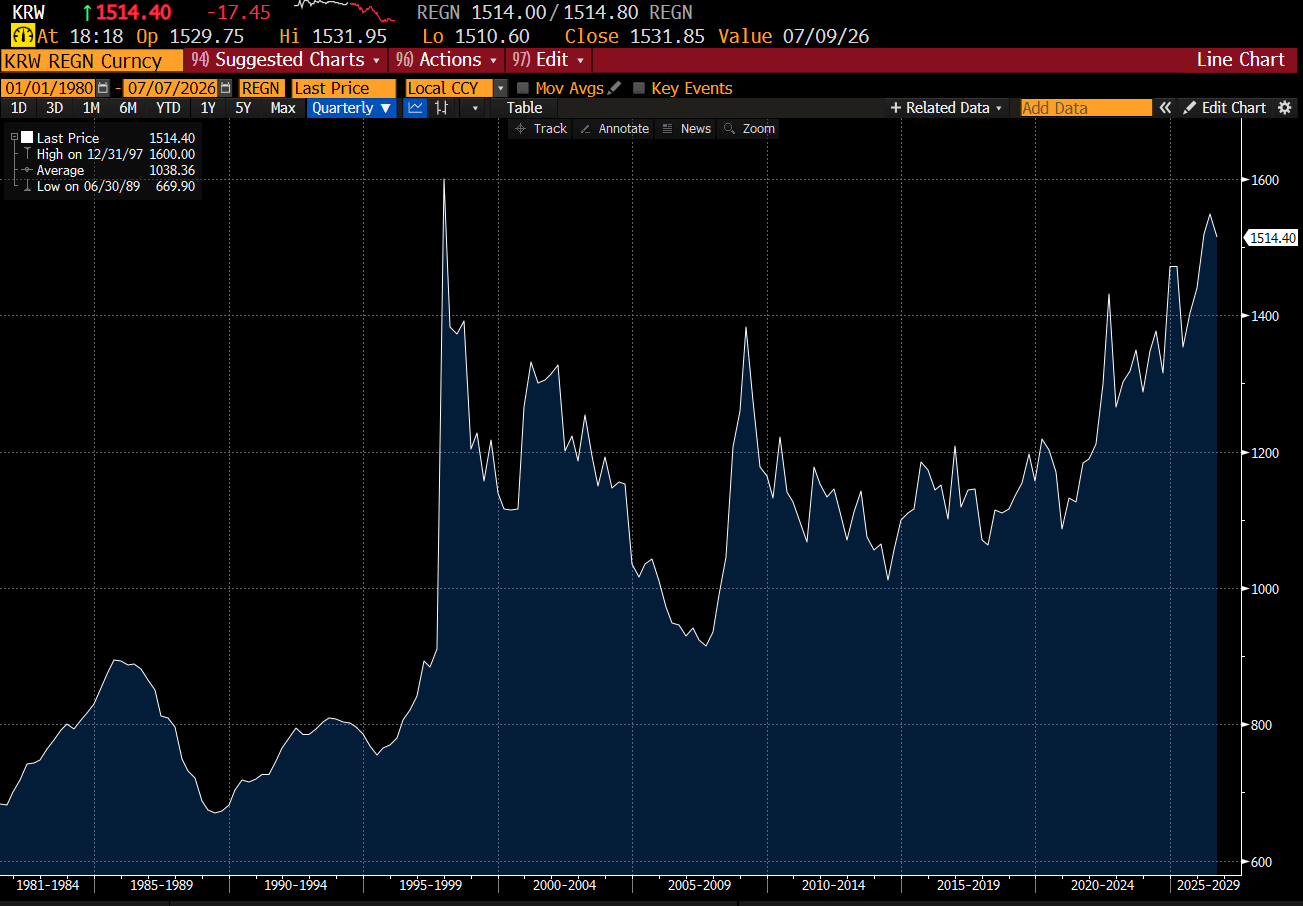

This record trade surplus has not seen the Korean Won appreciate. In fact is has a record weak exchange rate. What is bad about this for US treasuries was that when Korean Won or Japanese Yen used to appreciate from having a trade surplus, they became buyers of treasuries. Now that currencies do not follow trade flows, there is no natural buying of treasuries.

For me, everything seems to be working in reverse, which means that the next economic surprise should be higher yields - the opposite of what happened in the 1990s and 2000s.