Below is a note from 2013 - In Italics, with added thoughts after

Gold buying as a leading indicator of financial distress

I wrote a note on gold late last year, pointing out that the gold price and the Indian rupee seemed to be correlated to me. With that view I suspected that if the Indian rupee fell, gold would then also fall. However market action has been the reverse, with gold falling before the Indian rupee fell, and the fall in gold was greeted with a record surge in gold buying in India. These Indian gold buyers have been rewarded with gold once again moving to new all time highs in rupee terms as India has entered a period of currency and possible financial crisis.

This led me to thinking about whether it was common to see elevated gold buying prior to financial crises. Certainly, the most motivated buyers of gold will be those depositors who take a view that their banks could go bust, either through their own reckless behaviour or government’s reckless behaviour. I went to the World Gold Council website (www.gold.org) to collect data on consumer (not official) buying of gold. Alas there was no single spreadsheet which I could consult, so the data had to be complied from a number of news releases. Below I present gold buying over time with what I believe is the best visual representation of financial distress in each market.

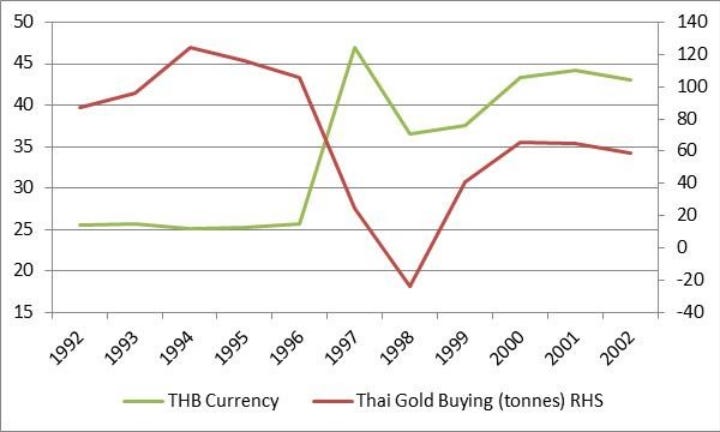

Thailand

We can see an increase in Thai gold buying before its major devaluation 1997.

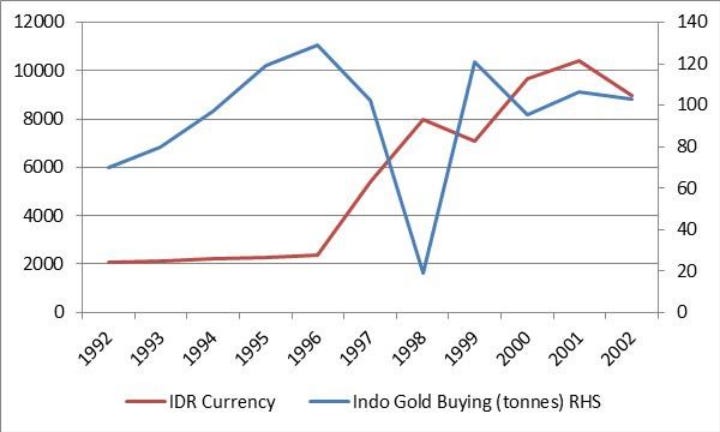

Indonesia

Likewise Indonesian gold buying spiked and peaked before its currency devaluation.

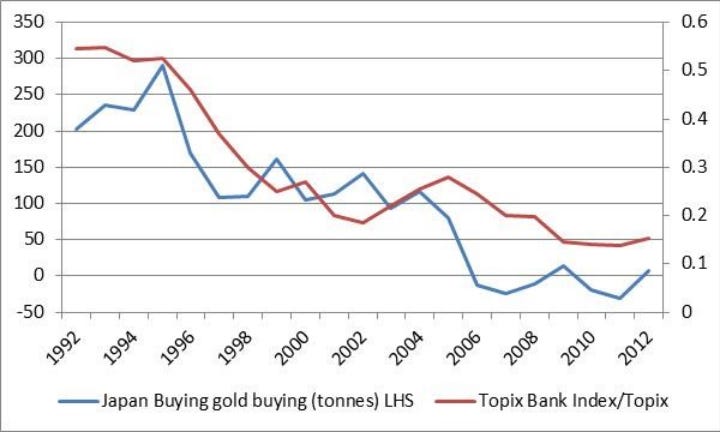

Japan

Japan has never faced a meaningful currency crisis, but an ongoing financial crisis. Japanese gold buying peaked as Japanese banks started to underperform the markets. That is Japanese investors perceived the weakness of their own financial system and started buying gold.

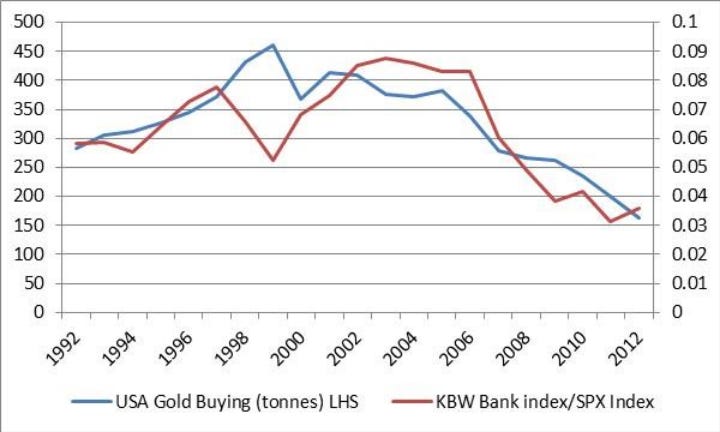

USA

Much like Japan US gold buying seems to peak at the same time as banks peaked versus the market, and seem to reflect depositor’s views on US banks that they were undertaking reckless lending behaviour.

Conclusion

We have recently seen big increases in gold buying by emerging market countries with the World Gold Council reporting a 71% increase in Indian buying, Chinese buying was up by 87%, Turkish buying was up by 73% and Russian buying up by 184% in volume terms in the second quarter of this year. For gold bulls they take this as a sign of ever increasing emerging market demand for gold potential driving gold prices higher. For me I take it as a sign of domestic emerging market investors voting with their feet against their own currencies and financial systems. Investors should be aware of the rising financial risks in emerging markets.

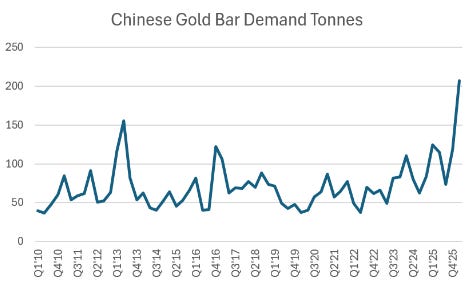

In a recent note, I showed how Chinese consumers had gone all in on gold.

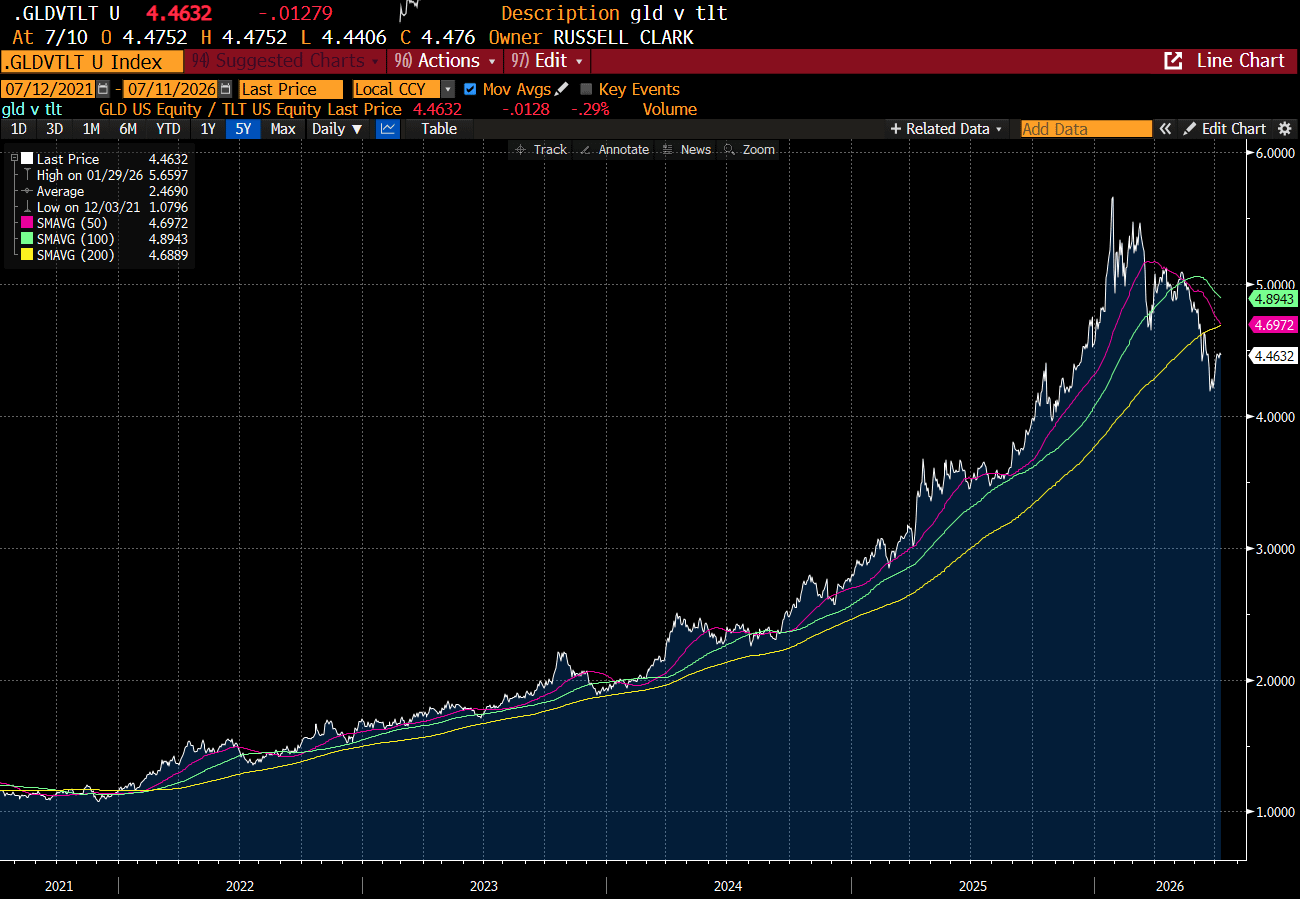

And since this buying orgy, GLD/TLT has fallen back below its 200MDA.

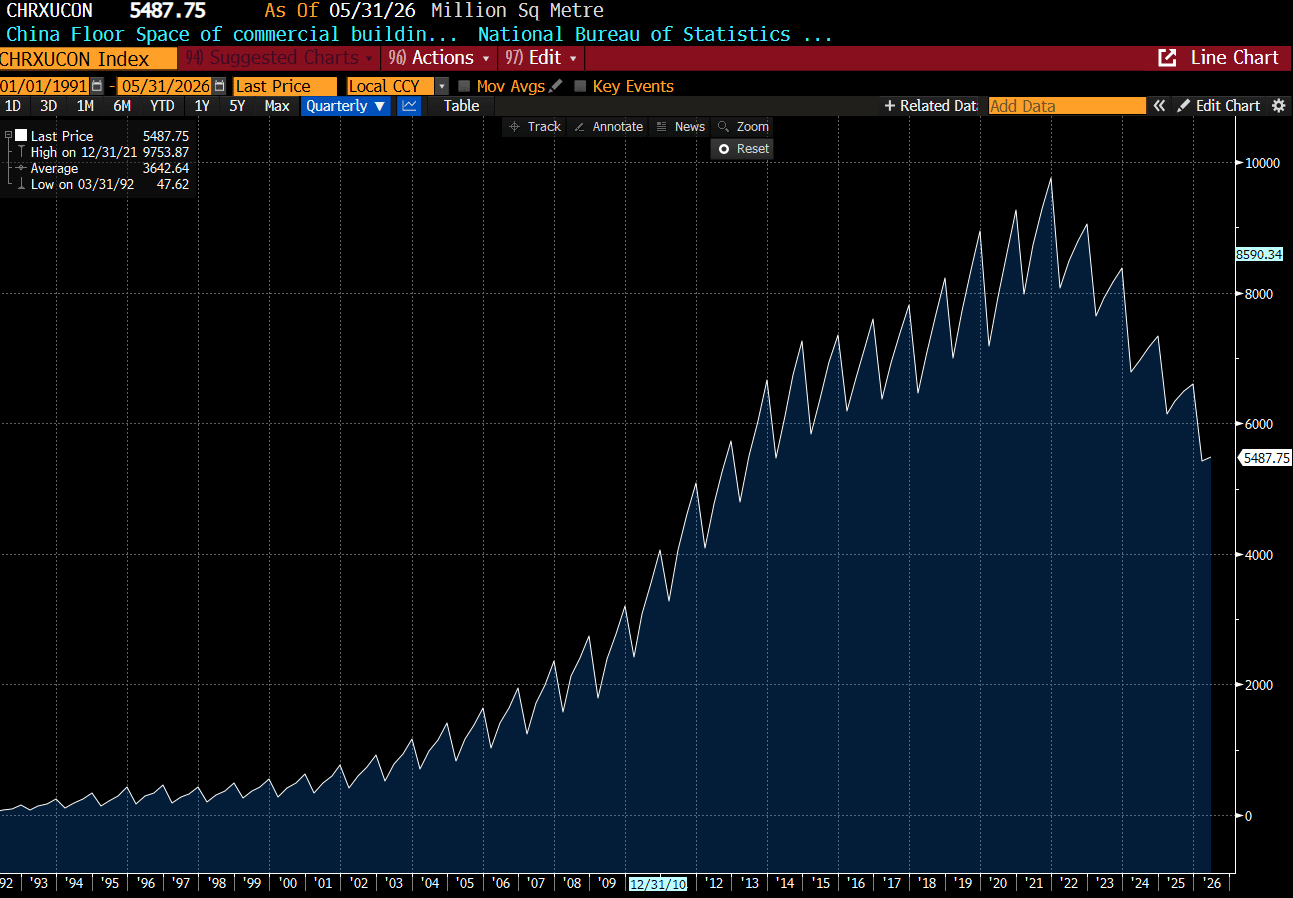

Looking at this note from 2013 (which I reposted because the data is chore to find, and putting on Substack means I will be access it for ever), the implication would be that China is about to enter a financial crisis of some sort. China devaluing would be very negative for GLD/TLT - so it stuck me as a good note to repost. All the crises above were in part property/financial crisis. China has already seen a slow down in construction.

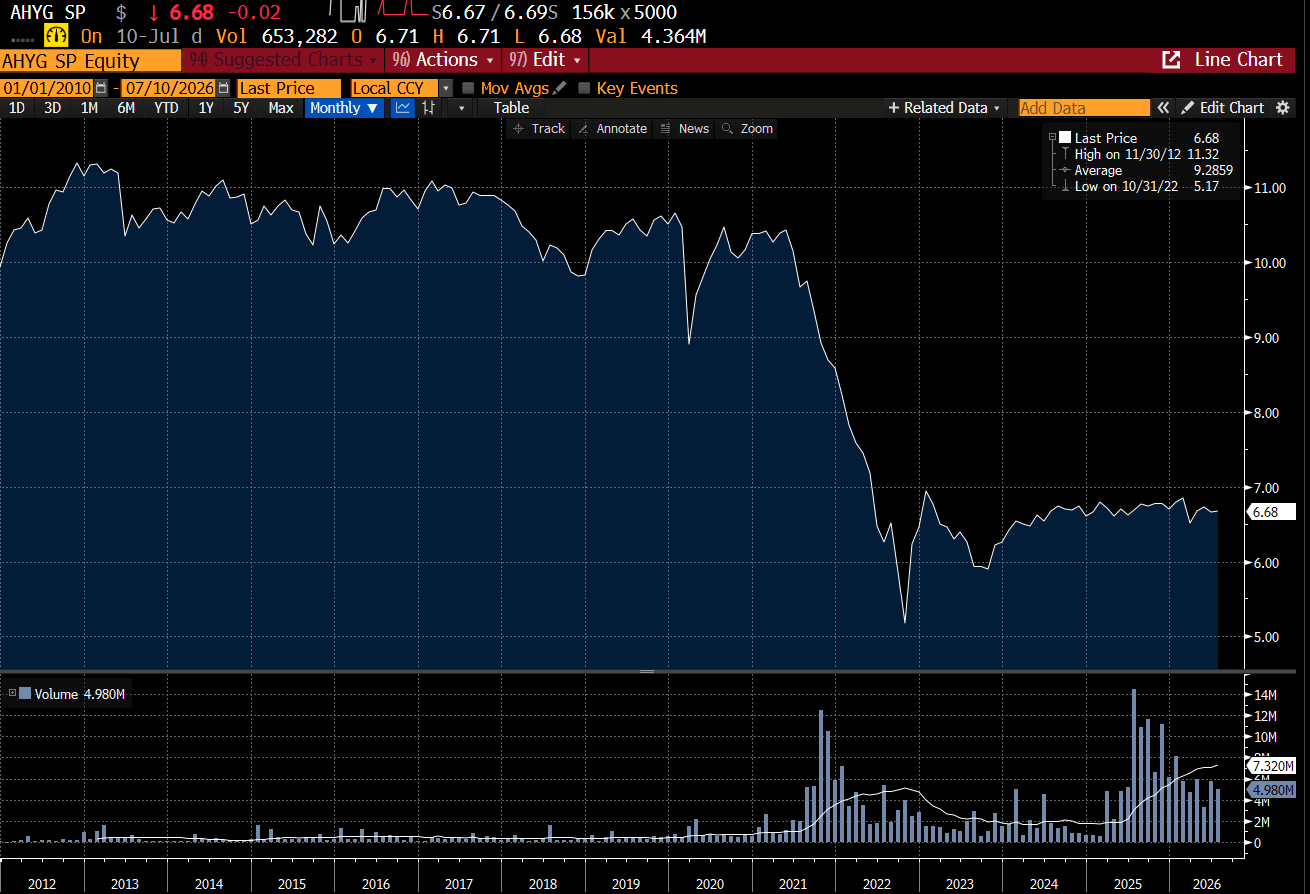

And the Asian High Yield Market was very poor in 2022, mainly driven by Chinese debt problems.

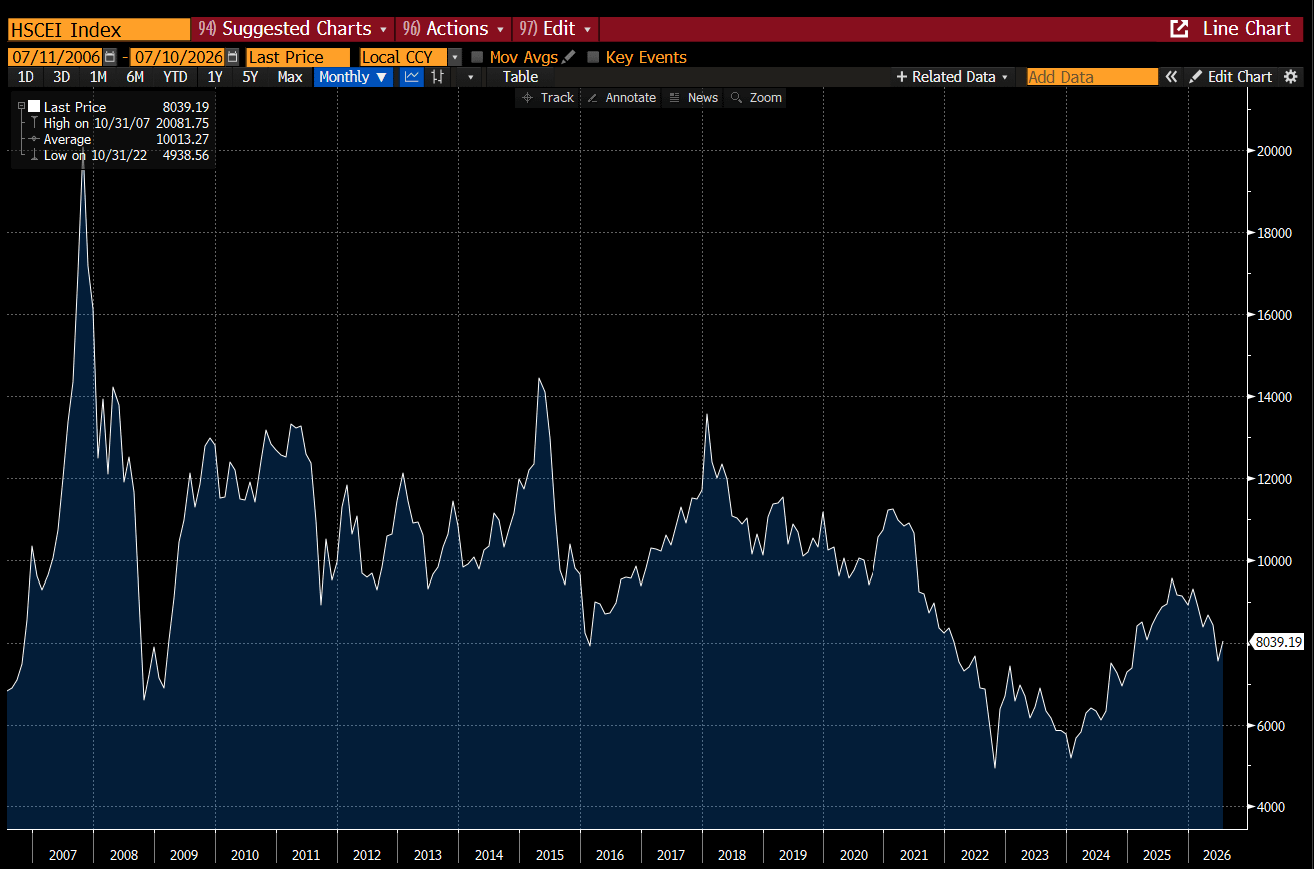

The HSCEI Index has been very poor since 2007, reflecting these problems.

But the Chinese Yuan has been strong this year in contrast to Japanese Yen or Korean Won. Could Chinese buying be signalling a potential devaluation?

Here is where I reflect on how much the world has changed from when I first wrote this gold note. Back then I would be convinced that Chinese gold buying was a sign of trouble. But now, in the modern world we live in, I think it reflects the political world we live in. In the 1990s and 2000s, central banks were sellers of gold, and the lack of tariffs and industrial policy make devaluation a popular policy choice. But today, what would a Chinese devaluation solve? Nothing, as almost certainly tariffs would follow. And with trust in the US ebbing, central bank act at buyers of last resort for gold - just as they used to do with treasuries. A changed world indeed.