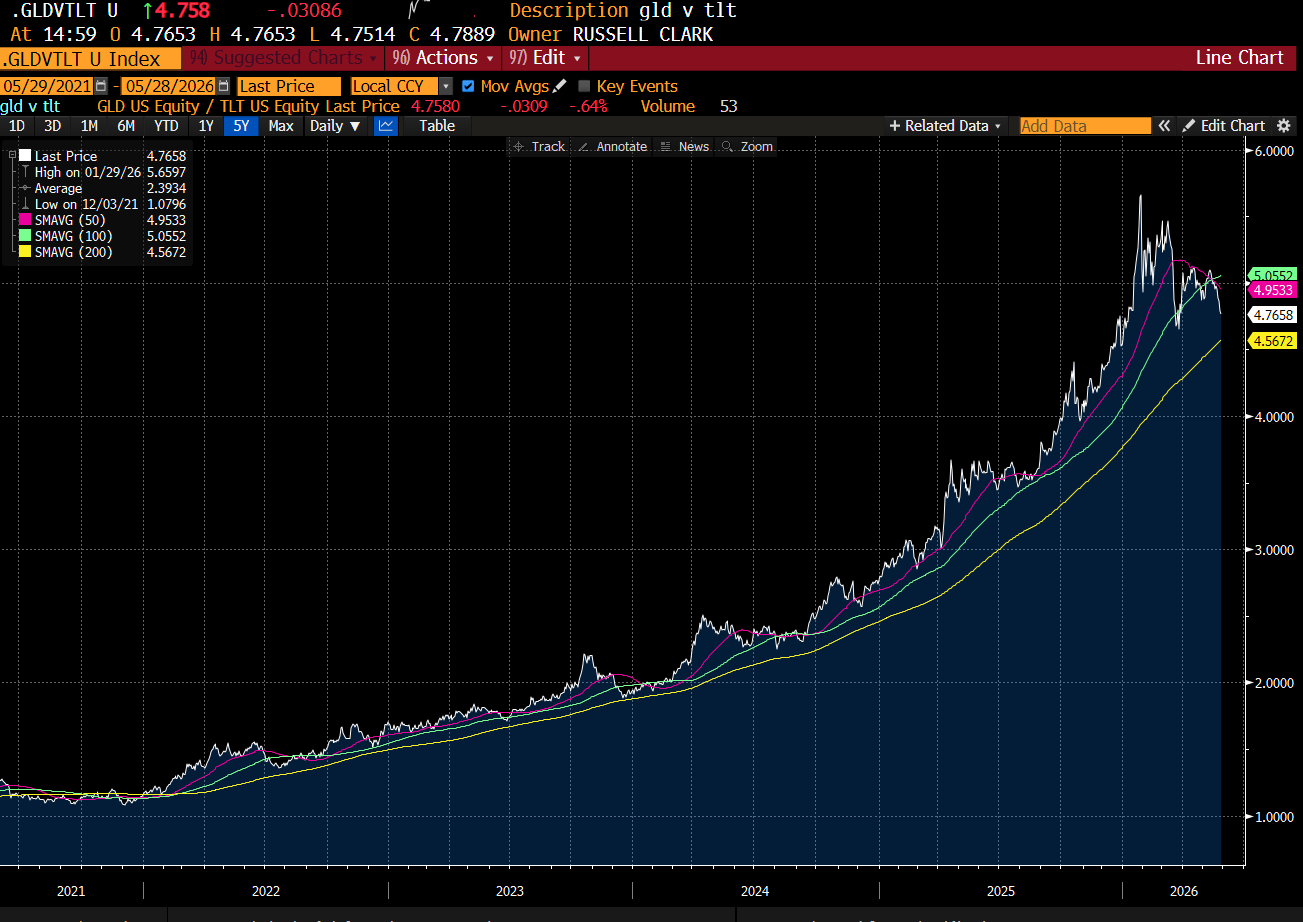

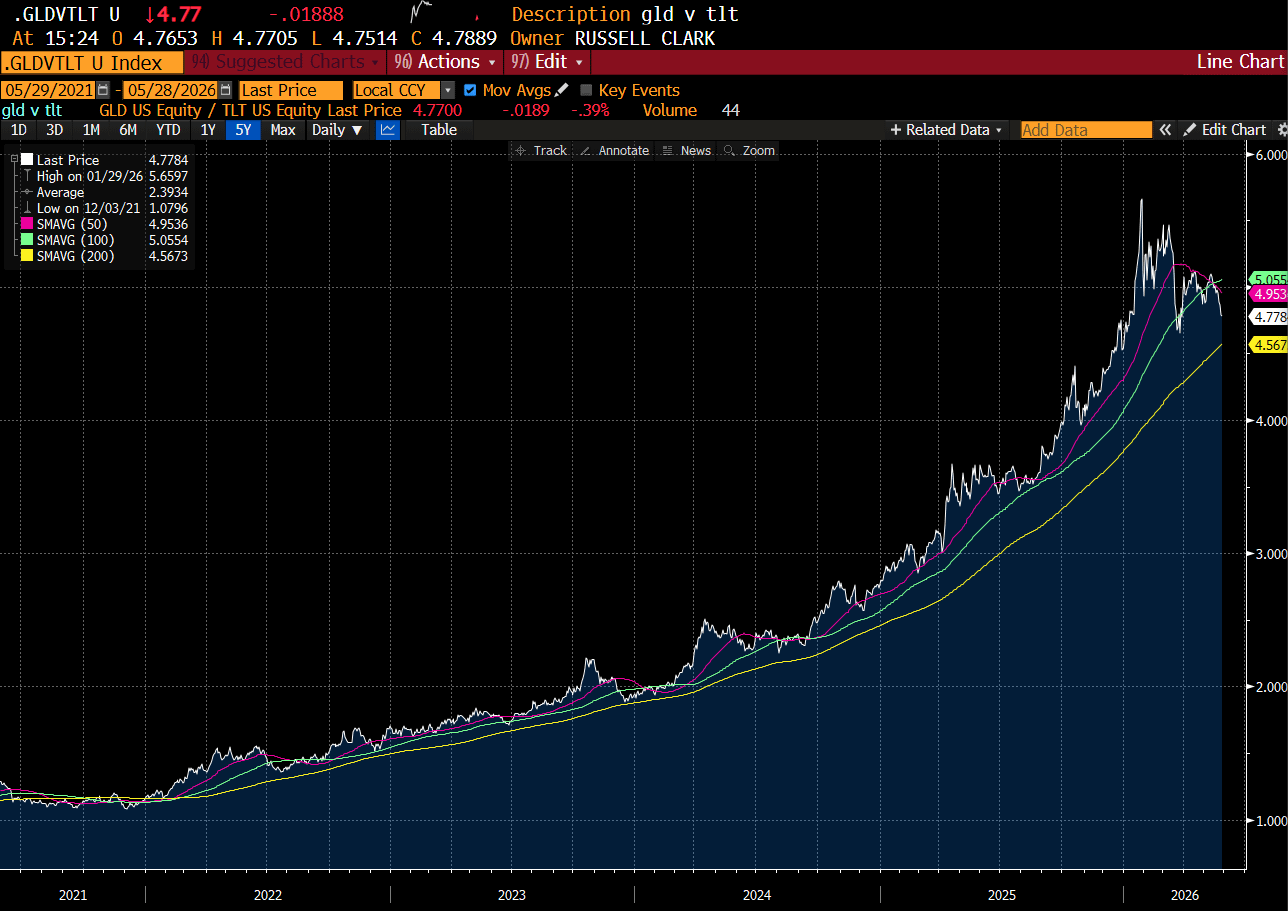

I had lunch with an old client a few months ago. One thing he said to me was the GLD/TLT was my only idea. A little harsh, but maybe is is the only idea I have been REALLY committed to for the last four years or so. And why not? It WAS a great idea. But since a blow off peak in January it has been going sideways.

The really problematic part at the moment is gold. For the first time since 2024, its threatening to break below its 200MDA.

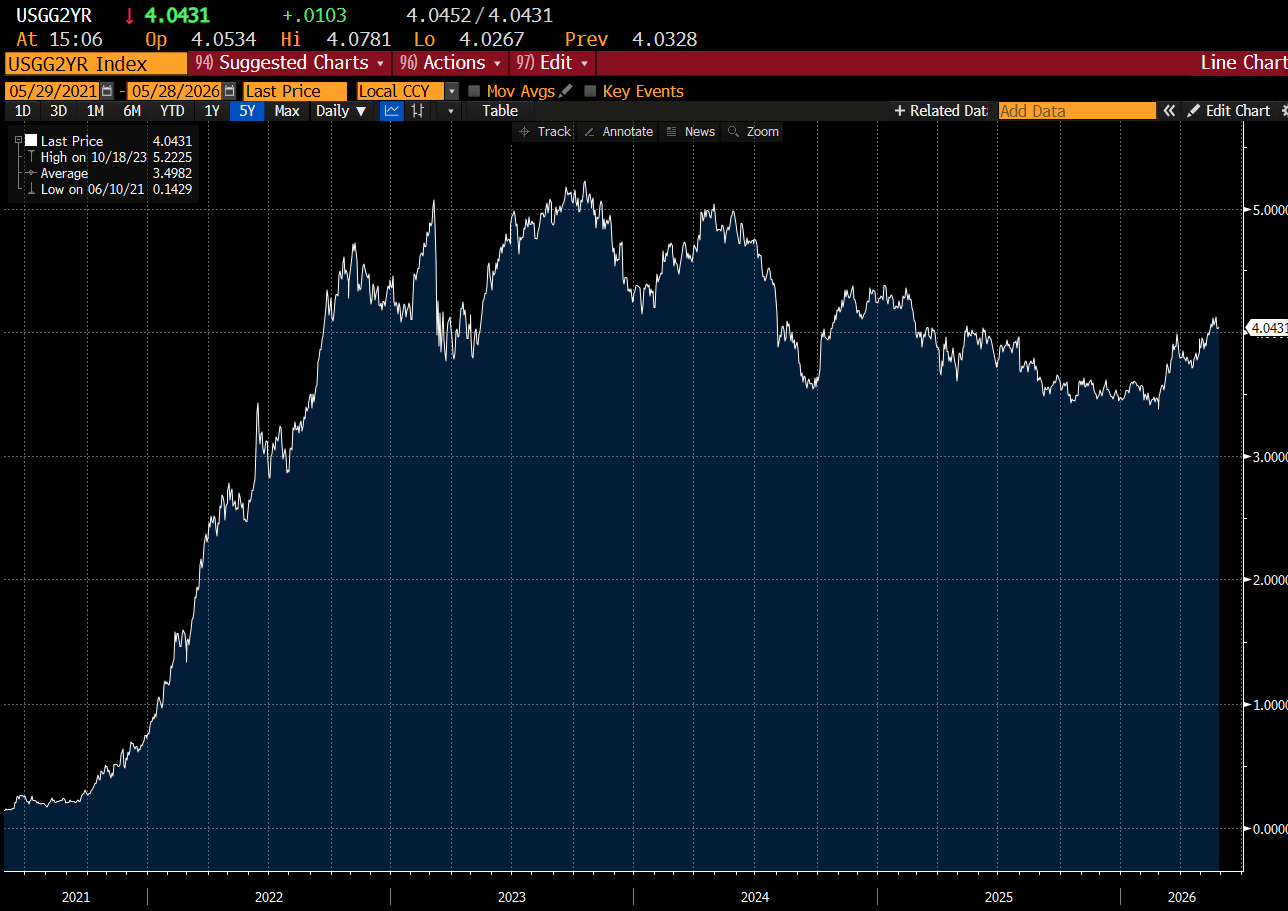

If I had to put a reason to its weakness, it would be almost exclusively with the movement in short term interest rates in the US. Since the War in Iran, markets have been pricing in a more hawkish Federal Reserve (and changing governor as well).

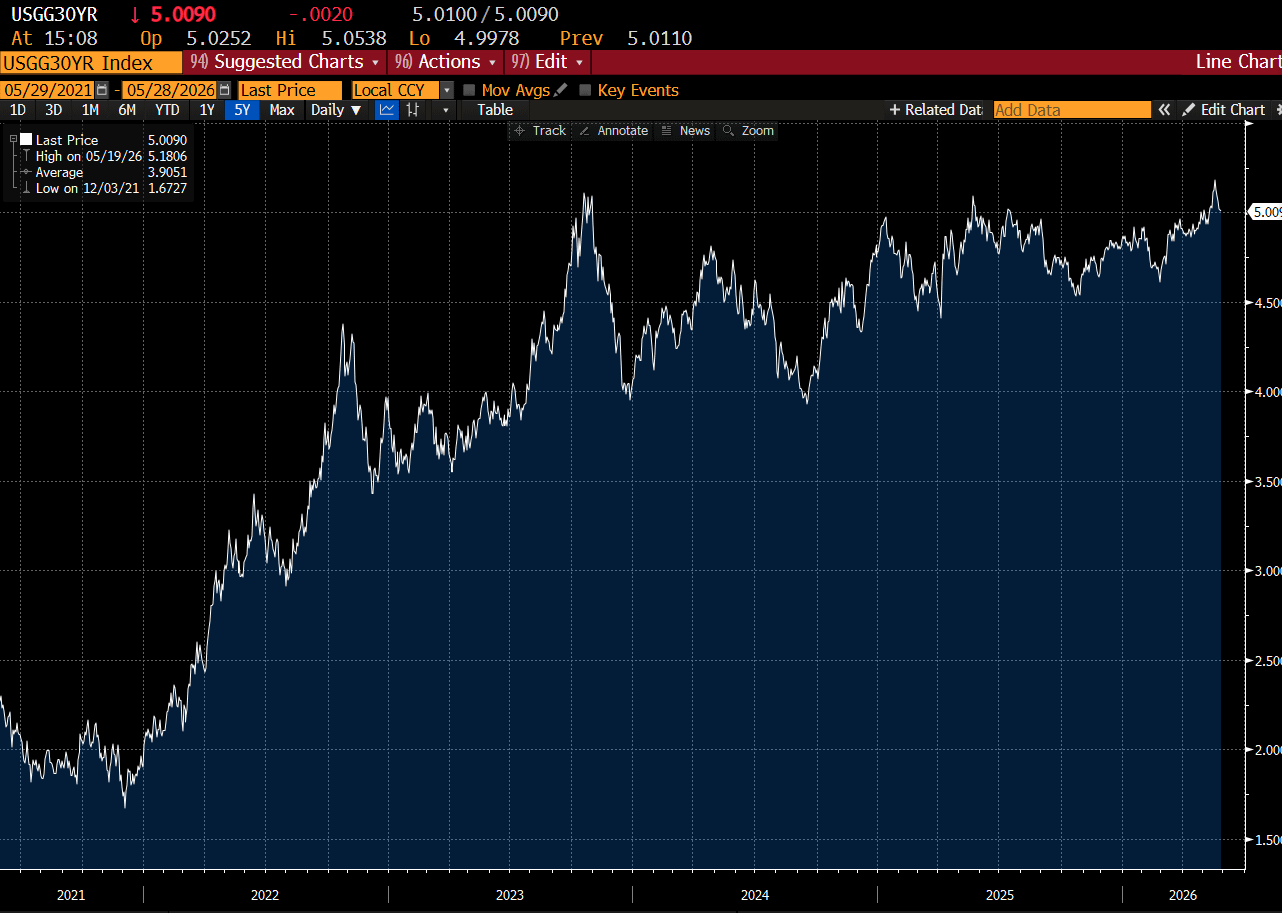

The 30 year has sold off a little bit, which is why GLD/TLT has held up, but we have not had a decisive move lower.

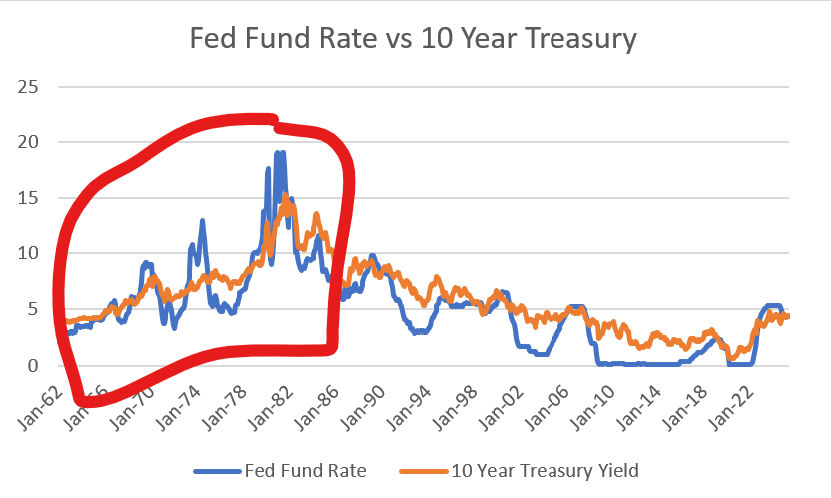

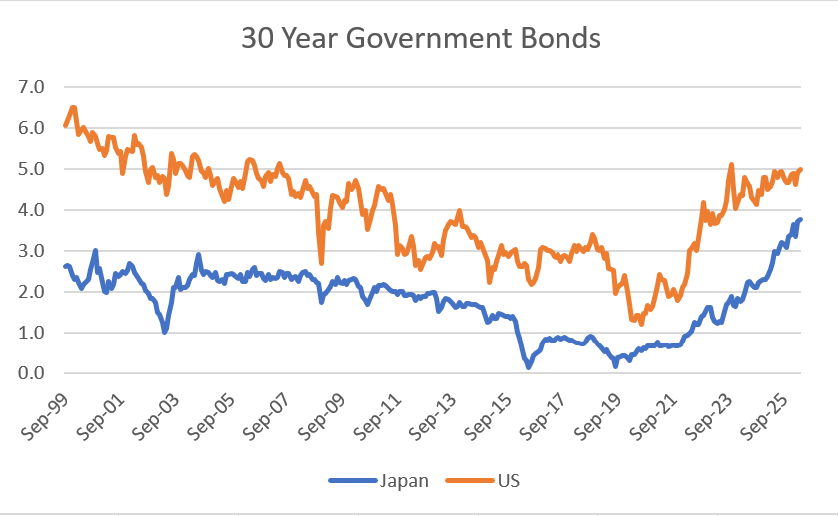

Now in a pro-labour world, I expect the long dated bonds to LEAD the Fed fund rate higher, as it did in the 1970s.

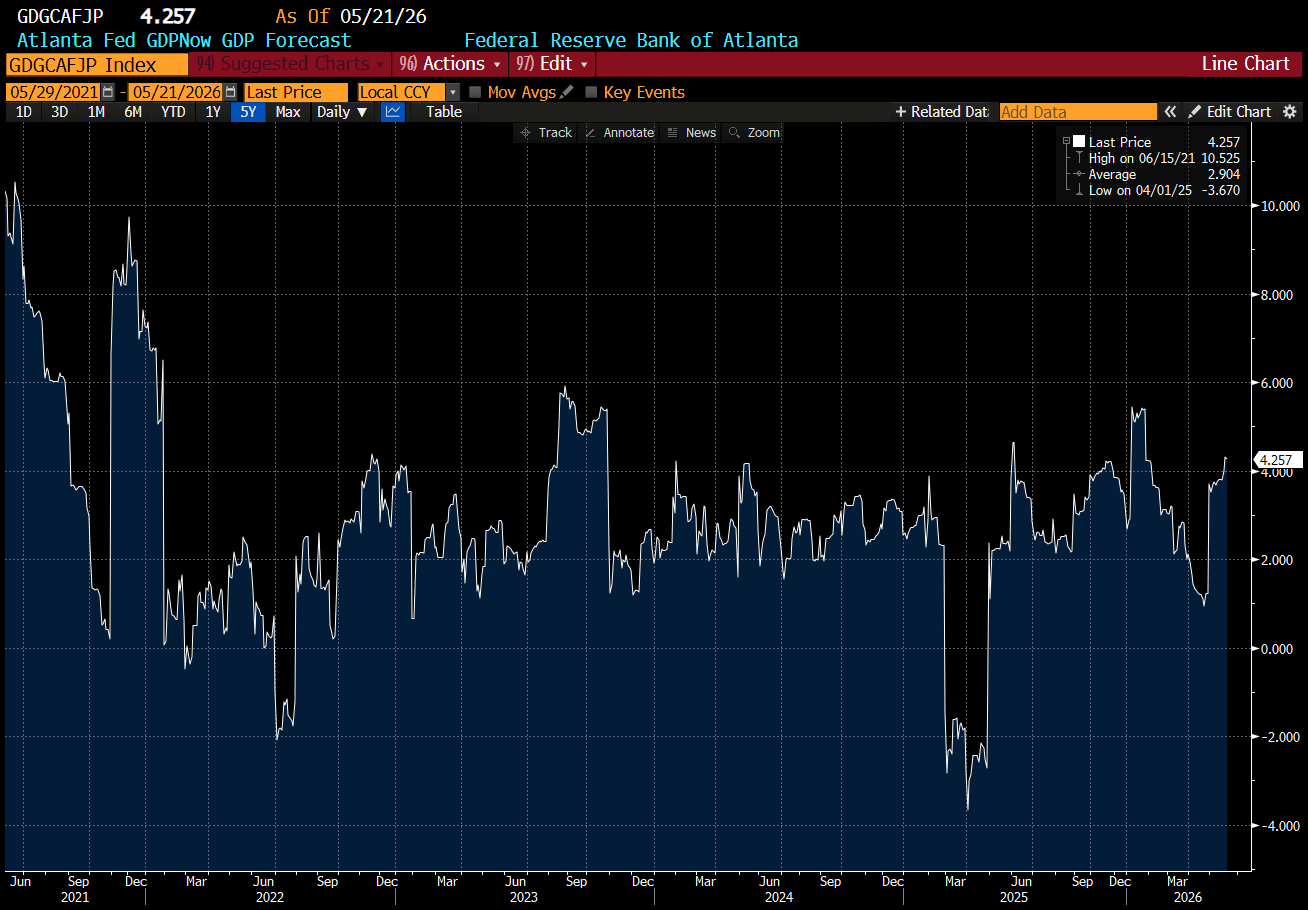

If that line of thinking holds, then I expect the 2 year treasury yield to move higher from here - back to 4.5%, where there 10 year is now, and possibly 5%. Given that the Atlanta Fed GDPNow forecast if 4%, this does not seem excessive.

Looking at the 2-30 spread on US treasuries, it seems possible that 2 year yields could rise another 1% before forcing the back end 30s higher. The 0.7% higher move in 2 years, has seen gold drop nearly 20%. Could another move of a similar magnitude see gold drop 20% again? That would take gold back to USD3,800 an oz, or where it was late last year. The problem would come if the yield curve flattens, and TLT does not fall. In rough number, that would imply a fall back toward 4 on GLD/TLT.

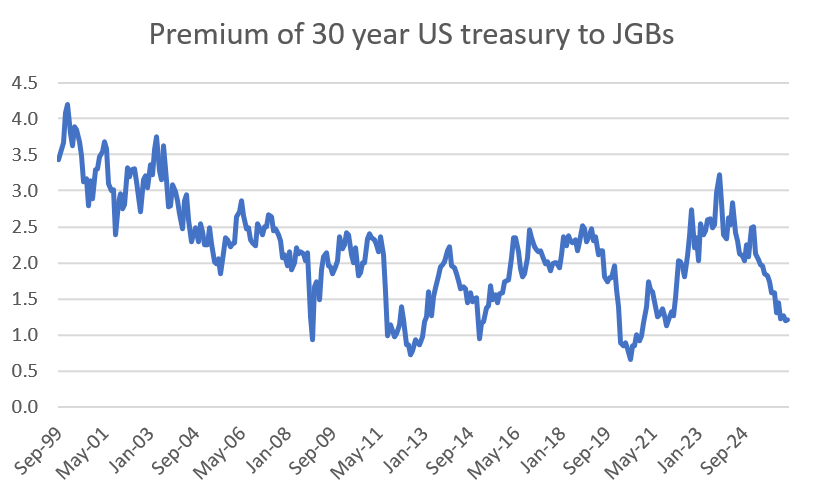

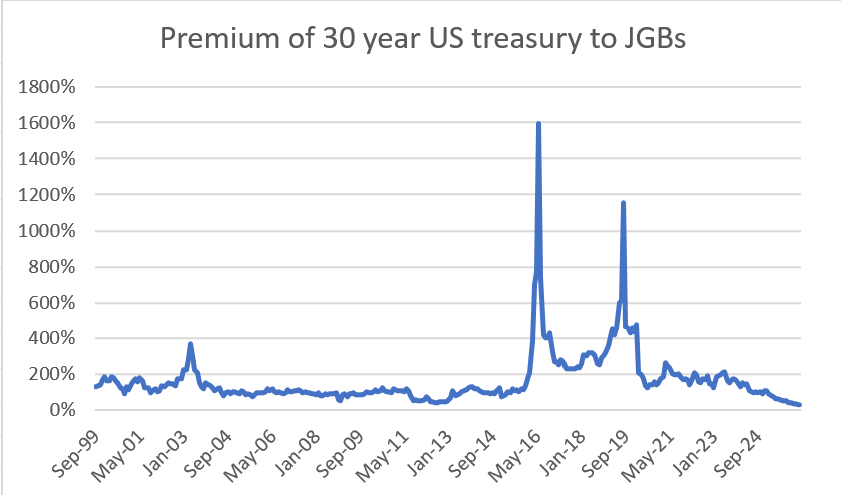

That is the risk if I just looking at market movements this year. Fed Fund rate expectations rise, gold weakens, and yield curve flattens. Against that, US 30 year yields are already trading at one of the lowest premiums to JGBs ever.

In absolute terms, its only just about 1%.

In percentage terms, the gap has probably never been lower. Typically treasuries have been 200% of JGB yields.

IF the gap between JGBs and treasuries were to revert to historical norms, that implies a US 30 year yield of between 6% and 8%.

So this leaves GLD/TLT in an interesting place. If the Fed tightens, TLT could rally and gold fall - which would be bad for a already sideways moving trade. If the old relationship between JGBs and treasuries reasserts itself, then TLT should fall between 20 and 40% (based on TLT having a duration of about 20).

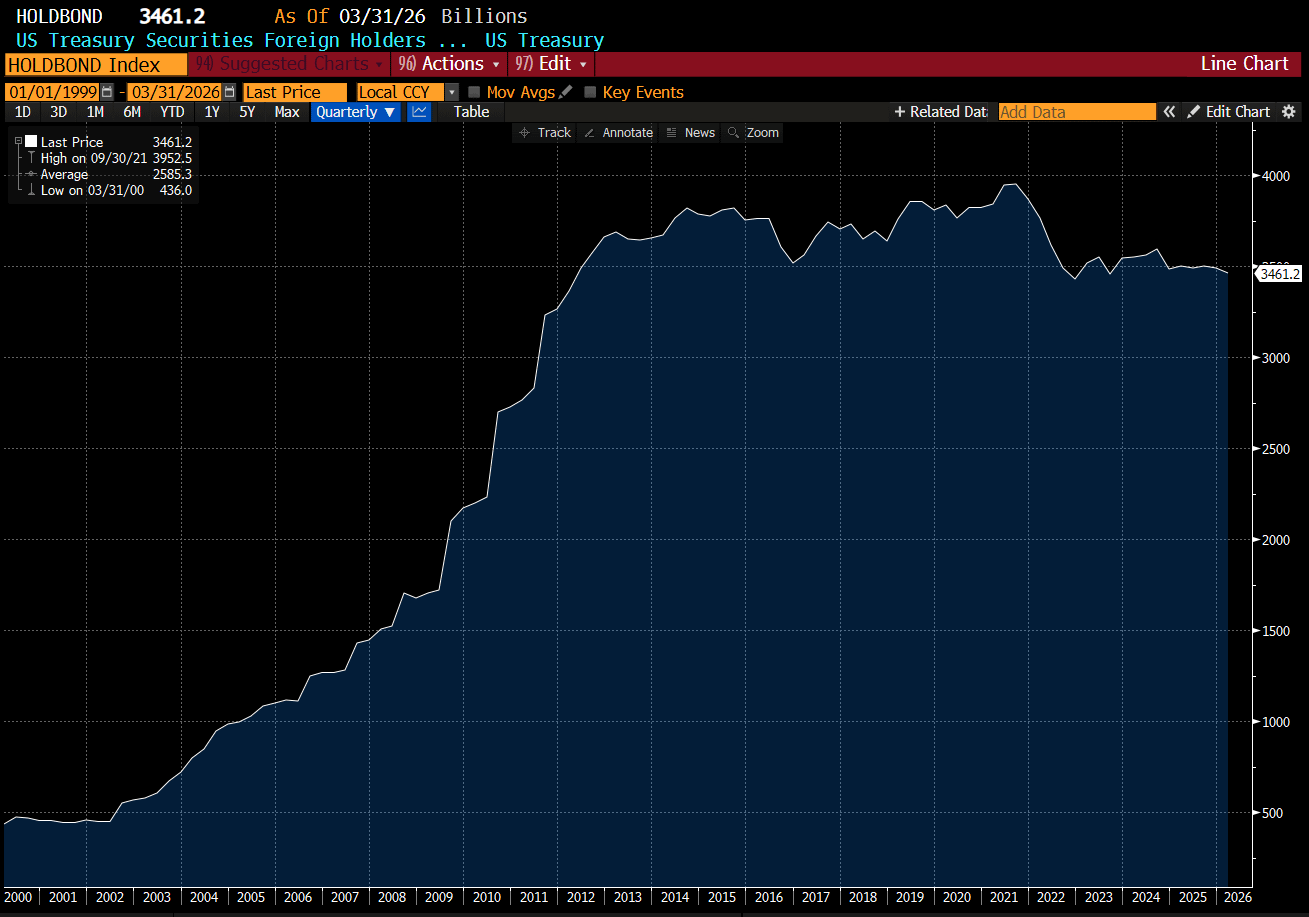

Normally, I do not like 50-50 bets like this. Maybe JGBs yield trade through US treasury yields? It seems odd - but odd things happen alot in this market now. The big kicker for me is that there is still USD 3.5 trillion of official treasury bond holdings out there. Given the freezing of Russian treasury holding - who is buying this debt?

The largest holder is Japan, which needs to sell treasuries to support its currency, and the second largest holder is the UK, which is probably hedge funds doing basis trade, and the third largest is China, which is a seller.

I think it is possible that GLD, and other precious metal do nothing, especially true given the massive retail participation they drew during their run up. But, GLD/TLT still looks good - but mainly the short TLT side.