Back when I first started writing this substack, one of my first questions I was asking myself, was why had JGB yield stopped falling? During the Covid crisis - a huge potential deflationary bust - JGB yields starting rising very early on and have kept going. My view remains Japanese investors are very clued on on inflation vs deflation trends. I wondered what they saw.

One of the first things I found was surging pork prices in China due to the spread of African swine flue.

The funny thing about African Swine Flu is reduced demand for grain initially, as the herd was wiped out, but it would definitely lead to surging grain demand once the herd was rebuilt. Various other problems with Chinese agriculture (polluted land, lack of land, labour and water) maybe me think we would see an era of elevated grain prices - and the war in Ukraine convinced me of this even more. Corn prices doubled from 2020 to 2022 - but rather than stay elevated, they fell all the way back again.

I pretty much gave up on the food inflation trade - but a funny thing has happened. Food inflation has continued to soar. Japanese Fresh Food CPI, definitely has a strong 1970s vibe to it.

Most of Japanese food inflation is coming form vegetables, which Japan imports from China. The stand out is cabbage - up nearly 200% from a year ago.

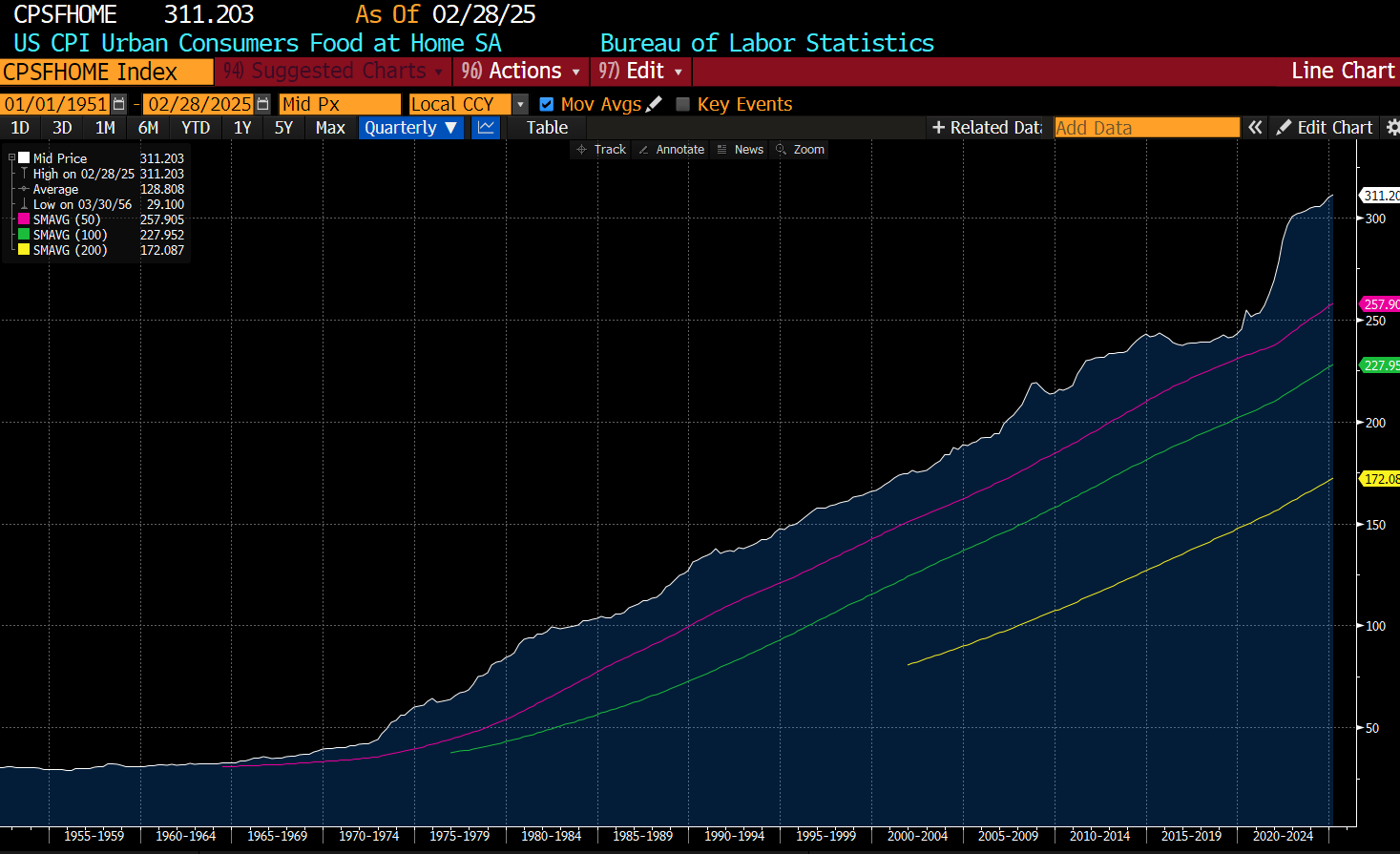

We may wish to dismiss Japan and its cabbage problems as a one off ( I love okonomiyaki - so Japanese cabbage problems feel very personal to me), the US seems to have a food inflation problem as well. US Food At Home CPI is moving higher again.

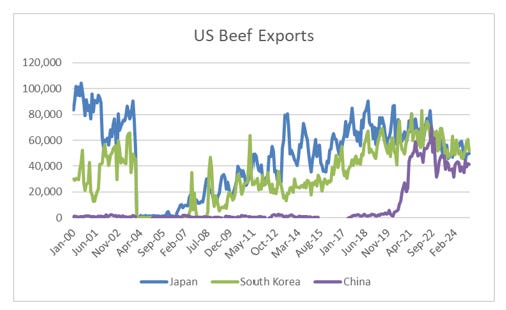

While eggs prices are higher due to avian flu - very quietly beef prices have been moving higher.

In part when pork became expensive, China became big beef importers, on par with Japan and South Korea. But they have maintained their imports, even as pork prices have fallen back. This seems to be putting pressure on the beef complex.

Despite this growth in Chinese exports, the US has turned into a net beef importer. While this seems weird, the US exports high quality beef - but imports huge amounts of low quality beef for hamburgers. The recent surge has been from Brazil.

What I am trying to say, in a very roundabout way, was that China not devaluing, and focusing on maintain real wages, has had an inflationary effect on the rest of the world. But not quite in the shock of soaring grain prices that I expected, but a more insidious tightness in food supply, where prices seem to rise for certain products, but then never come back again. This probably explains why grain related trades, like fertiliser, plantations and tractors have been poor, the food inflation proxy of GLD/TLT has been great.

As they say in fund management - ideas are cheap, execution is everything.