I got my first job as an emerging market analyst because I was cheap. I was a graduate working for UBS in Sydney, and UBS offered a two year program to work elsewhere in the bank with the central office picking up most of the tab. I found a role at GAM in London working on an emerging market fund and away I went. I have been in London ever since. As an emerging market analyst, my boss would ask me to look at banks in a different emerging market every day, so I tried to minimise my work by creating a single huge excel spreadsheet. What I was trying to do was work out if there was any consistency in bank valuations across the world. I created a valuation matrix for each nation, get the average valuation across all banks in that nation , and then compare to various metrics by nation. One result was that market capitalisation to total assets tended to rise with higher return on assets. This should not be a surprise - as valuations and return on assets are different ways of looking at the same thing. I show how it looks today below.

However, I always felt this was a slightly weird way to look at it. During the GFC, and more recently with Silicon Valley Bank, I felt that the quality of the deposit franchise should be where the real value of a bank should be. Or in other words, growing a loan book is easy, but gathering deposits is hard. The problem with this view of course is that deposits are a liability and cost. The relationship between market cap and deposits and 10 year bond yield seems far more random.

This probably sounds abstract. Another way to think about it the value of the top 4 banks in very different markets. I look at Brazil, US, Canada, Australia, UK and Japan. Despite UK and Japanese banks being much larger than Australian and Canadian banks, they are worth less.

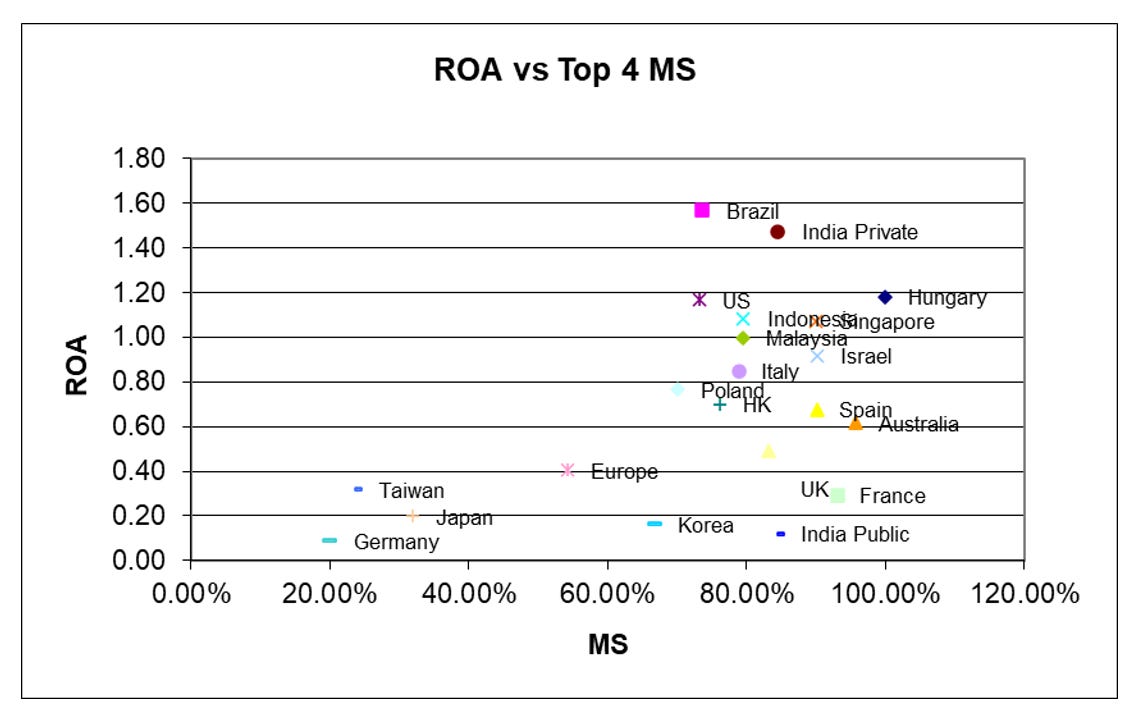

The usual argument for this valuation dispersion has to with market concentration. Broadly speaking that seems correct. Overbanked nations like Germany, Japan and Taiwan tend to generate lower returns on assets.

But with the recent failure of Silicon Valley Bank, and my view that politics is turning pro-labour, I wonder if bank dynamics are going to change?