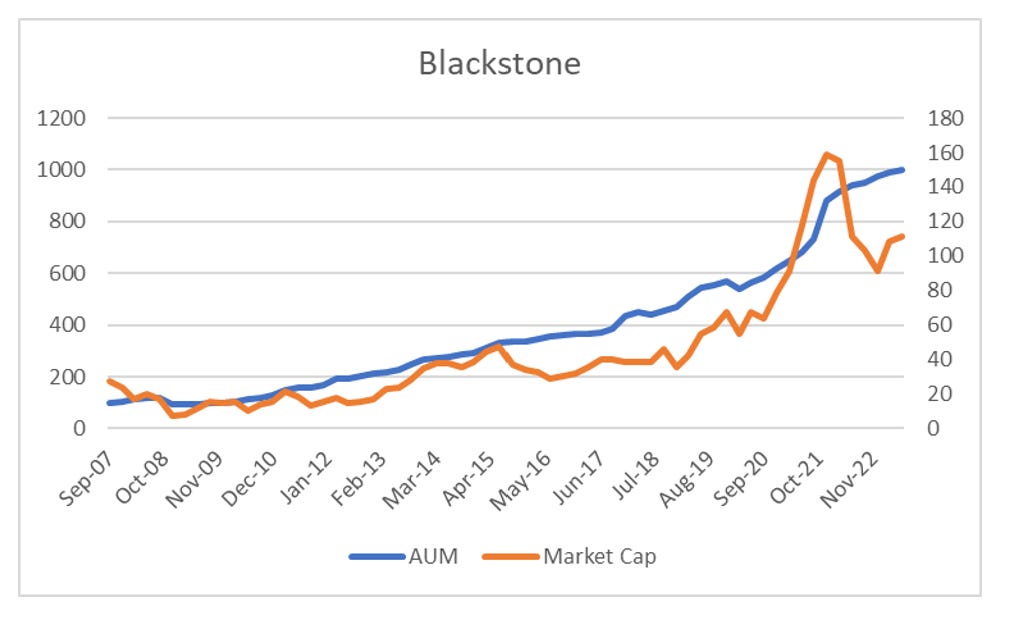

If you have been following recent posts, I have been surprised at the continued growth in AUM for private equity. In fact based on AUM growth, alone, I would probably have to pitch Blackstone as a buy.

Dividing market capitalisation by AUM gives a range for Blackstone of between 20% and 8%. At current levels of 11% is not a bad valuation if you believe in the promise of private equity.

However, one of my theories was that rising interest rates would enact a double whammy on private equity. The first was that when investors can get 5% in short rates, they would lose interest in private equity. Using the Q2 2023 Bloomberg Private Equity Chartbook, we can see that publicly reported commitments to private equity has fallen significantly, with 2023 only annualising at USD28.4bn, well down on a peak of USD120bn in 2017.

The fall in public commitments to private equity is hard to match up with Bloomberg numbers that USD 144bn in private equity funds closed in Q2 of 2023 and that Blackstone has just closed a USD30bn fund. Blackstone was the biggest fund to close in the quarter, Blackstone Real Estate Partners X LP at USD 30bn. The X in the name refers to this being the 10th fund in this series. Like movie franchises, private equity, like to continually relaunch the same fund.

The idea is that investors shift from one fund to another fund as one opens and then closes. As Blackstone shows in its presentation, there is always an open Blackstone Real Estate Partners (BREP) fund. The question I wonder here is how much new money went into this. This could suggest that there is a lag to money flows into Blackstone. As well performing funds roll off, there is natural AUM as money is rolled in. This would imply that if interest rates remain high for a few more years then we will begin to see this AUM fall.

Taking a closer look at Blackstone, the first thing to note is that there is a very big difference between total AUM and Fee-earning AUM. Over 25% in Blackstone case, with total AUM at USD 1 trillion, while fee earing AUM is USD731bn. The second thing to note is that Real Estate is a much bigger AUM on a fee earning basis.

Blackstone has a number of permanent capital strategies which have tilted the firm even more aggressively towards real estate. The Blackstone Property Platform (BPP) with USD71bn and Blackstone Real Estate Income Trust (BREIT) with USD68bn make of 20% of fee earning assets, and half of the fee earning assets for Real Estate. Blackstone Infrastructure Partners (BIP) is listed and is down 16% this year

The Blackstone Property Partners Platform is not particularly transparent to me. I can see there is a USD 15bn European part of the platform with listed bonds. Predictably these bonds have been poor, which I would assume should be negative for this business. Most listed European property funds have been extremely poor over the last year.

The Blackstone REIT with USD 67bn of assets, which would make it one of the largest REITs in the world. Why has Blackstone entered the REIT market? Well a quick look at the fact sheet provides a pretty clear reason - they have been able to jack up fees. Listed REITS have no performance fee, BREIT does - at 12.5% of annual return.

Blackstone has been aggressively pursuing the idea of taking listed REITS and making them private. Blackstone M&A in the REIT sector includes PS Business Parks for USD5bn, American Campus for USD 13bn, Preferred Apartments for USD3.6bn, Bluerock Growth for USD2bn and QTS Realty for USD 5.3bn. Not all of these have ended up in BREIT - in particular QTS Realty looks to be in a different fund. BREIT has large exposure to rental (including student) housing in Florida and Texas.

One of the selling points of private equity is that valuations are more stable. So in the case of REITS, by taking them private pension investors have no need to mark to market. For this “benefit”, Blackstone is able to charge a performance fee. The weird thing about this, is that investors are charged a fee for reduced liquidity. When BREIT was hit with redemption requests, the fund gated.

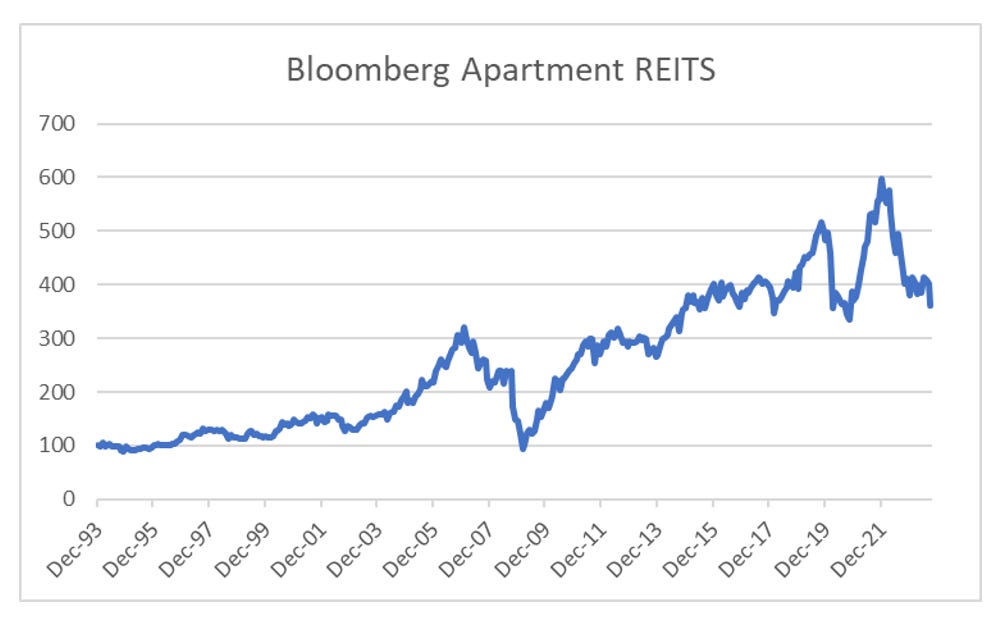

Looking at the performance of listed apartment REITS, I find it hard to believe that redemption requests are likely to go away.

Bloomberg Private Equity data shows slowing flows to the sector, and Blackstone’s two largest permanent capital structures should be seeing financial pressure and/or redemption pressure. So how can AUM still be rising? And why are Blackstone shares holding up so well. Well it seems that underlying collateral values remain strong. Despite rising interest rates, US house prices have risen to new all time highs.

To be fair to private equity, part of their appeal is that the stability of their valuations is an attraction. And as property prices and collateral values are still rising, its hard to argue that the valuations of their funds have necessarily taken a hit. But rising property prices imply still rising inflation pressure in my mind, and hence rising interest rates. To my mind a short Blackstone position makes sense as either inflation and interest rates keep rising, or collateral values start falling. Neither of these will be good for Blackstone.