The basic view I have is a world that is moving pro-labour and away from capital friendly policies. De-globalisation, anti-immigration, anti-free market are all pro-labour policies in my view. One observation is that rapidly rising food prices tend to cause political change. US food prices remained under control until 1970s. This caused a big political change from the 1980s onwards. We seem to have entered a new era of rising food prices.

To capture the change, I have a a core trade that is long gold, short treasury trade. This has worked well. The idea is that WITHOUT much higher interest rates, inflation will run amok. That is if TLT rallied, then GLD will rally. This part has worked.

I had assumed the bear market in bonds would lead to a change in leadership in markets. There are definite signs of this. The bear market in bonds has seen Japanese banks outperform the broader Japanese market for the first time in 14 years.

The Eurostoxx 50 has also seen banks make up 3 of the best performers this year, Unicredit, BBVA and Santander.

US stocks HAVE struggled with a rising rate environment. The equal weighted S&P 500 has been sideways since 2021. And US banks have underperformed Japanese and European banks for the first time in a long time.

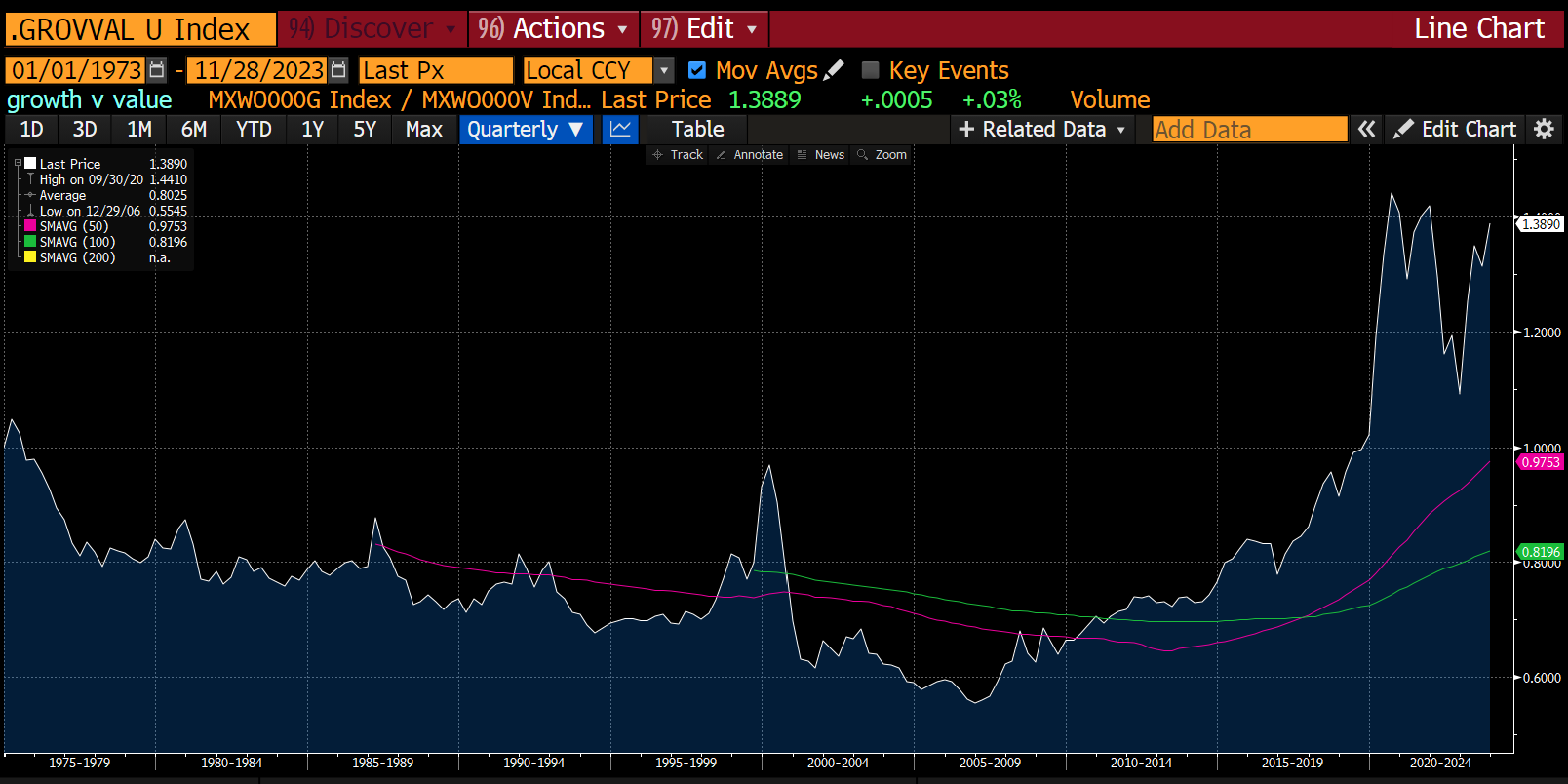

Where I have been wrong is thinking that we might see the underperformance of “growth” stocks versus value stocks. This has not happened, largely driven by large cap tech.

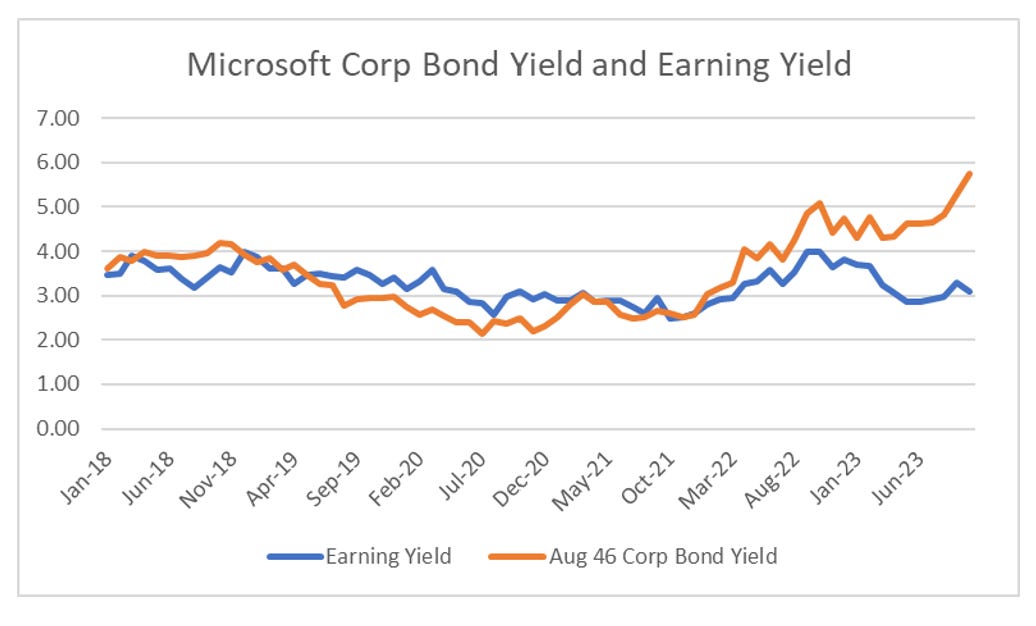

Where I have been wrong has been the willingness of companies to carry out share buybacks at valuations that make little economic sense. If Microsoft’s earning yield had followed its bond yield, the stock would be much weaker.

I had also assumed that the Chinese example of regulating tech would be followed by the US. This has been plainly wrong. One argument in favour of US tech is that US elections are so expensive, politicians in the US cannot afford to take on big corporations.

I have also been wrong that wage inflation would drive commodity inflation. Grain prices for example have been incredibly weak. US corn prices have given up almost all the gains seen in 2020 to 2022 period. So commodity price increases are not necessary to drive inflation. Wage increases are sufficient. That is I have been wrong to be bullish on other commodities, other than gold.

On currencies, I have been surprised by the strength of the Mexican peso. It would seem that the size of trade flows seems to determine economic power. Trade policy determines who gets the benefits. US is still by far the largest importer. This seems to allow the US to set the terms of trade.

US trade policy benefits Mexico over China in recent years, which has reversed a decade long trend of a weaker Peso versus the Chinese Yuan. Historically I would always have chosen Yuan or Yen over Mexican peso - but US policy seems to be the dominant driver.

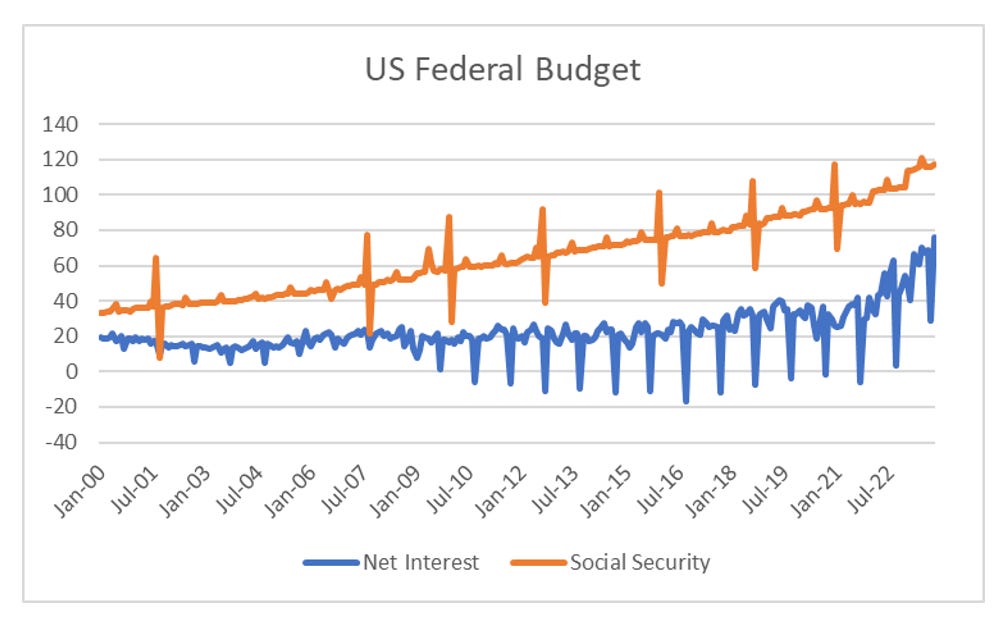

Structurally I am bearish on bonds. I think inflation is going to be entrenched, Where I could be wrong on bonds is the but I am sympathetic to a politically bullish argument for lower interest rates. That is the US government cannot afford higher interest rates. The interest bill on the government debt it already closing in on social security as the biggest expense.

Politically in a pro-labour environment austerity is dead. Hence, I have to think that corporates are the most likely source of tax revenue. Both right wing and left wing governments have shown their antipathy towards large corporates, so I am going to continue to avoid them, and stick to my long GLD, short TLT trade.