Back in the free market era (circa pre 2016) autocallables (structured products in Europe) were guaranteed time bombs in financial markets. Essentially, they sold volatility to create yield products. In calm markets, they artificially reduced market volatility, but in crisis markets they amplified market volatility. Originally invented in Japan, they cost retail investors so much market, they eventually fell out of popularity. Korea is now the financial mecca of equity linked autocallables. If you want to know more - see the autocallable and volatility tab on my home page. I have had a few investors ask if there is any risk they blow up with this sell off. So I will present the most recent data I have on Korean autocallables, and allow you to make up your own mind.

Typically spikes in VIX coincides with a fall in autocallable issuance, as happened in 2015 (China devaluation fears) and 2020 (Covid). We saw a drop off in issuance as interest rates rose in 2022, but over the last year issuance has been relatively strong.

In February, the most popular equity linked products are below. Kospi 200, Eurostoxx 50 and S&P 500 are the most popular indices, with Samsung Electronics (#3), Nvidia and Tesla being the most popular single names.

Are we at risk of triggering a volatility spike with any of these popular names? On the KOSPI - we can see the dividend futures remain lacklustre - which is a neutral sign.

Kopsi Volatility does seem to want to break higher which would be negative for markets.

Kospi 200 has not hit a new high since 2021, which would imply there is large amount of volatility selling going on. The future direction of the Kospi market is largely determined by two stocks - Samsung Electronics and SK Hynix - both semiconductor plays. Of the two, SK Hynix (lower chart) has benefited from recent enthusiasm for AI plays.

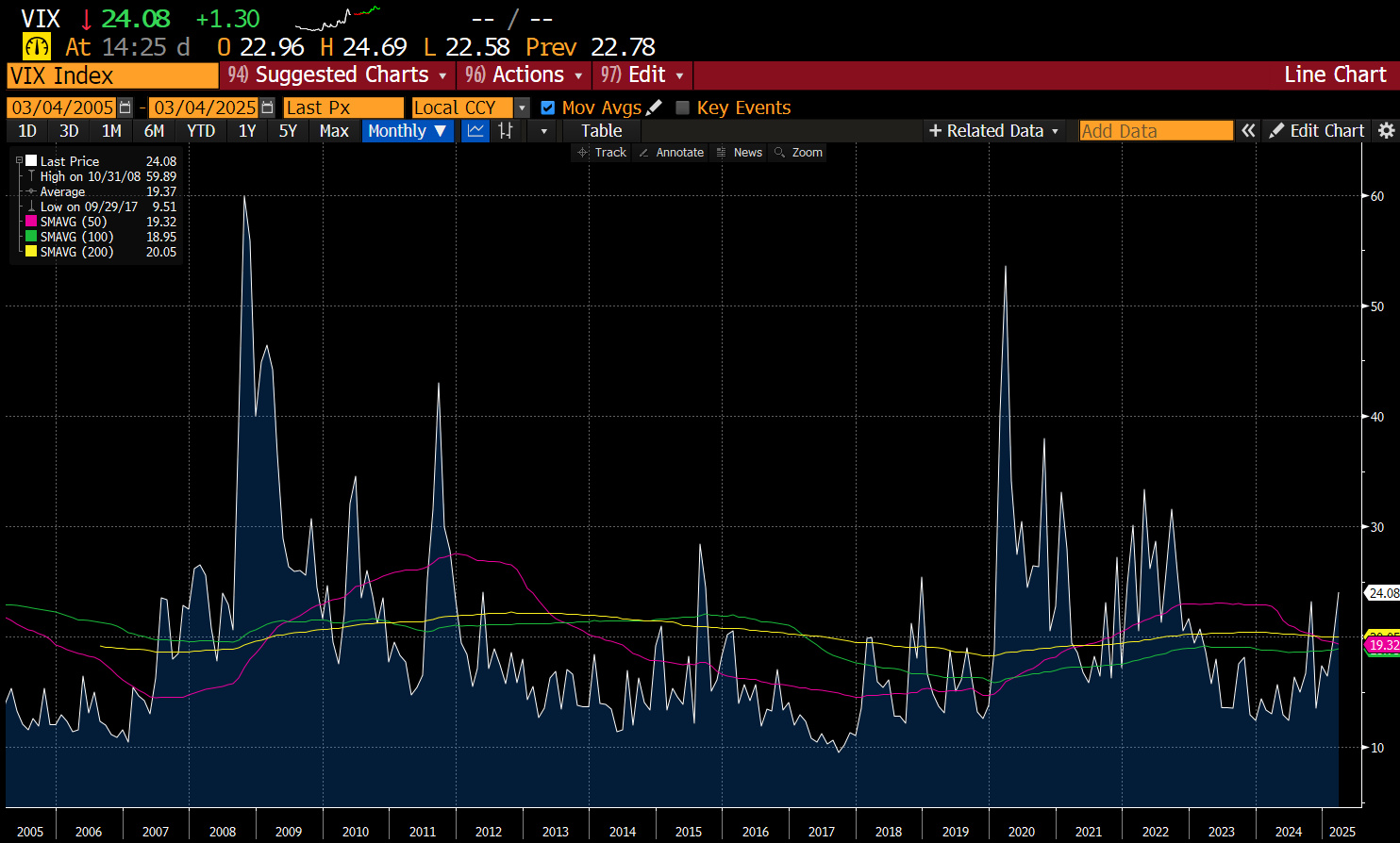

I would say there is definitely some risk to the autocallable market from weakness in the Kospi 200. S&P 500 and Eurostoxx 50 both tagged new all time highs recently, which makes the risk of a blow up here less. But when I see 8mth generic VIX (UX8) turning higher, downside risk to the markets tends to be elevated.

On an individual stock basis, clearly there is risk in Tesla. Should it break 200, I would expect some problems in the autocallable markets. Typically autocallables are sold with a round number barrier 50% below spot where the banks can return risk to retail - so with Tesla trading around 400 early this year - 200 would be a likely barrier.

So there is a chance of an autocallable blow up, but with VIX already at 24, the risk reward of a long VIX trade is very tricky here.

What does look under-priced is corporate debt spreads. If you think autocallables are about to have an even, then corporate debt spreads looks far too tight.

In my view, I think it is correct to worry about market and corporate debt valuations - and maybe autocallables makes things worse, but will not be the trigger - they will act as an amplifier.