I am a member of club in London that is somehow the best night out in London mid-week, while simultaneously the home of conservative thinking in the UK. I joined for the partying, but recently I have been frequenting this club to access their library of books on conservative thinking. Neo-conservative thinking has never really made sense to me. And as I thought it was not that important, and to be honest, largely discredited after the second Iraq war, something I could safely ignore. But reading Peter Thiel, I thought I should read more conservative writings to try and get an idea of where they are coming from. Intriguingly, it did not take long before the name Strauss popped up again. And even more intriguingly so did the name Hobsbawm. I knew I was on the right track.

Broadly speaking the ideas I took from a 2004 book (not pictured - but very similar version) edited by the “godfather” of neo-conservative, Irving Kristol, can be summarised as thus:

1 - America is a uniquely special nation. It's freedom makes it the natural leader of the world. Any nation that rejects the US as leader will have to define itself anti-US and anti-freedom.

2 - To defend this position as a world leader the US is completely justified in pre-emptively attacking or constraining rivals.

3 - Fiscal deficits do not matter. The US government should spend to create the society that is wishes to have. Spending on people that the government “likes” should be generous. The book specifically mentions pensioners are ideal recipients of welfare.

4 - Multinational organisations are there to limit US power and should be treated as hostile.

5 - Corporations are “good” for the lack of a better word and should be supported.

6 - Conservatism in Europe is weak as they lack the imperial ambition and belief of the US.

While President George W. Bush was seen as a neo-conservative (or at least surrounded by neo-conservative), President Trump is a much fuller expression of neo-conservative beliefs. Under President Bush, the US greatly underperformed the Chinese stock market (to be fair in 2000 - neither China or Russia was seen as a threat to the US), but from 2016 onwards in particular, US equities have massively outperformed Chinese equities.

Many macro and mean reversion style investors see the above chart, and want to buy China, sell the US. And given this how most investors made their names from 2000 to 2010, this is is understandable. But there are so many difference between 2000 and 2024, I am not sure traditional macro analysis works. One example is the US fiscal deficit. It was surplus in 2000, and deficit today.

I think the easiest way to understand the difference is neo-conservative policy is that it aims to reduce power of government as much as possible. The easiest way to do this is to reduce the revenue raising power, and the rise of big tech has meant that a large portion of wealth in the US is now untaxed. Share buyback transfers wealth in the most tax efficient way possible, and the ability to borrow against shares allows owner to avoid selling and realising capital gains tax. Back in 2000, companies and shareholders were much keener on selling shares, hence the fiscal surplus. This also explains why share count for the S&P continues to fall.

One thing about neo-conservative policy is that it is very good for equities (corporates) and bad for bonds. The relationship between SPX and treasuries reflects this strongly in recent years.

Interestingly, Japan is also showing a similar relationship, with equities and bonds going in opposite directions.

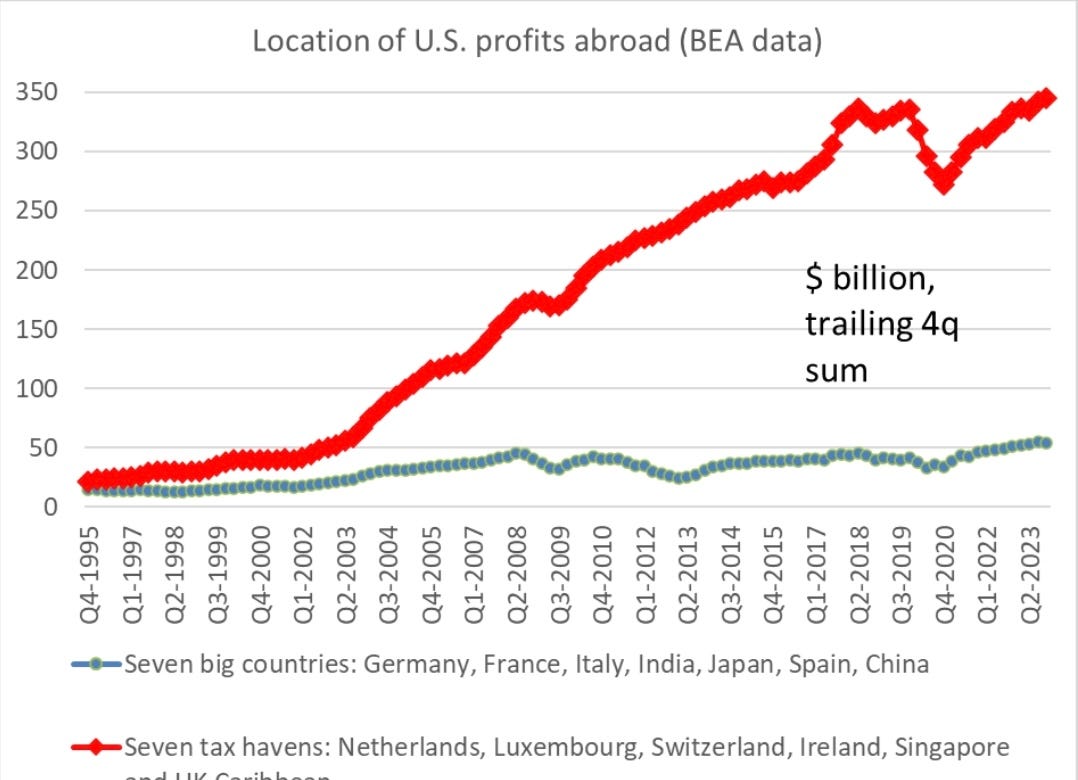

In practical terms, neo-conservatism is anti free trade as it strengthens rivals -Europe and China in this case. One thing that is clear to me about neo-conservative policy is that it is not really “pro-labour”. We have begun to see that with many US consumer facing stocks beginning to weaken as real wages fall. Japan is also seeing real wages fall despite low unemployment. Neo-conservatism is only pro-labour in so much as it is hostile to free trade. That is it does not want its corporates to use China. It is also clear in the use of policy to protect sectors like the tech industry from competition, while not demanding any tax from them - in stark contrast to FDR. Current US tax policy that allows US corporates to avoid taxation outside of the US would fit in with this view.

Neo-conservatism also suggests that active sabotage of other nations is also acceptable. For example, the destruction of the Nord Stream pipeline from Russia to Germany would benefit US natural gas exporters and harm both the Russian and European economies. There is of course no proof of US involvement- but it would be one of the few nations with the ability and motive to carry out such an operation.

So what are the risks to current neo-conservatism economic policy. There are numerous, but so far seemingly contained. It heightens risk of conflict in the rest of the world (by design). We now have war in Ukraine/Russia and Israel/Middle East. China has greatly increased pressure on Taiwan. This is in many way what neo-conservative policy wants - as it secures US pre-eminence. Even if China is aware that US is baiting them into aggression, politically it is difficult to resist, as American tariffs and other polices strengthen the voices of hawks in China. China now far more frequently violates Taiwan’s air defence identification zone (ADIZ).

Rising conflict globally drives more capital back to the US, which helps fund the US in a virtuous cycle. As a child of globalisation, neoconservative thinking does not come to me naturally. Generally I would take the view that war and conflict should be avoided. That being said, it looks to me like neo-conservative thinking is now embedded totally in the Republican party, and partially in the Democratic party (hostility to China). The Supreme Court also seems very neo-conservative in its view of corporates as “good” and government as “bad”. So neo-conservatism is here to stay for the foreseeable future - particularly after Biden’s horrible debate performance. For me, all the favourite macro, mean-reversion trades look to be a disaster. I see SPX/TLT continuing to do well (government spends to keep corporates doing well, and avoids raising taxes). I see GLD/TLT doing well as war tends to be good for gold and bad for bonds. I see Yen continuing to be weak, as it suits US policy to continue to put economic pressure on China. That is current markets are all being driven by neo-conservative policy. It ends when US policy ends - and politically the chances of that is fading into the distance.