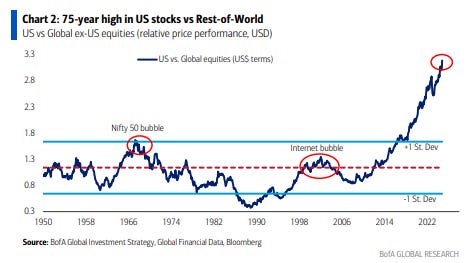

The chart of the relative performance of the US to the rest of the world is truly extraordinary.

It has been very tempting to bet on mean reversion with this graph, and you would have been wrong. I think mean reversion use to work for very simple reasons. For me, equity investing is always about growth. There are two forms of growth as I understood it - one was a new technology taking market share - so tech investing, and then there is the catch up growth as developing markets catch up to developed markets. 1970s & 80s were about Japan catching up the US, the 1990s was about new technologies - mobile and internet - and then 2000s was about China catching up to the world. This is a huge simplification, but broadly speaking how I saw the world work. The simplest way to visualise this is energy consumption per capita. The US and Europe reached peak energy consumption per capita in late 1970s, and has been in decline since. Asia has been the growth story, and Africa always has the promise of enormous growth.

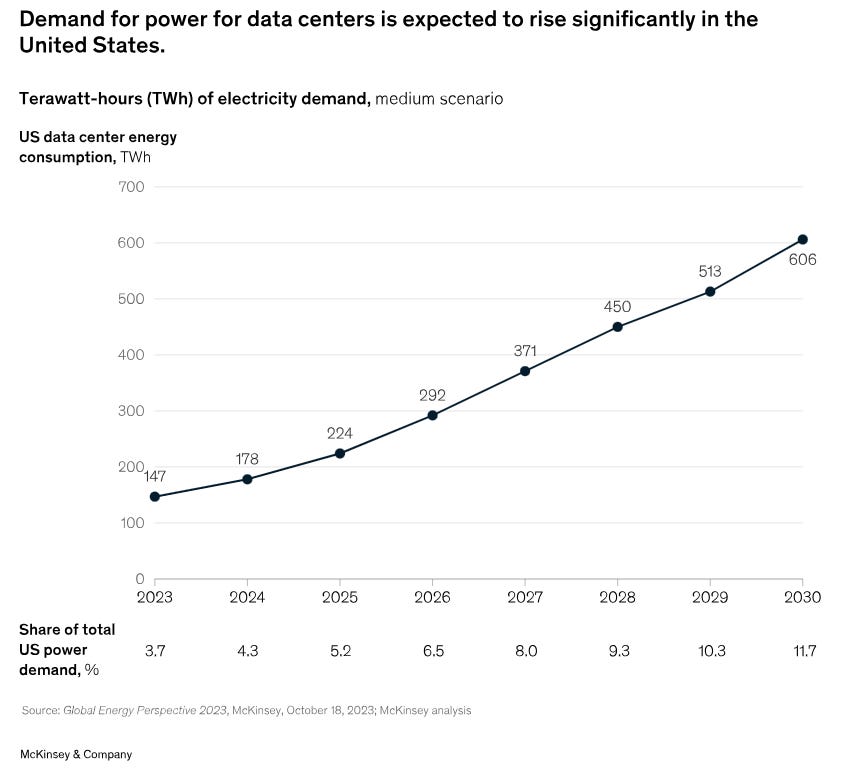

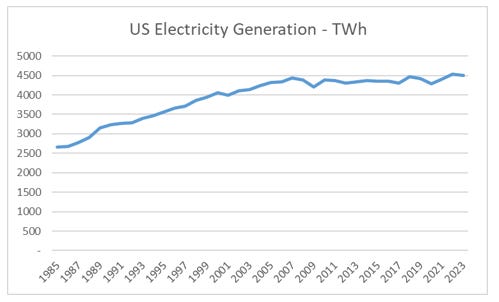

Looking at the above, energy consumption of around 150 gigajoules per capita puts you in the “developed” bucket - or at least a serious economy. You could also argue that development eventually leads to a cap in energy usage. More efficient cars, better insulation, more urbanisation all have negative effects on energy consumption per capita. But a strange thing is beginning to happen. US energy consumption is beginning to inflect higher. McKinsey has cloud computing taking up nearly 12% of US electricity consumption by 2030.

How big is that in terms of total consumption? It should be pointed out the digital revolution has been up to this point good at reducing energy consumption, hence the change in energy consumption trends is a big deal. Despite improving efficiency, growing population mean that US energy consumption peaked in 2007 at around 100 exajoules. The McKinsey numbers show a rise of 459 TWh to 2030 - which is an additional 10% consumption. This would be half of Japan’s existing generation, or 30% more than the UK’s total electricity generation.

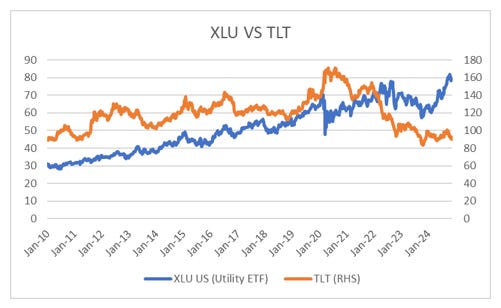

This is already bleeding into stock markets, with the US utilities breaking their historically high correlation to long dated bonds. The market is probably correctly pricing in a new period of growth.

What I am starting to think is that the digital economy is beginning to be as a big a transformation to the world and society as the motor car. The US led the world in auto production in 1920s. I wonder if the Dow Jones index was similar outperforming the rest of the world at that time? All the large car companies and most of the oil companies would have been in the US at that time.

Even in the 1950s, US dominated auto production, but as time went on Germany, Japan and China have all come to be larger producers. That is, there was a natural tendency for nations to catch up as they mastered old technologies. Protectionism and nationalising oil industries also helped to globalise the auto industry. This is where mean reversion occurred.

Looking at the digital world, US companies have a lock on the collection of data (outside of Russia and China), and leading market share on cloud computing. Just as a lock on auto production drove the US to be the biggest consumer and producer of oil, we are beginning to see a US energy consumption rise as well. There are two separate questions here. How much demand for Gen AI will there be? Will we start having domestic robots constantly using Chat GPT to talk to their owners? Will we expect to talk to our computers constantly like Star Trek? Who knows, but the potential to surprise to the upside is there. Secondly, when do the rest of the west realise that they need to nationalise the data and cloud flows they have allowed the US to monopolise? Or does slow growth Europe happily allow itself to subside into meaningless? In the real world, Europe is a huge economic power, but in the digital world it badly lags the US and China. The digital world is eating the real world, and this is why mean reversion does not work anymore.