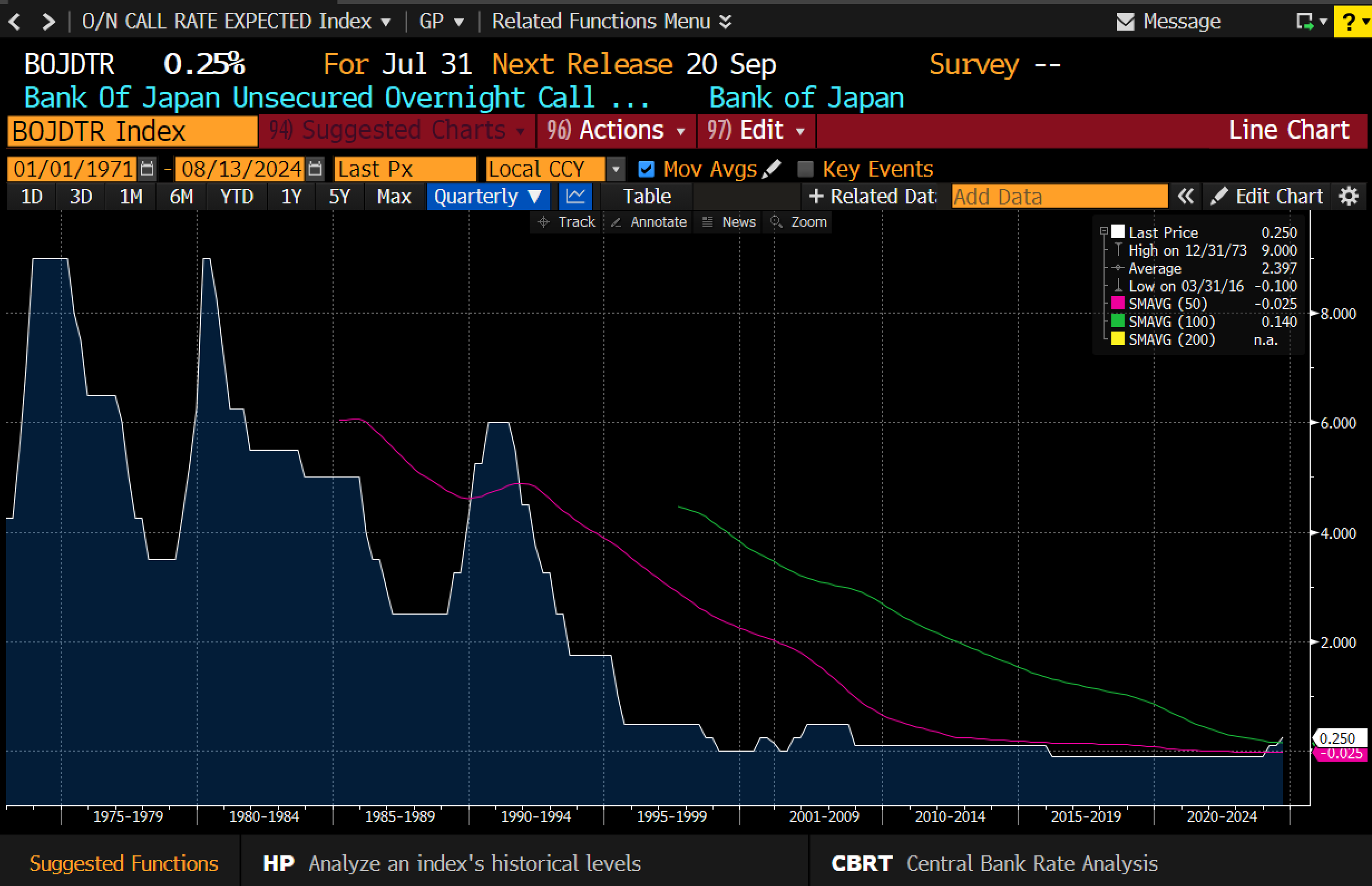

Markets have had a rough month in August so far. The favourite reason given is the unwinding of the carry trade - precipitated by rising interest rates in Japan. For most investors in the market, the idea of Japan ever being able to raise interest rates seems like a fantasy - and the episodic unwinding of the carry trade is seen as one reason.

One popular carry trade has been long Mexican Peso funded by shorting Yen. Mexico is paying nearly 11% on deposit, while Japan had negative interest rates for until recently. Not only has carry been good, Mexican peso has been very strong against Yen.

A lot of people think they know what a carry trade unwind is. But I was born in it, moulded by it. I made my name by trading both sides of it. The carry trade belongs to me. In fact I even made a trading rule for carry trade unwinds. When an unwind occurs in a carry trade - like in 2008 or 2015, then the fall in higher yielding currency should equal the gain in carry earned in the years before. Or in other words, there is no free lunch. Today in JPYMXN, as seen above, this would imply a move of 50% or more from where we are today, and would be very negative for markets. Do I fear the carry trade now?

For me, I loved the simplicity of the unwinding of the carry trade. I used to explain it as the flow of capital back to Japan. This helped explain one important feature of the unwinding of the carry trade - the collapse in Japanese bond yields. All that capital leaving Mexico, Australia, Brazil, Russia, Korea etc had to go somewhere. Typically you would see 30 year JGB yields collapse in periods of carry trade unwind, like 2008, or 2015 or 2019.

For me, the carry trade unwind was the full economic and financial representation of the “pro-capital” policies. This may seem odd give how much capital tends to be lost in carry trade unwinds, but pro-capital policies place economic adjustment on workers. When an economy becomes uncompetitive, and wages have risen too high, then the easiest possible route out of stagnation is to devalue. This cut real wages, and tends to be positive for asset owners. And in a world with low tariffs and free movement of capital, the lack of wage growth in Japan would make it a natural currency to appreciate, and Mexico with its inflationary tendencies, a natural currency to depreciate. Carry trade unwinds and currency crises are not a bug in the pro-capital system - they are a feature.

But we are now in a pro-labour world politically speaking. For me, the recent appreciation in the Yen is belated political realisation that workers will no longer tolerate falling real wages that a weak Yen implied.

There is also another big change in the world. US trade policy now naturally favours Mexico over China and Japan. In pro-capital world, the most profitable place to invest got all the capital. Now its the safest place to invest. Nearshoring is a real thing, and tariffs favour more investment into Mexico. While a carry trades come and go, industrial policy is forever (or at least a couple of electoral cycles). In a free market world, you should fear the carry trade unwind. In pro-labour world of tariffs and industrial policy - carry trade is nothing but a boogeyman, conjured up to scare investors, and force them back into bonds, before pro-labour polices destroy them again. The JGB market knows what’s up - it has barely moved despite a spike in Nikkei Volatility to over 70.

Pro-capital policies are dead, and so is the destructive ability of carry trade unwinds. Capital or assets will take the adjustment going forward, not real wages.