The portfolio has been build around the idea of a political shift to favour pro-labour policies. There are numerous repercussions in the investment world, and as it is based on politics, is subject to change. The essential idea is that move to pro-labour policies would mean that inflation would be endemic, and that unless central banks raised rates, inflation would take off. The trade I like to represent this trade off most was long gold/short long dated treasuries. The thing bout gold versus treasury trade, was that there was a decent trend in this from 2000 to 2011, before reversing from 2011 to 2020.

2000 to 2011 also roughly coincided with a period of emerging market dominance over US equities. Strong commodity prices and higher interest rates would seem to be a negative for the US, but in 2023, we have seen the US continue to dominate emerging markets.

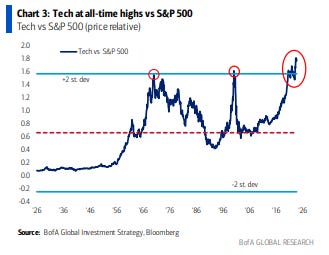

Even worse for active managers, US tech continues to dominate, and has moved far past previous eras of equity dominance.

And of US tech, you have needed to be in the Magnificent Seven.

Where macro fails, I have learnt that politics can offer a way forward.