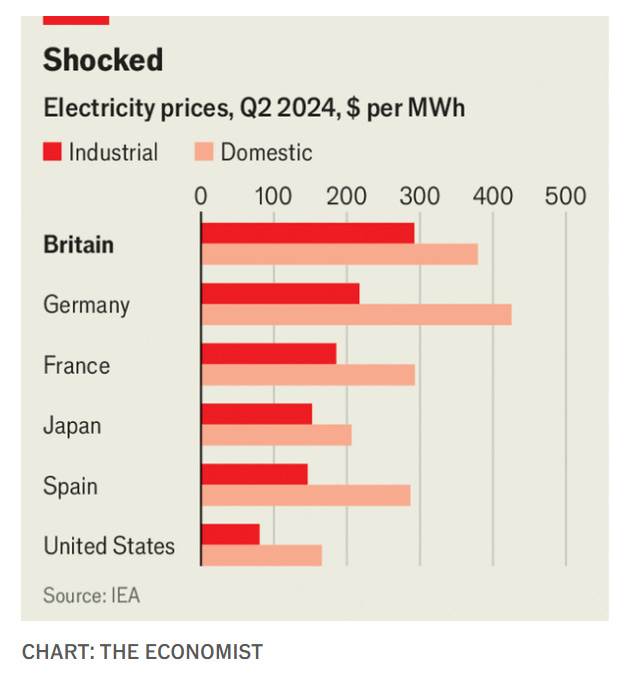

Republican and in particular Trump energy policy can be summed up as “Drill, Baby Drill”. It has become de rigueur in Substack and elsewhere to praise US policy, and the criticise European energy policy. The UK has come in for particular abuse. The main nature of this abuse is that high energy costs in the Europe and a pursuit of net zero has led to business stagnation. This Economist article is pretty much standard. The key graphic is below.

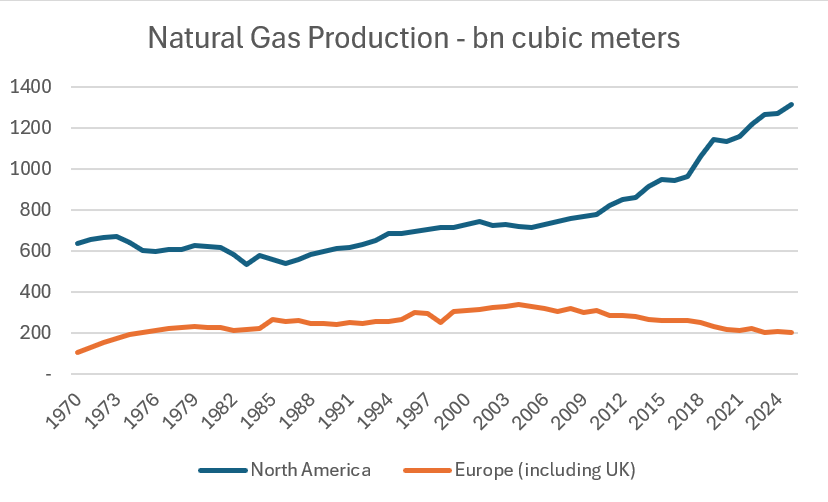

The political view on this is that the UK has been “too woke” and heavy taxation on oil and gas production, as well as trying to upgrade an electricity grid has made UK and Europe uncompetitive. Data from one my favourite publications, the Energy Institute Statistical Review of World Energy 75th edition provides compelling evidence. North American natural gas production has surged, while European gas production has collapsed.

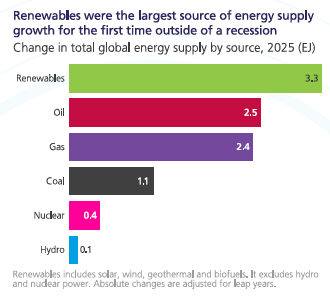

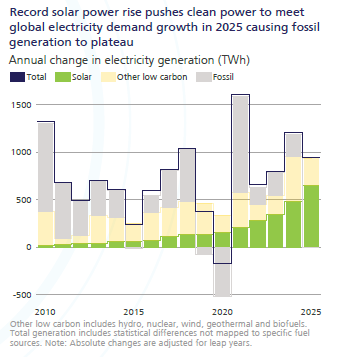

But as I read through the rest of the publication, I was struck by how much it made the US policy of increasing fossil fuel production looks like a short term win, but long term loss. This review starts strong by highlighting how renewable energy became the biggest source of new energy in 2025 - the first time outside of a recession. Now you may have, like President Trump, a natural born hatred of renewable energy. But last year it proved it can add capacity at a fast enough rate to not slow GDP growth.

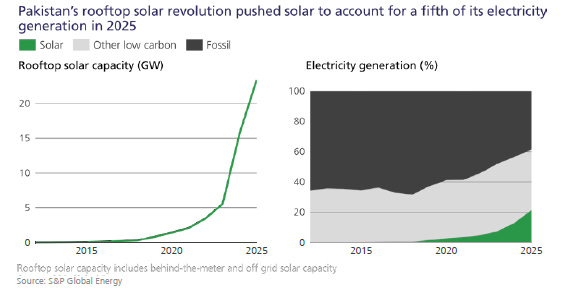

And I find it stunning that Pakistan gets 20% of its energy from solar panels. This does hold out the possibility of decarbonised future. If developing markets can adopt renewable energy early, then the outlook for fossil fuels looks negative to me. For places like Pakistan, building out a decentralised system seems like a good option.

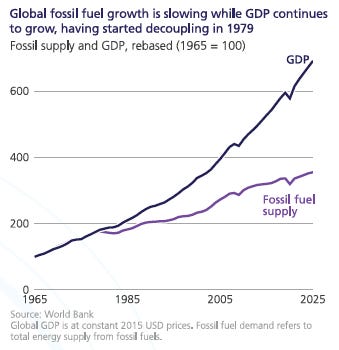

We can see that the relationship between GDP and fossil fuel supply is already breaking. This is probably the most negative chart you could possible produce on fossil fuel in my view.

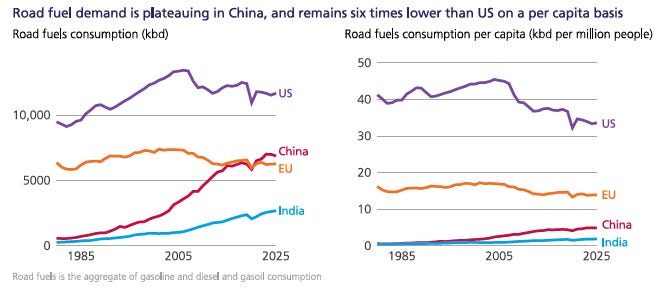

China, where EV usage is higher, is already slowing oil consumption at a much lower per capita level. This is almost a reverse of the emerging market investing model. When I started, it was assumed emerging markets would converge on western consumption levels. Not it looks like Western consumption levels will converge to Chinese levels. Potentially you could see western demand for road fuel drop by half.

The world is moving towards an electrified future, with renewables meeting much of the demand growth.

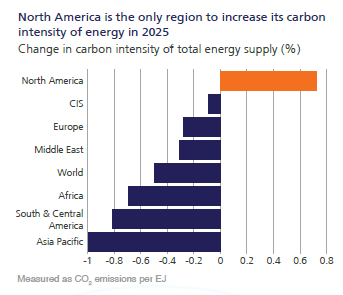

It follows it up with this very arresting graph of US exceptionalism. When I look at this, I start to see a potential problem for the US. A decarbonised world does seem inevitable to me - despite the protestations of corporates and older voters. Eventually the Greta Thumbergs of the world will be politicians and not activists. North America is alone in making its energy supply more carbon intensive.

Here is where the politics gets interesting. European carbon prices have remained at a high level for a few years already. Which comes back to the original argument that European electricity costs too much. But does it really cost too much, when it incentivising the growth of renewable energy and true energy independence? Does it make sense to switch reliance on Russian energy exports to US energy exports?

Which is a much higher level than markets elsewhere. California Carbon Allowance is one third of European levels.

But this has had the effect of leading to a much more thoroughly decarbonised electricity generation system than either the US or China. Europe is much closer to fossil fuel independence than either China or the US.

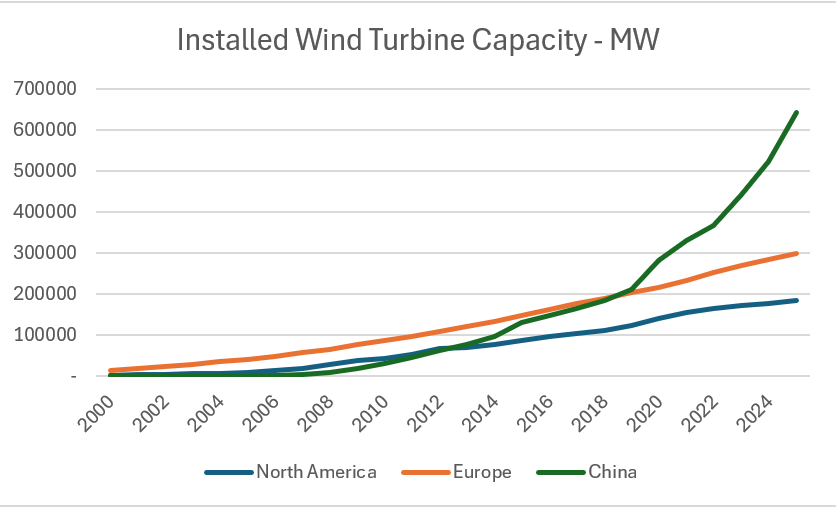

In this pro-labour world we live in, with tariffs and industrial policy. It would be very easy to see Europe seeing US renewable energy policy as “carbon dumping”, or race to the bottom deregulation. Why not tariff US exports to price the externality of the carbon heavy energy production? What I am saying is that the data already shows that fossil fuel consumption has already broken away from GDP growth, something that markets have already shown when Russia turned off the energy supply in 2022, and again this year with the closing of the Straits of Hormuz. In fact, sometime the best way to think about US foreign policy changes, is going from a free trade era to ensure maximum oil supply, to a competitive era, where it is looking to reduce competition for its exports. But long term, do you want to be investing in an industry that looks to be heading for decline? North America already lags badly behind China and Europe in Wind capacity.

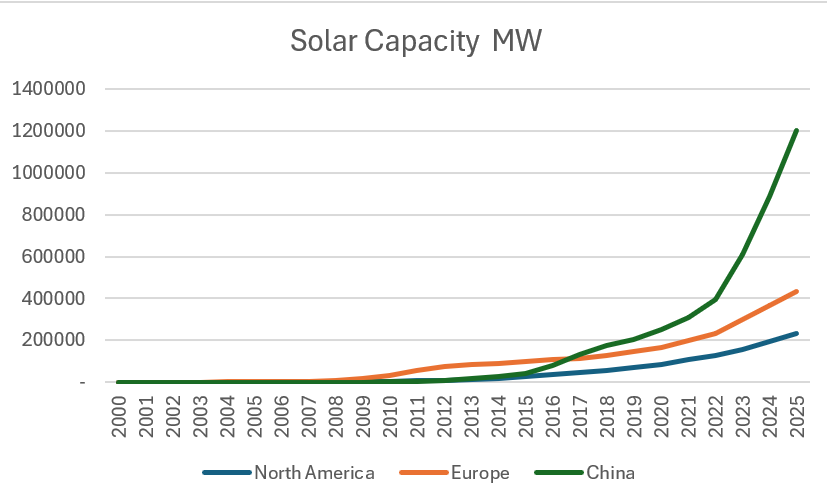

Likewise in solar capacity.

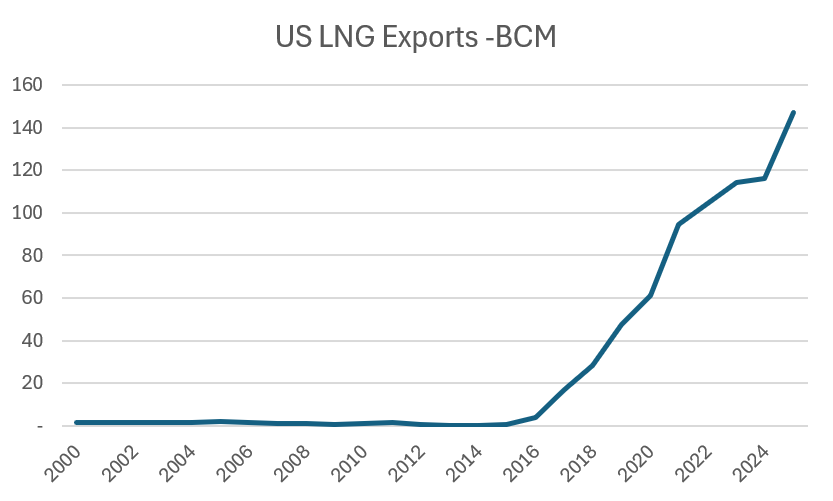

For the first time, I wonder if we could see US LNG exports actually decline at some point? While the Straits of Hormuz are closed, this should be fine. But in my mind, the pieces for globally falling fossil fuel consumption are coming together.

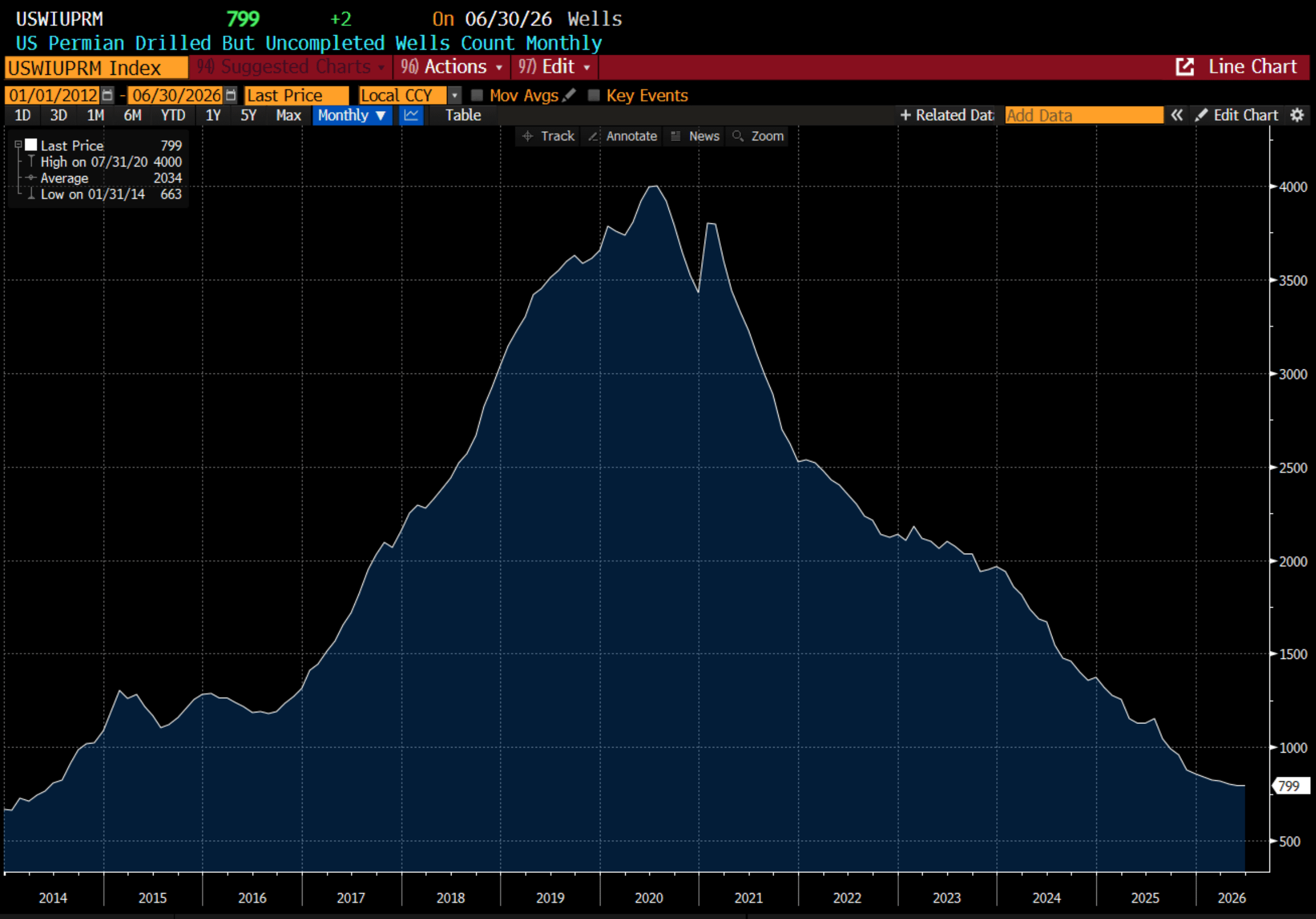

I do wonder if US shale producers see this same world as me. Permian drillers have been running down their stock of wells now for a few years. Even with the supply disruptions in Russia and the Middle East.

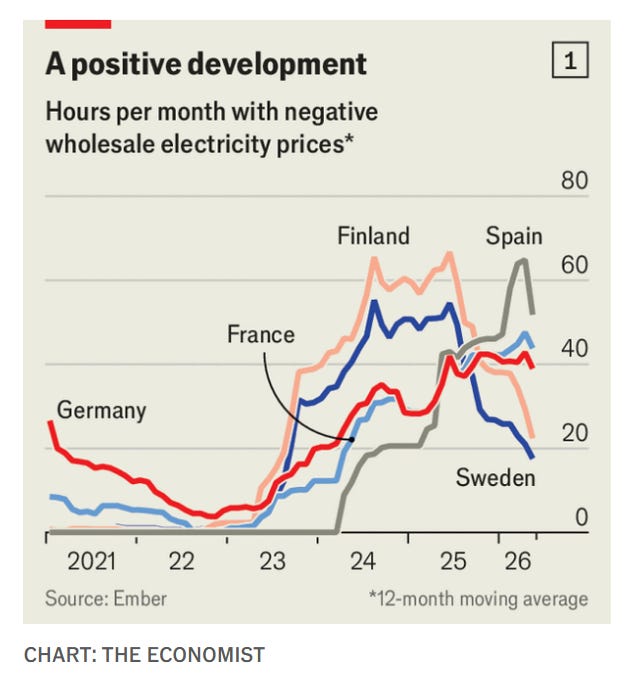

If there is one thing I have learnt in my life, is not to bet against technological change. And it is hard to not see technology making fossil fuel yesterdays energy. The interesting part for me, is that we are already beginning to see signs of the benefits of European investment into renewables. Negative pricing is becoming more common.

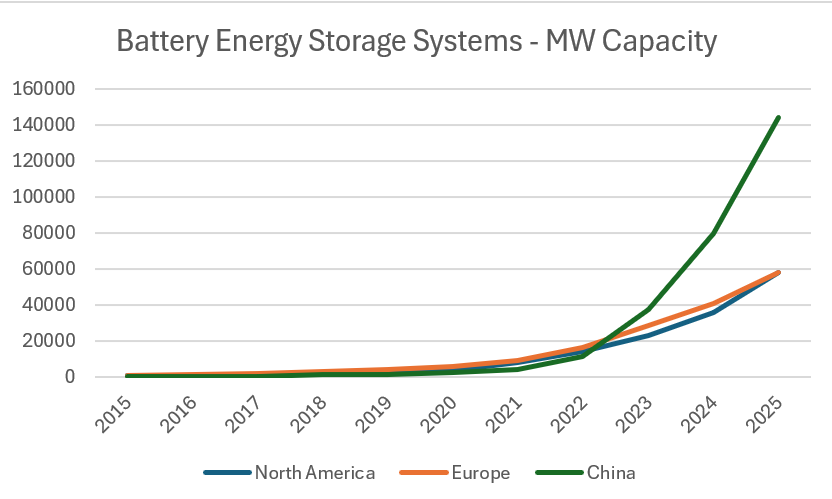

And this negative pricing in driving a build out in battery storage.

Putting it all together, it looks more and more like fossil fuels are a dead industry.