I always think of this as one of my all time great notes, for two reasons. First, almost no one had looked at this before I did, and second, after I looked at it, I had research providers trying to sell me this as their own research.

In some ways, this is a timely note - as once again ETFs (this time leveraged single stock ETFs) are causing market havoc.

Japanese US REIT funds and the Buy Case for Yen (2015)

The last few years in Japan have seen the emergence of and selling of some innovative high yield funds. These asset management products are designed to pay out very high yields, while sadly almost guaranteeing the destruction of capital. There are numerous examples of this but this note shall deal with only US REIT Funds sold in Japan.

According to Goldman Sachs, the largest 20 Japanese US REIT funds have 50bn USD under management. The single largest is the Shinko US REIT fund (Bloomberg Ticker: 06311049 JP), which has an AUM of around 14bn USD. For comparison the Vanguard US REIT Index fund has 26bn USD of assets, total US REIT market capitalization is 720bn USD.

Japanese US REIT funds tend to offer a dividend yield in the high teens. The Shinko fund has a yield of 17% currently. For reference the US based Vanguard REIT Fund has a yield of 3.4%. The extra yield of 13.6% does not come from leverage. In fact the assets owned by the funds are very similar. Rather Japanese funds will sell down assets to ensure that a higher yield is paid out.

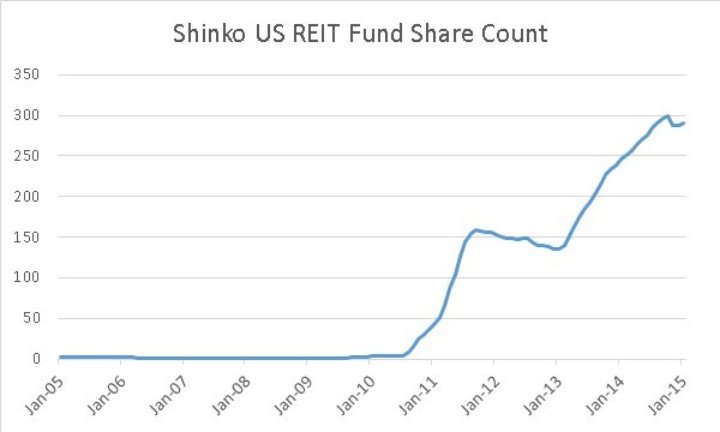

From 2005 to 2010, the Shinko fund and Vanguard fund had very similar performance, after 2010 a huge divergence opened up. In my view, Shinko noticed that assets under management at their fund grew aggressively when funds offered a high dividend yield. Talks with participants in Japanese financial markets indicate Japanese investors prefer funds that offer at least a 1% monthly dividend yield.

As can be seen from above, Shinko AUM exploded higher once it began to offer a yield in excess of 12%, and it continues to rise. The other major funds that I have looked at all offer similar yields and are presumably managed in a similar way.

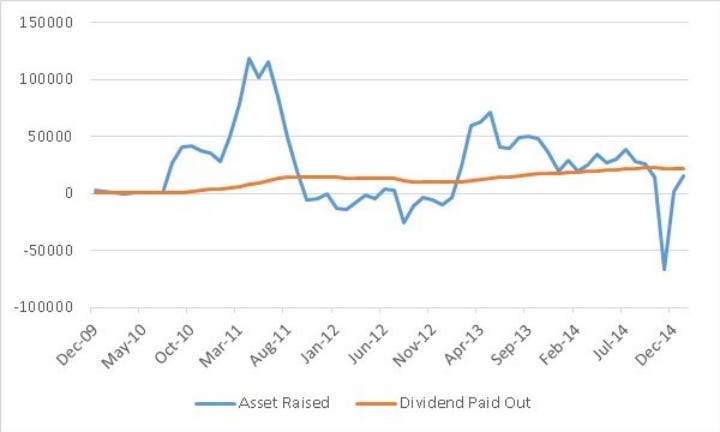

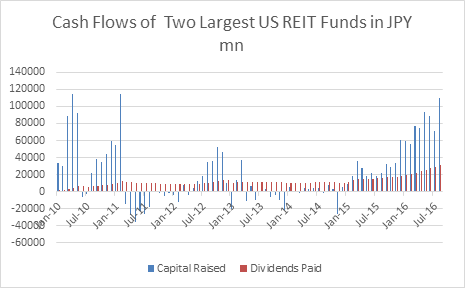

With such high dividends, assets under management can fall as the fund needs to sell assets to pay dividends. To get an idea of when this can happen we can use the change in the share count of the fund multiplied by the fund price and then subtract the dividend payout to calculate net cashflow movements in the fund. We can see that there have been two times when assets raised have fallen below the cash needed to pay out.

This has a very clear effect on the shares outstanding for the Shinko fund, which fell in 2012, and again in recent months.

I suspect this new fund structure will have a big effect on the Yen. Typically, the flow of investment funds relative to currency movements is unknown. The reason for this is that sometimes investors will see the currency depreciation as a chance to buy an asset cheaper. Certainly US listed Japan equity funds tend to see rising share count (i.e. raising assets) when the yen is weakening. In other cases, weak currencies tend to correlate to weak returns and investors selling assets. The latter is what we have seen more recently with emerging markets funds

What I find most intriguing is that at constant values, ie US REITS remain constant, and the Yen exchange rate does not change, and Shinko does not raise any more assets, then this fund will be forced to sell 14% of its holdings in the US to repatriate to Japan to pay dividends each year. What is true for Shinko would be true for the industry as a whole.

The implications of this are intriguing for me. Firstly, assets in these funds are very unstable, as the high yields destroy assets under management very quickly. Secondly, if there was a shock that caused yen to appreciate or US REITS to fall in value, funds like Shinko would be forced to liquidate their assets very quickly to meet redemptions and dividend payments. Their liquidation could cause yen to appreciate further and possibly REIT to fall in value locking them into a vicious cycle. Even more disturbing, that this is only one of seemingly many assets classes that have this feature.

For investors nervous about the state of global markets, a long yen position seems to offer a good hedge in my view.

Japanese US REIT Fund – an Update 2016

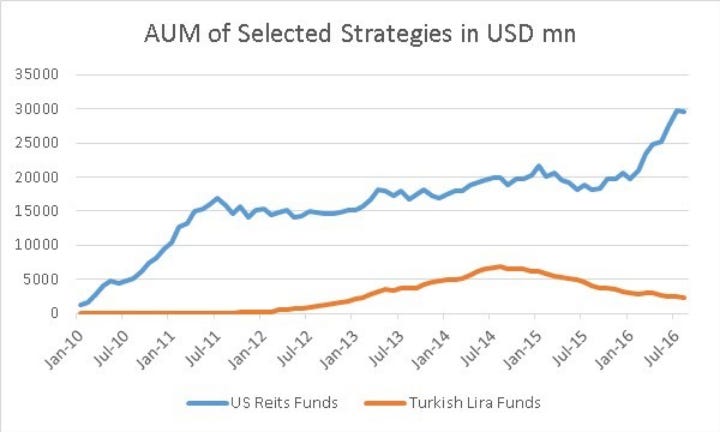

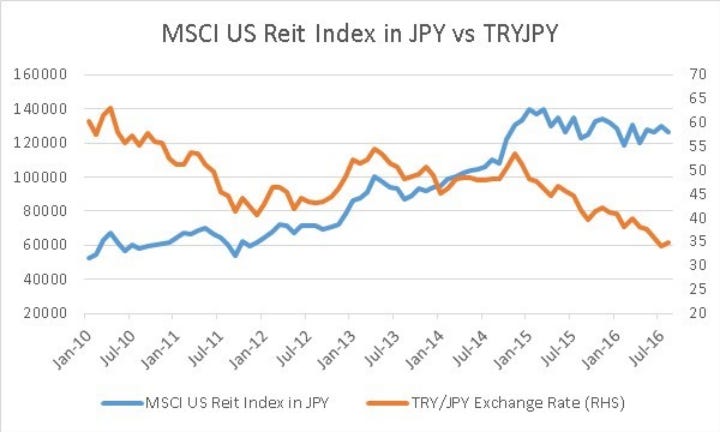

In 2015, we released two market views about Japanese investors being short Yen via fund products. One was long Turkish lira (TRY) and short Yen (JPY), while the other was long US Reits (Real Estate Investment Trusts) unhedged. Both of these assets classes are relatively concentrated, the two largest TRY funds account for 80% of assets, while the two largest US Reit funds make up 50% of assets. This year we have seen Yen rally significantly. While the size of the Turkish lira funds (Amundi European High Yield – TRY Course and Nikko Pimco High Income Soverign Fund – TRY Course) have shrunk dramatically, the US Reit funds (Shinko US Reit and Fidelity US Reit Fund) have increased.

The contrasting fortunes of Turkish lira funds and US Reit funds in Japan are undoubtedly connected to the divergent performance of these assets. The Turkish lira has been very poor, while US Reits have performed well.

While the US Reit funds and the Turkish lira funds are very different assets, they both offer Japanese investors very high dividend yields as the main selling point for Japanese yield hungry retail investors. The largest Turkish lira fund, the Amundi Europe High Yield fund Turkish Lira Course, still offers a 25% indicated yield. The largest US REIT fund in Japan, Shinko, also offers an indicated yield of 25%. This level of dividend yield is typical of the funds in this space.

US Reits do not offer 25% dividend yields, and the Japanese US Reit funds are not leveraged. Instead, they commit to maintaining these dividend yields from capital. Fortunately, for these funds they have been able to raise enough funds and realise enough capital appreciation to grow their funds’ assets significantly. The problem is that with increasing share count, and large yields the two largest funds are paying out 64bn JPY (640m USD) a month. Since 2015, a period of significant capital raising, they have on average raised 80bn JPY a month. If Japanese investors just cease adding capital to these funds as they did in 2012 and 2014, it would precipitate significant selling of US Reit holdings to pay dividends.

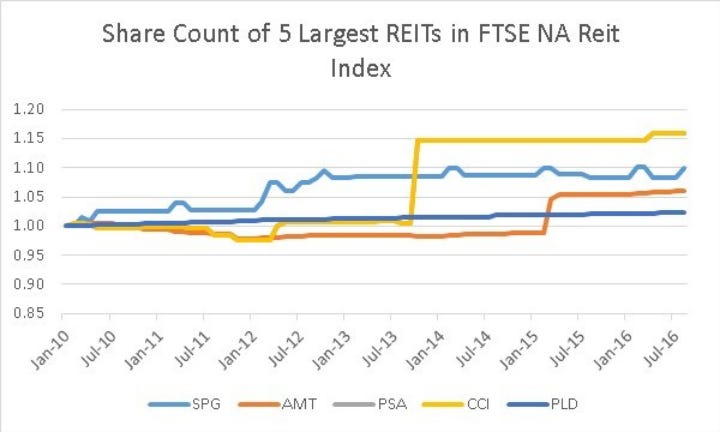

It is also interesting that US Reits, in contrast to the trend for most US corporates, have generally been issuers of shares, some quite dramatically. In general terms, Japan based US Reit Fund use the FTSE North America Reit Index as a benchmark. According to the index provider, the top five stocks in this index is Simon Property Group, American Tower Corp, Public Storage, Crown Castle Intl and Prologis.

Reits have various tax advantages, as long as they pay out the majority of their income as dividends. This means that to grow assets, they need to issue shares to buy assets. The Reits above are typical in that share count has a tendency to rise over time. It seems to me that for the Reits to grow, they need to be able to find buyers of new shares at ever higher prices, while Japanese based US Reit funds need to find new investors to not become sellers of Reits to meet dividend commitments. This strikes me as particularly unstable.