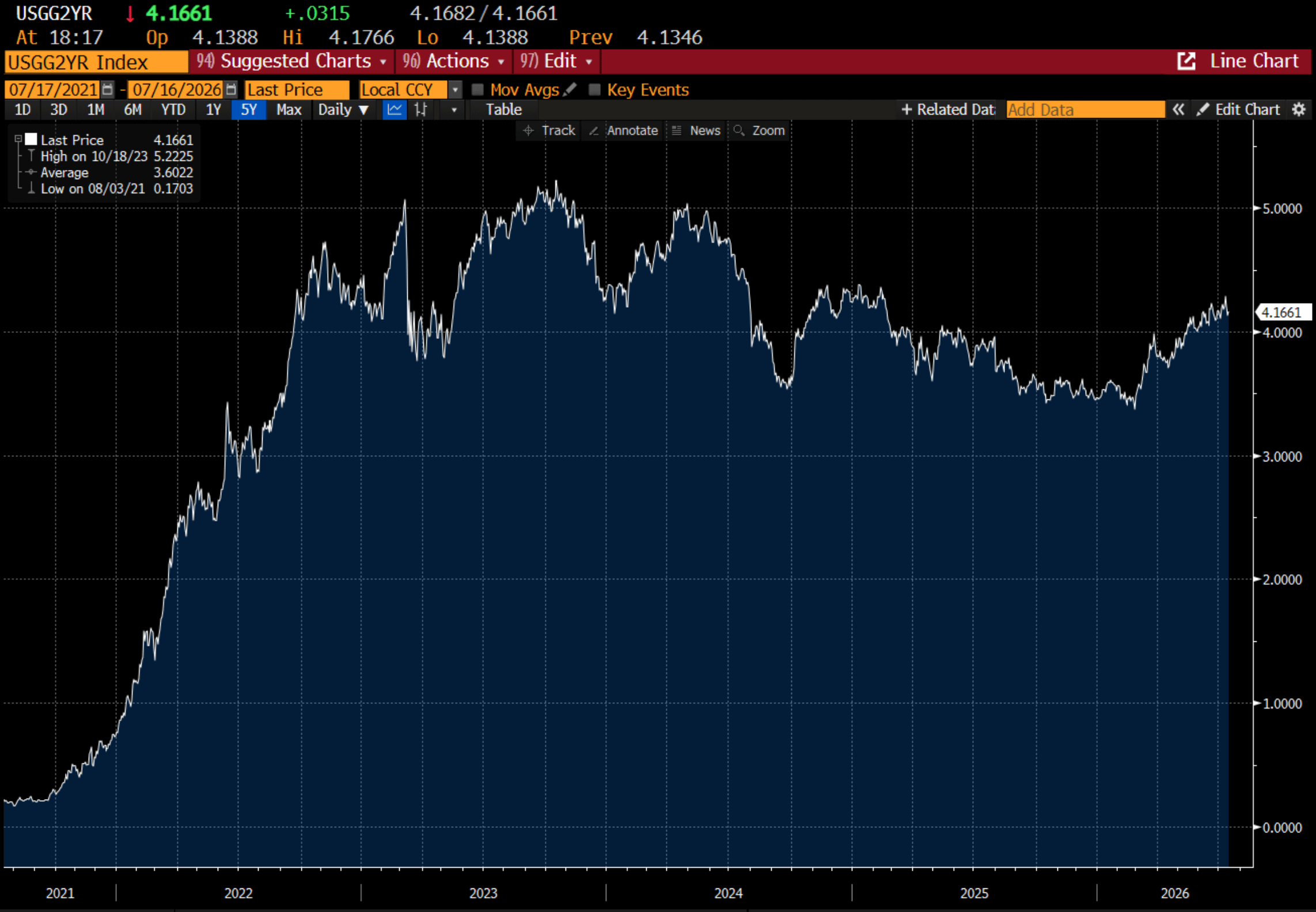

I have been thinking about markets in a political way for a few years. I have this theory that we were moving to a “pro-labour” era, which would be good for wages, but higher interest rates would be bad for asset markets. In some ways we have seen this, with market doing very well while 2 year yields were falling, and now we are getting all sorts of market weirdness now that 2 year yields are rising.

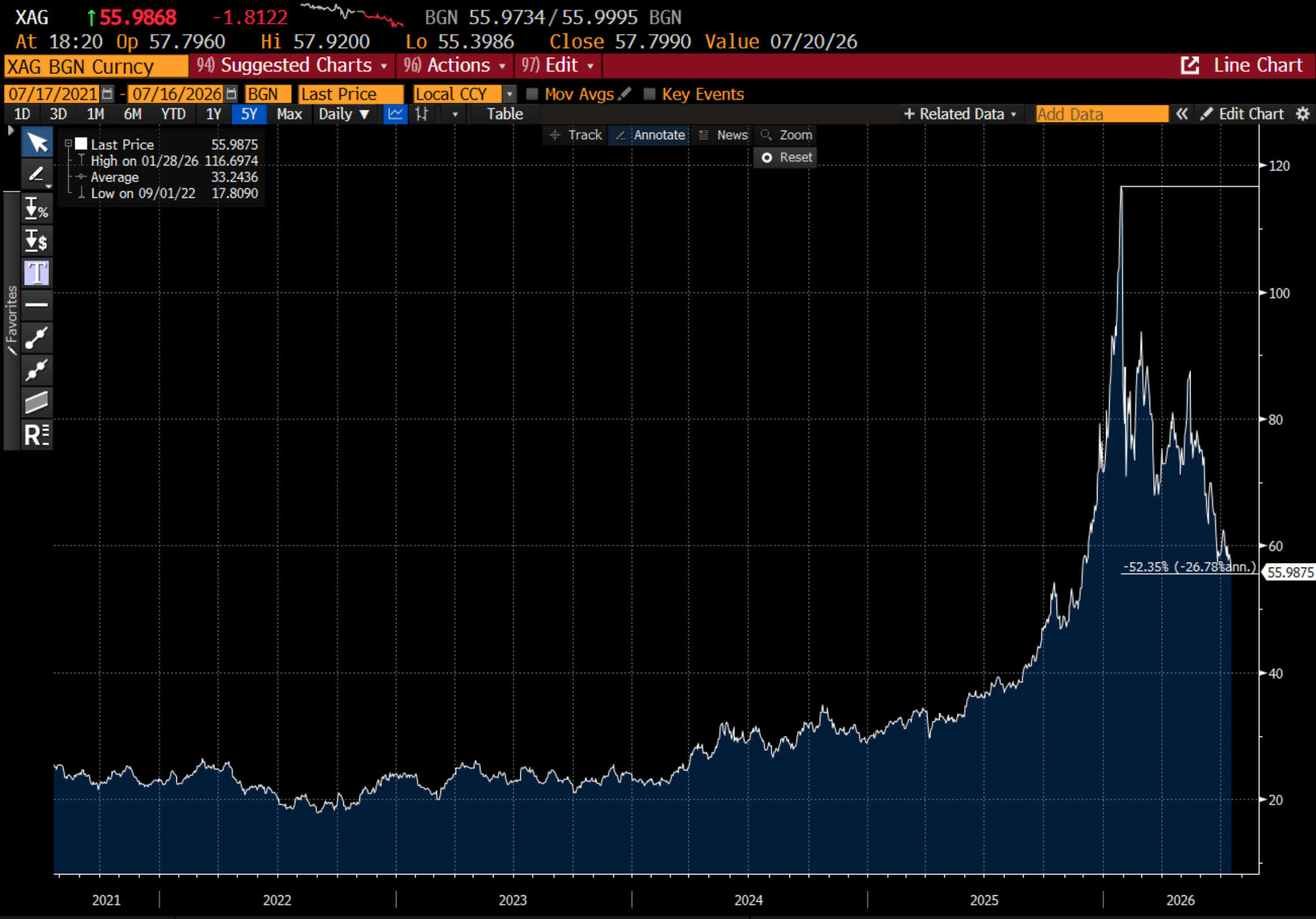

What has been most interesting is that rising yields HAVE been hugely negative for SPECULATIVE assets. Silver, which does have central bank supporting it, has gotten smacked this year, down 55% from its peak.

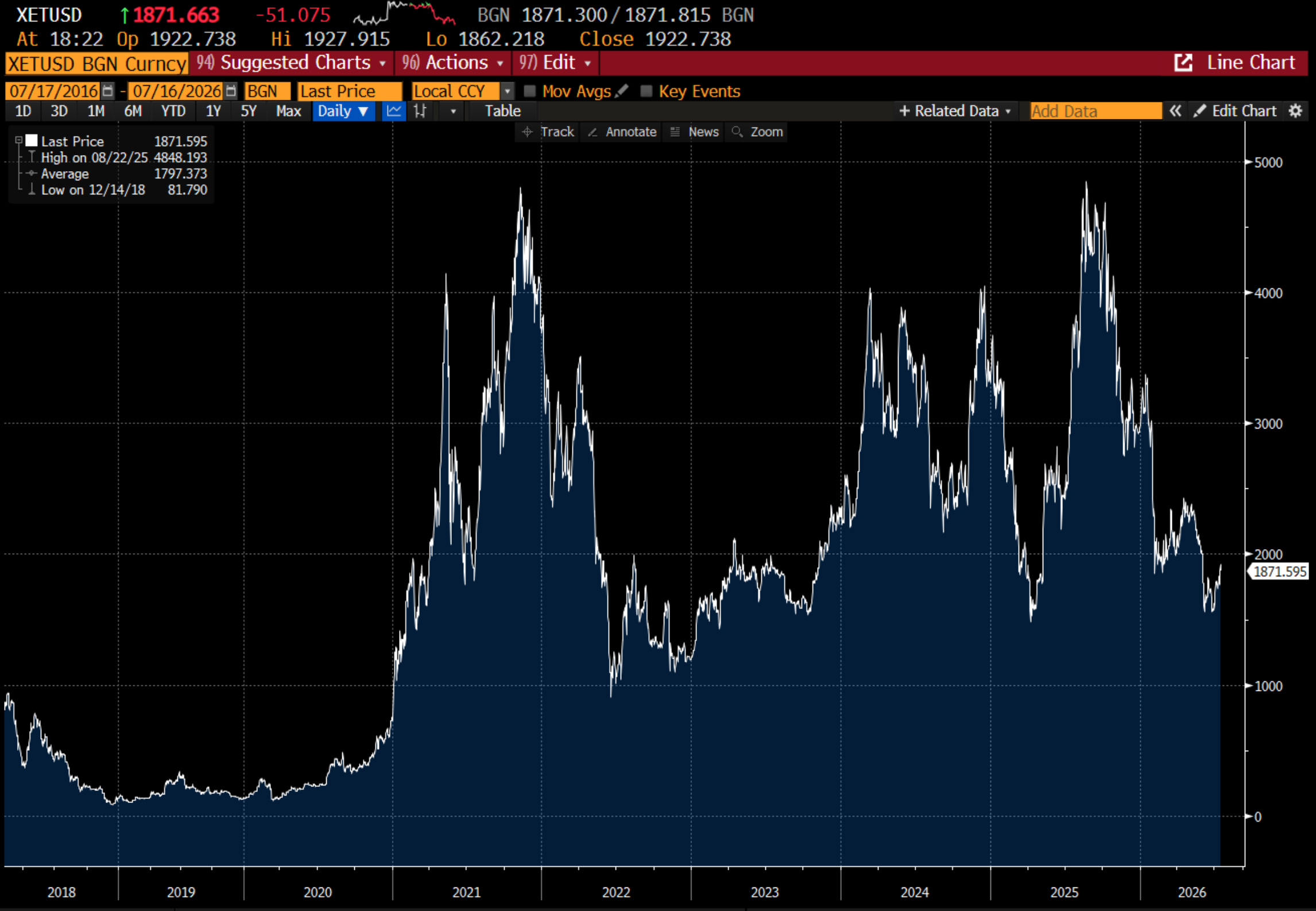

Crypto has been given the same treatment - with Ethereum at 2020 prices.

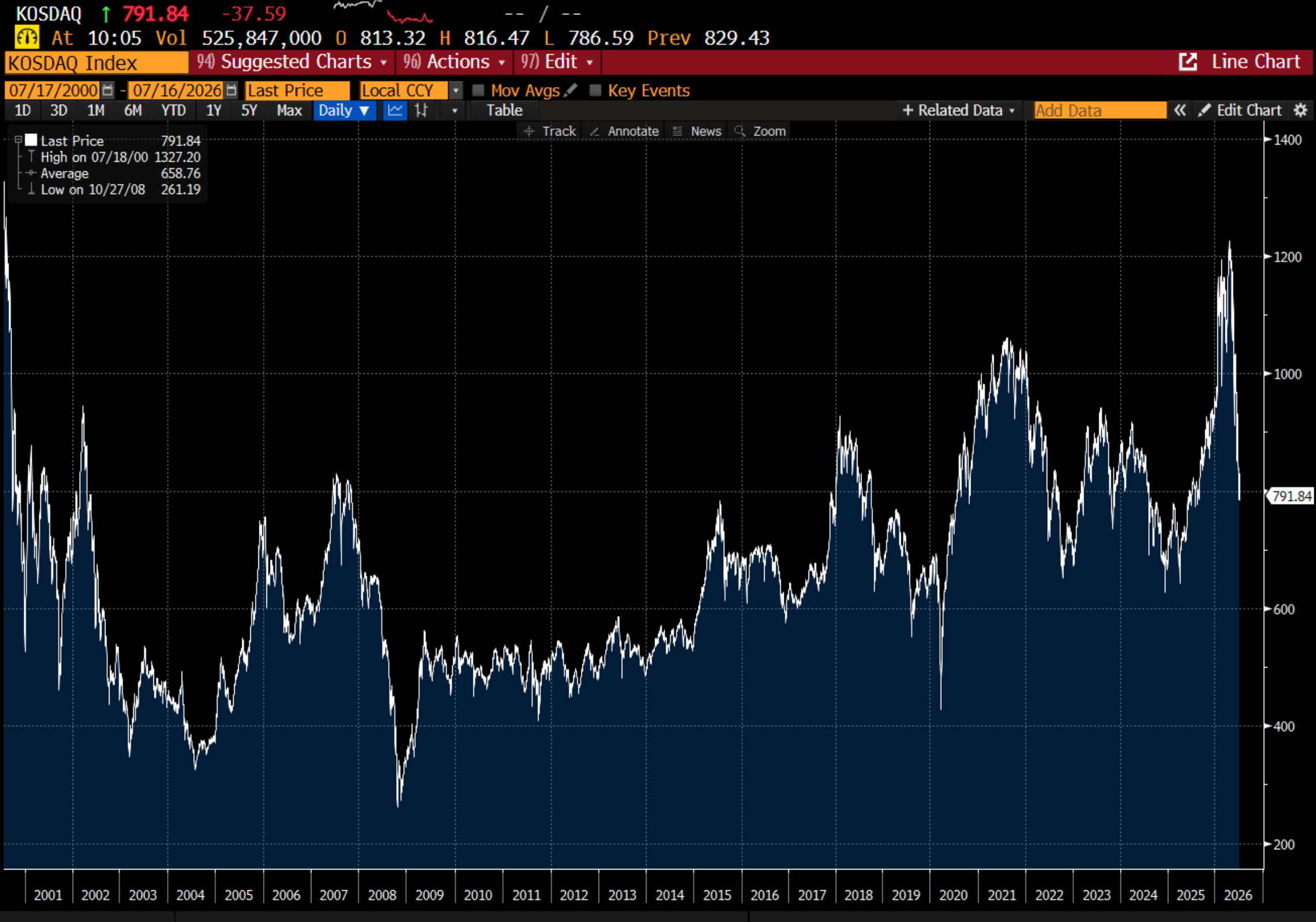

I have mentioned private credit and private equity have also been at the mercy of this speculative asset smackdown. But the trillion dollar question is whether AI is a speculative asset or not? Lets take a closer look at Korea. The Kospi, which has broken out of a long term ranges, has become a memory/AI trade.

But weirdly, the Kosdaq, another speculative Korean index has been very poor this year. What I am trying to say here is that generally speaking Korean stocks have been difficult, but the memory/AI plays have been good.

Now here is the rub. I think many people think AI is entirely speculative. I think this is not correct. But I do think speculative structures have been erected around AI trades. Why is AI not speculative? Well memory prices have moved, and remain at highs.

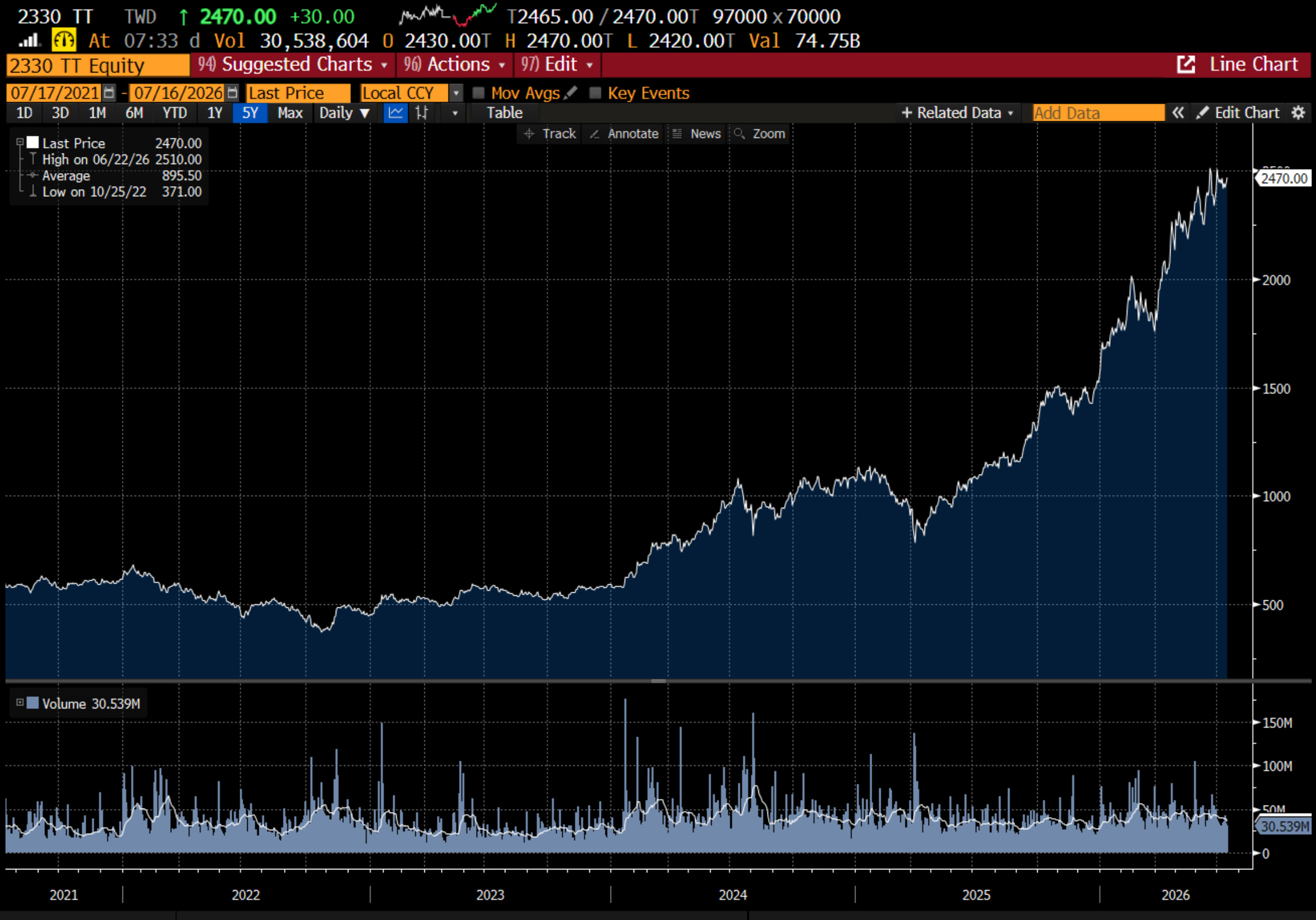

If the AI boom is done, then why does TSMC remain at all time highs?

If you are bearish, then you could point at Korean memory stocks or Micron, and say, look these stocks are down 30% - its the beginning of the end.

But the thing is, the memory stocks sit at the intersection of AI and speculative trading. When I look at MUU - the 2x levered Micron ETF - and see shares outstanding up 8 times from a year ago (market cap USD 4bn), I see speculation has run wild.

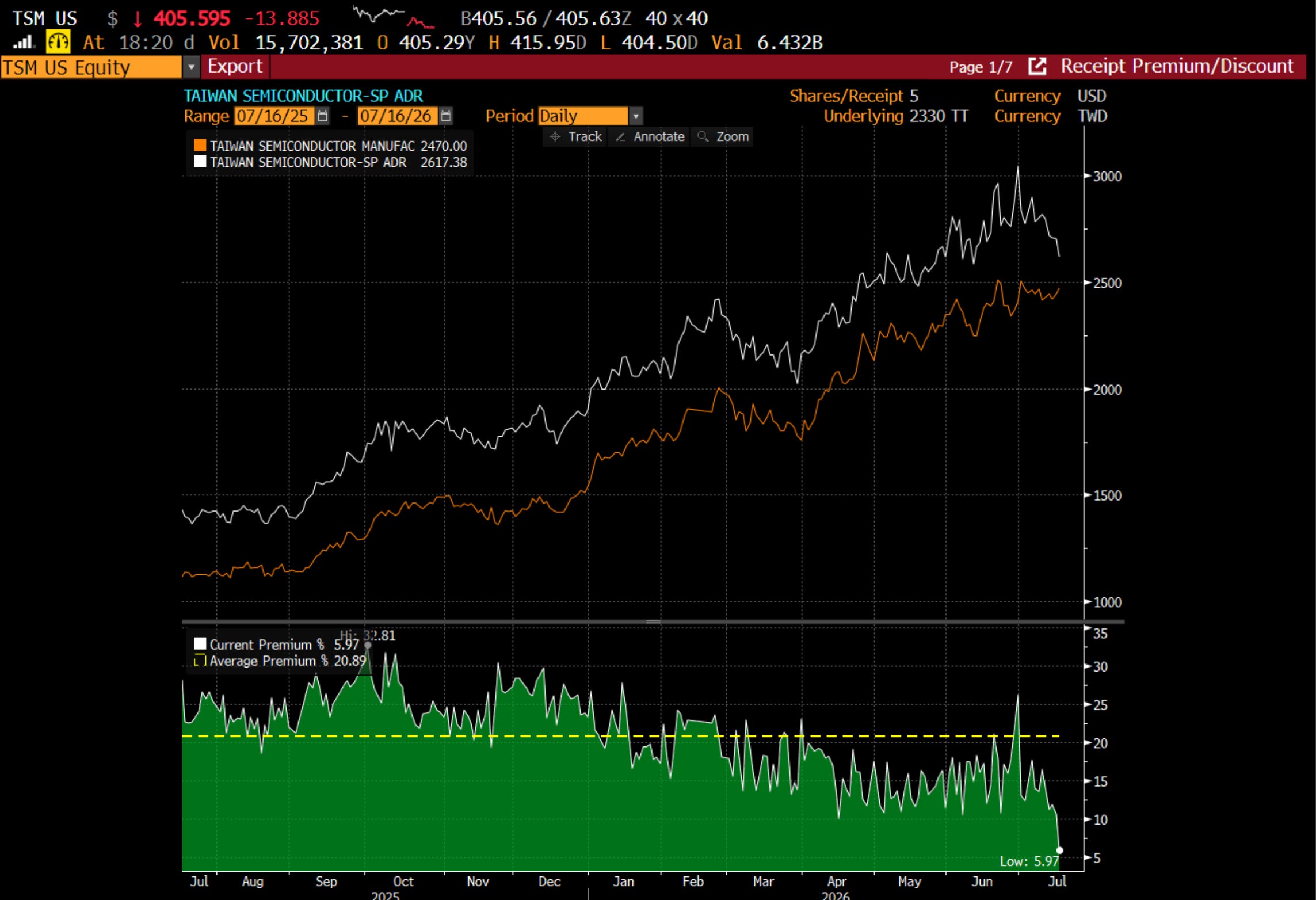

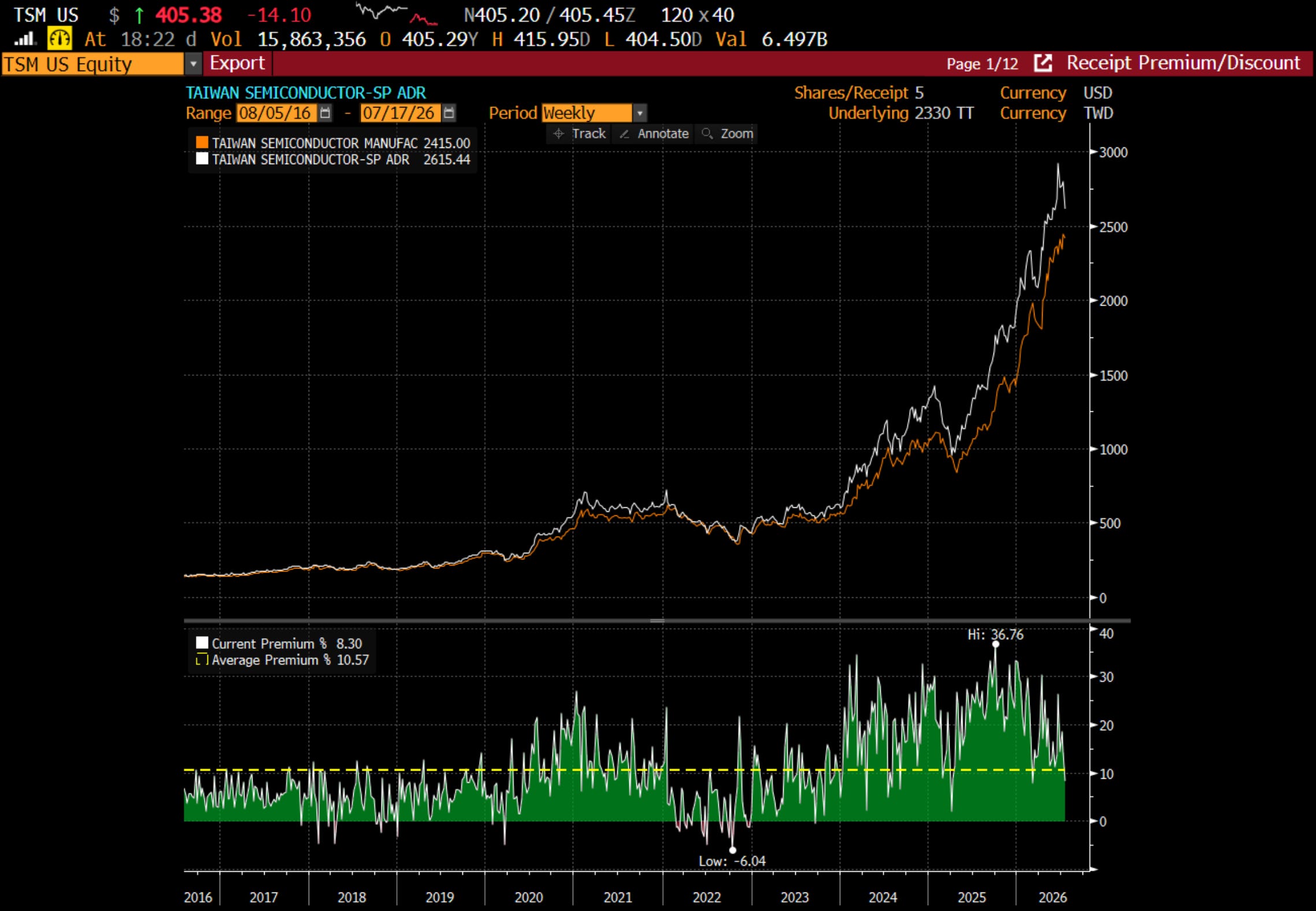

What I am saying is that it is right to be bearish on speculation, but I am not sure it is right to be bearish on AI. I am also going to follow that up with a view that perhaps we are near the end of the “speculation” bear trade. As pointed out, memory prices and TSMC local shares remain strong. But demand for TSMC ADRS (the US listed stock) has historically been so strong, it has traded at a premium to locals for many years. As of today, the premium has fallen to 6%, down form 25% not so long ago.

Typically the collapse in premium happens at lows. That is speculative unwind may have run its course.

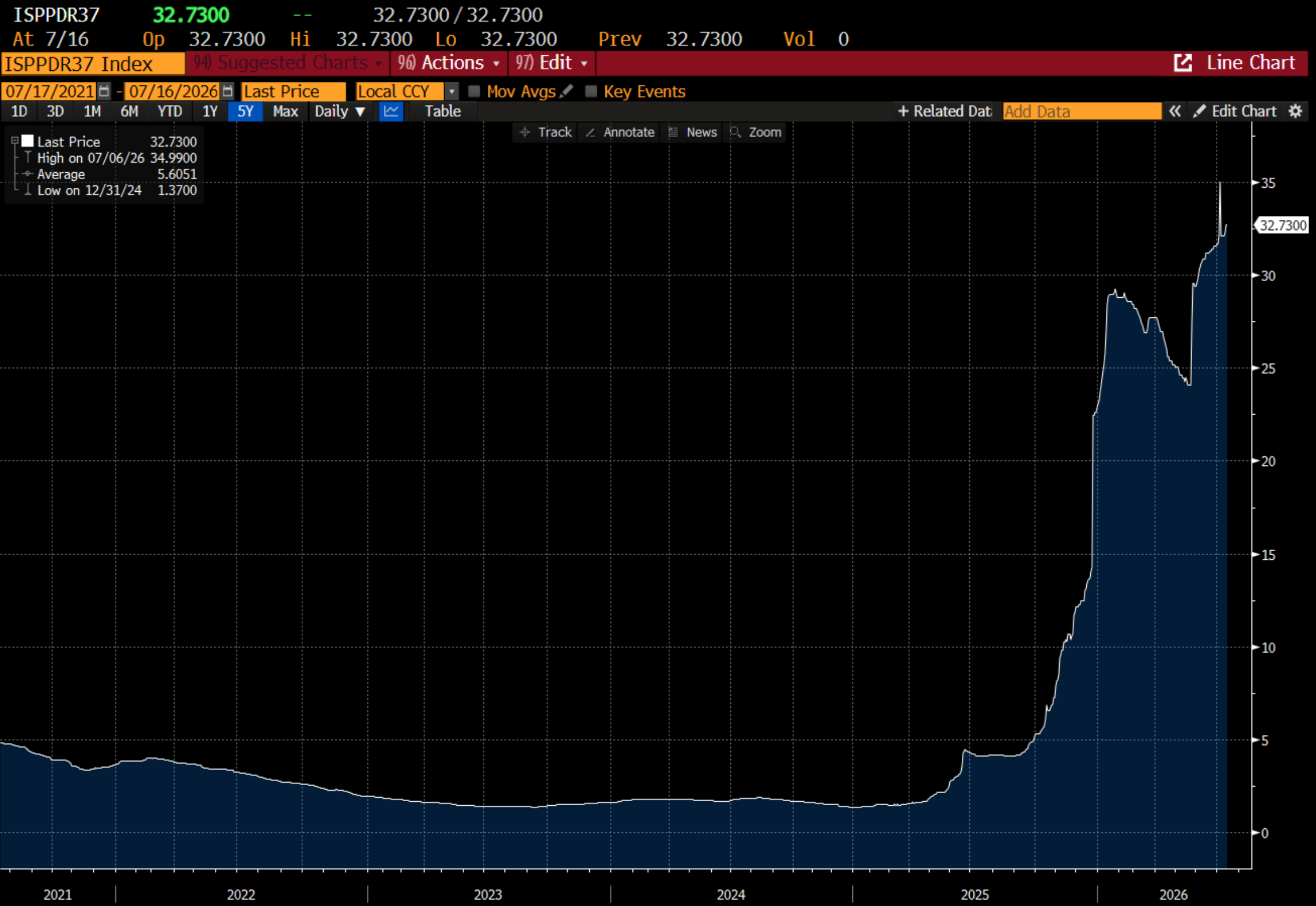

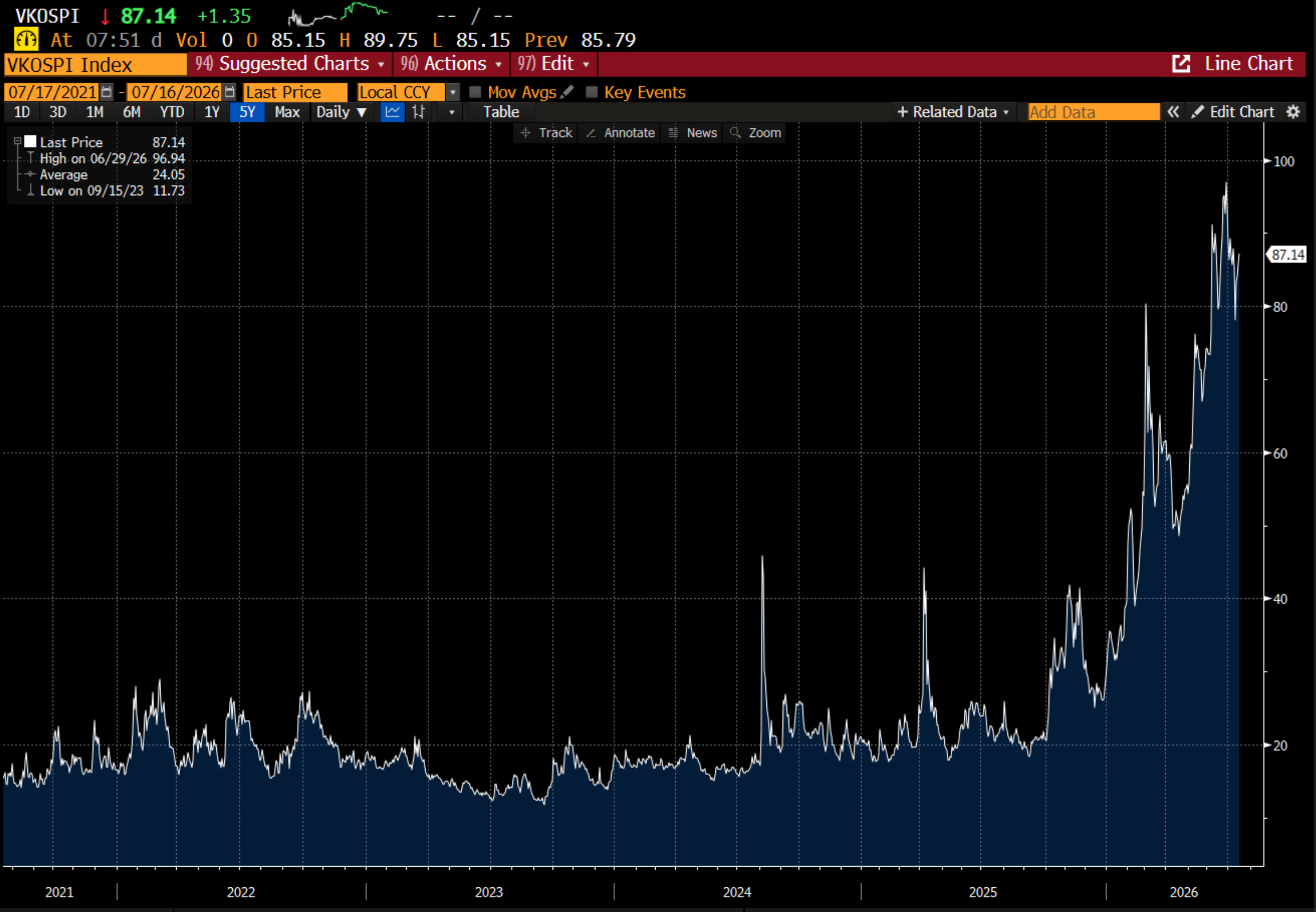

VKOSPI, which is VIX for the Kospi200, is running at about 80. This is a level I normally associate with a washout in markets, and potential buying opportunity.

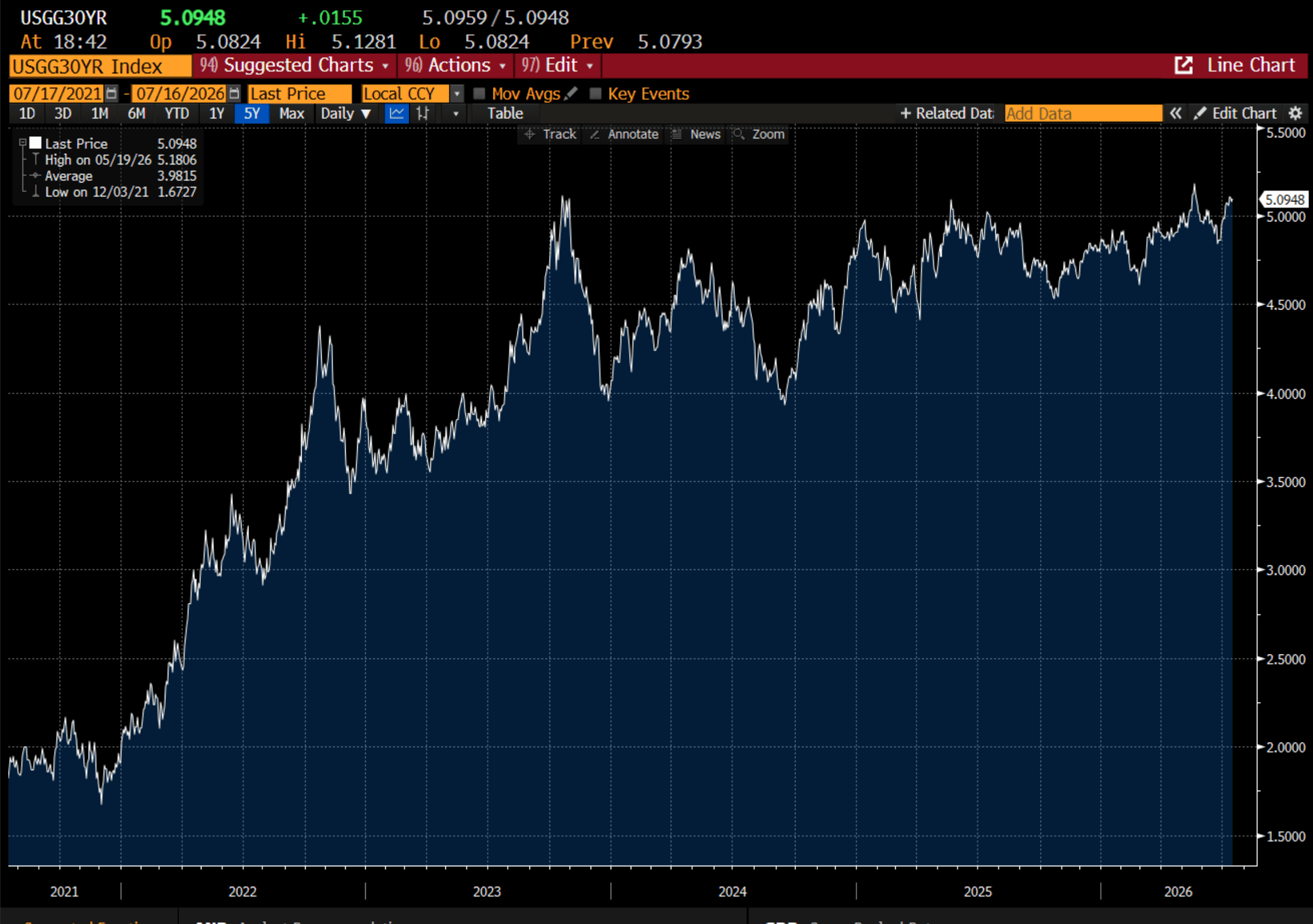

So what am I try to say? The pro-labour trade should be good for growth, but higher yields should be and has been bad for speculative assets. From where I sit, AI trade does not look speculative, but the market has built up a range of “speculative” assets around AI. For my money, I think the chat about AI crash or not is missing the bigger picture. If short term rates are bad for speculative assets, their remains one speculative asset that really moves markets - the US 30 year treasury. Very quietly, yields have passed through 5% again.

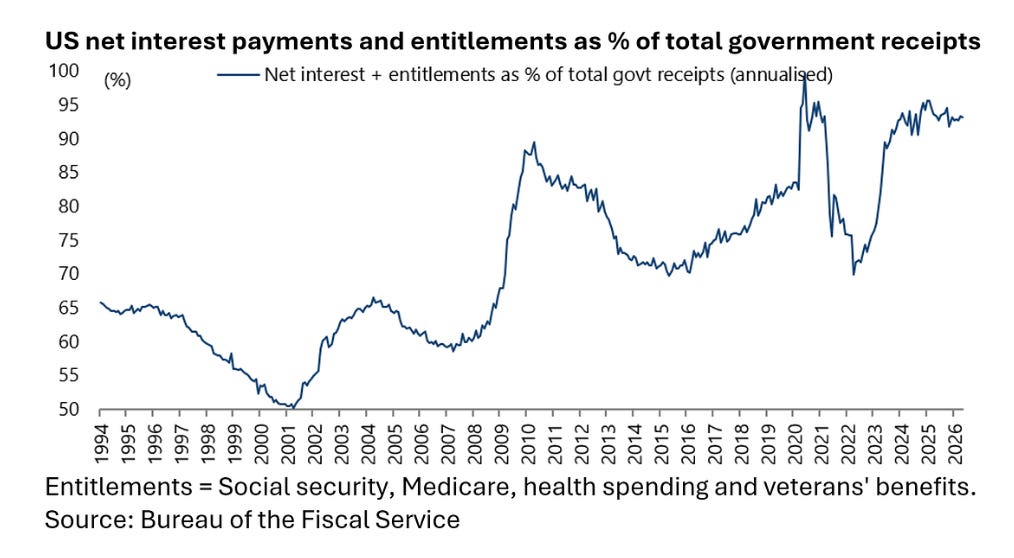

As my substack colleagues over at Grizzle Research and Quant point out, the US government really does not have any money anymore. Everything that comes in the door goes out in interest payments and entitlements.

I do think it is right to be bearish speculative assets here - but I am not sure AI is speculative. On the contrary, the “safe asset” that underpins all finance looks to be more problematic to me.