Professional fund managers will often worry about whether they are on the slope of hope, or are climbing the wall of worry. The slope of hope refers to the awful position of being on the wrong side of the market, and holding on in the “hope” that your position will come good. The wall of worry is that you are worried markets might fall in value, but never do. Back in the early 2000s, you could only really guess by reading stock broker morning emails, and perhaps looking at other funds positioning.

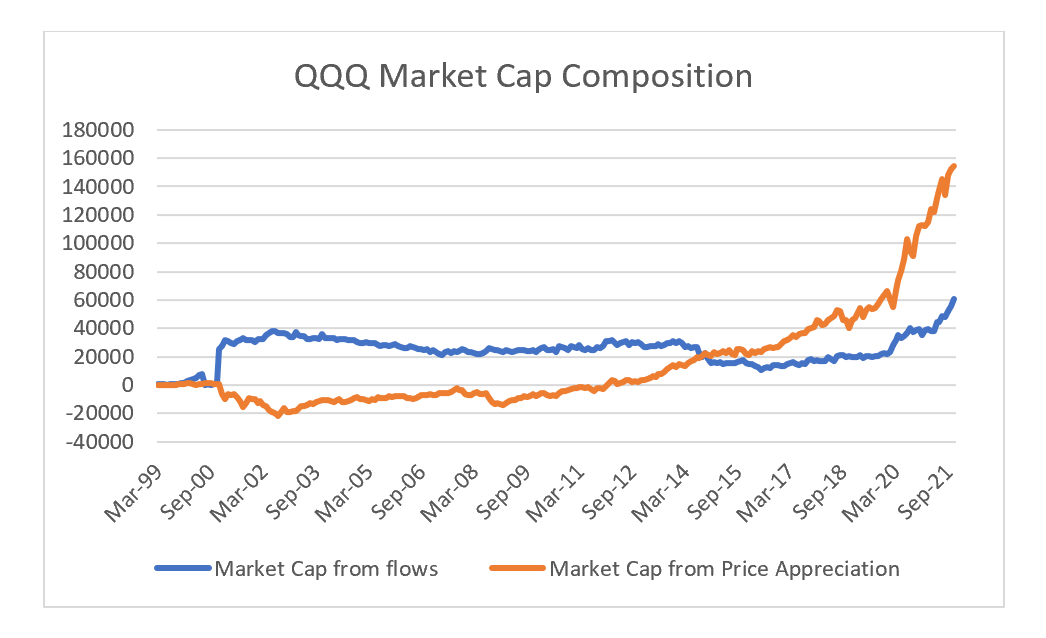

However the advent of ETFs have made the slope of hope/wall of worry discussion much easier. QQQ - the Invesco Nasdaq 100 ETF - was one of the first popular ETFs, and remains one of the biggest. As can be seen below, in 2001 shares outstanding and performance went in very different directions. A classic sign of riding down the slope of hope. By contrast, even as the Nasdaq has broken to new all time highs in 2015, shares outstanding has only risen slowly, a classic climbing the wall of worry, until recently anyway.

What is very surprising about the QQQ is that for the first 10 years of its life, the average investor had lost money. We can use two data points, the price of the the ETF and the shares outstanding to breakdown the market cap of the ETF into flow and price appreciation. For dot com era for the next 10 years, all of the market cap for QQQ came from flows, as the average investor had lost money on QQQ. For me this, is classic, slope of hope investing. However from 2014 through to 2018, the QQQ was climbing a wall of worry, as new highs in the QQQ was not greeted with rising inflows. However 2021 has seen the first new high in QQQ with a new high in shares outstanding since 1999.

One observation I take from this is that ETFs seem to have a wonderful countercyclical nature, that they take in flows even when in a bear market. This is probably shown in the fabulous performance of the world’s largest ETF manager - Blackrock.

But what can ETFs tell us about retail sentiment particularly in tech? If we get away from QQQ to other high profile ETFs, we see much clearer signs of a trend change. The ARKK funds was a leading fund for many years. However in early 2021, the fund saw underperformance early in the year, but was still greeted with further inflows, that have only slowly begun to turn to outflows. That is investors moved to a slope of hope, which has been borne out in 2022 so far.

Much like the QQQ in 2001, the average ARKK investors is now underwater on their investment.

Adding to concerns for tech investors would be the performance of the Grayscale Bitcoin trust (GBTC). In the first big bitcoin boom, share outstanding in GBTC barely grew, but in the most recent bitcoin boom, inflows into GBTC have been large. Perhaps even more disconcerting is that inflows have continued even during the recent weakness in bitcoin.

Looking at the market cap of GBTC from inflows and capital appreciation we can see the composition of gains now is in stark contrast to the boom in 2017.

Taken altogether, it would seem that the tech space is getting very close to entering the slope of hope phase of capital markets.