Typically, the spread on high yield bonds and VIX follow each other. Both are measures of risk or fear. The rise in VIX this year has not been accompanied by a widening in high yield spreads. This would place the S&P 500 in a buying opportunity scenario as seen in 1998 during the Asian Financial Crisis, and in XIV induced sell off in early 2018.

Historically speaking, the VIX was purely a simple measure of implied volatility on near dated S&P options. The higher the VIX, the more traders believed that the S&P could be volatile. However, in the long period of ultra low interest rates “selling volatility” has become a popular trade with retail investors. XIV ETF, that spectacularly blew up in 2018, is one aspect of this popularity.

The biggest single market for “volatility selling” globally is Korea. The retail market is always short volatility, and has a tendency to “roll” its exposure. This has two main effects on volatility. First, this has moved VIX from an independent observation of market sentiment, to a product that drives market sentiment. In plain words, it used to be that if market fell, then VIX would go up. It is now possible to VIX to rise, and this to cause the market to fall. This tendency is partly caused and exacerbated by Korean autocallables. Issuance is high when VIX is low (putting pressure on VIX to fall more) and issuance collapses with VIX spikes. As of December 2021 data, Korean issuance is back at highs.

The collapse in autocallable issuance in 2020 was obviously driven by Covid. The 2015 collapse in issuance was driven by weakness in the HSCEI market, which at the time was the most popular market for Korean autocallables. The HSCEI had been driven higher in 2014 and early 2015 in a liquidity induced rally, but as liqudity ebbed, falling HSCEI levels led to a collapse in autocallable issuance and a large spike in VHSCEI (the HSCEI equivalent of VIX).

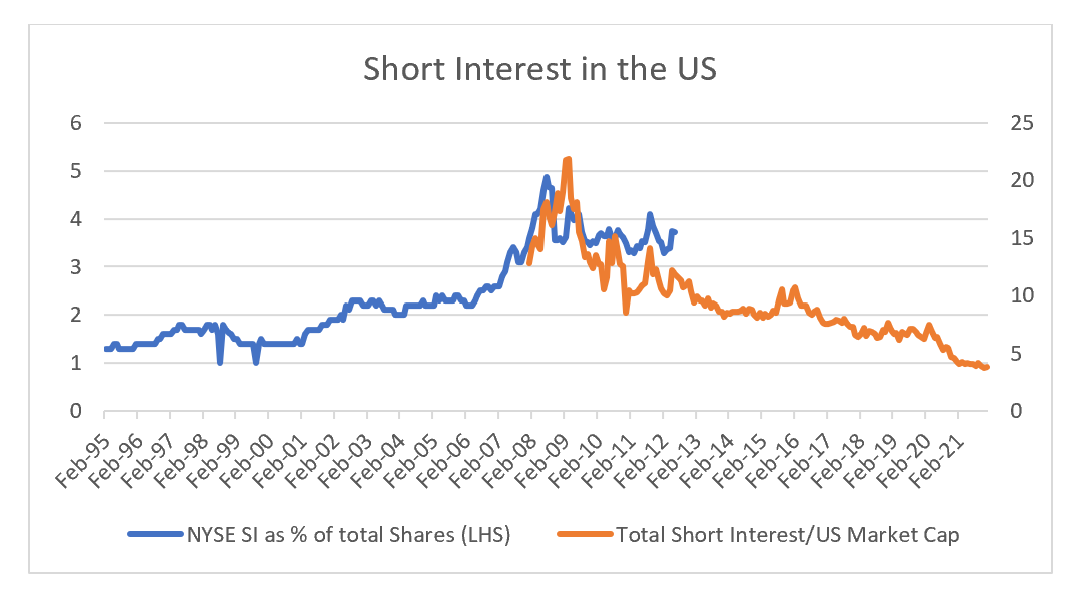

Could we see a similar autocallable led spike in VIX and similar 40% decline in the S&P 500? Covid induced liquidity rally has reduced short interest in US stocks to very low levels.

High yield debt now yields well below inflation. Any more to reestablish a premium to inflation would put downward pressure on equities.

If the Federal Reserve does remove market support to combat inflation, then the combination of large short volatility positions, very low yields and rising inflation could lead to a substantial volatility spike, and a severe sell off in the S&P 500.