I try not to take absolute positions, but relative positions. In the inflationary world that we live in, I think inflationary assets will do well, UNLESS central banks run tight monetary policy. What that means in practice for me, is that I like Gold (GLD) relative to Treasuries (TLT). GLD/TLT has been good.

I have always worked in relative terms - as I always fear political reaction to one side of my trade working. If one trade works (gold goes up, lets say), I run the risk that the Fed suddenly gets hawkish, and gold tanks. This make sense to me. But after the fact, people will say to me : “hey Russell, your short TLT isn’t working, why do you still hold it?” This is always the way - people always love the winning side of the trade, and hate the losing side. For me, personally, I cannot take the GLD side of the trade without the TLT side of the trade - it would be too risky for me.

In my career as a fund manager, I have had many client conversations like the above, and a year or two later, even though I have done well, they suddenly redeem. When I ask why (nothing more frustrating that redemptions when you are doing well), the answer inevitably is “we copied your trade, but we left off the hedge as it was not working - and we just got smoked, because you were right, we needed the hedge”. If something is inevitable, just because it did not happen today, does not make it less likely in the future, in fact the opposite is true - but investors and markets will always be backward looking.

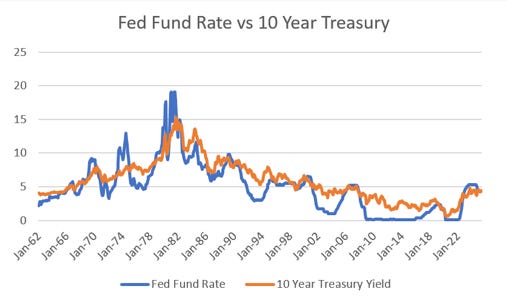

So the question is, does short TLT still make sense? If I think we are still in a pro-labour era, then yes. Back in the 1960s and 70s, when wages rose quickly, the Fed needed to run tight monetary policy (policy rate above the 10 year yield - the opposite of what we saw in the pro-capital era from 1980 to 2020). In concrete terms, I think pro-labour era policy rate tends to be higher than 10 year Treasury yield, and in a pro-capital era, the policy rate tends to be below the 10 year Treasury yield.

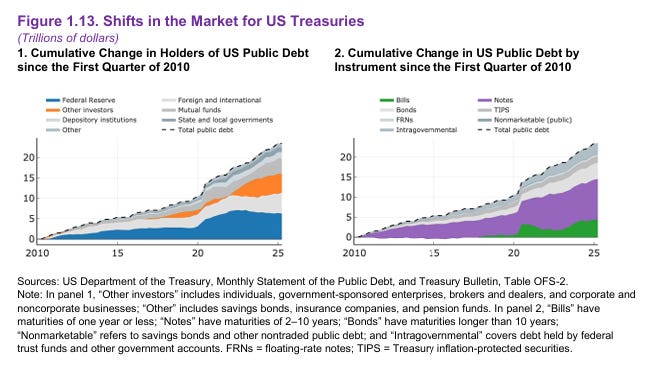

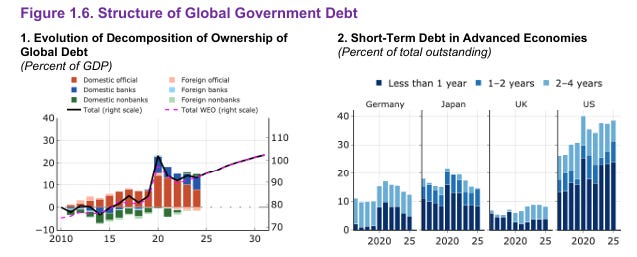

For me, the politics of a short TLT trade still make sense. But I was reading through a Chris Wood’s post on substack on Treasuries. I have read Chris Woods for a long time - and he was early on Fannie Mae and Freddie Mac, and the Eurocrisis. I always sleep better when my positioning is aligned with Chris - and he was pointing out the increasing messiness of the US treasury market. I steal some of his charts below. Let me start with some IMF charts The left hand side chart shows the rise of “Other Investors” in the US public debt (read as hedge funds) - who were virtually non-existent until 2022. This makes sense to me as “official” buyers (other countries) stop buying treasuries.

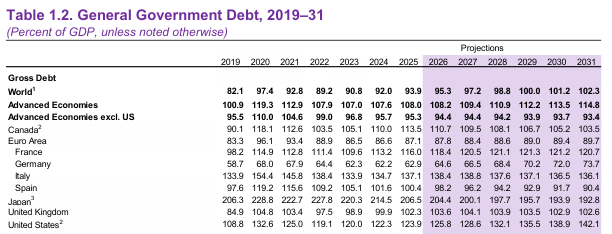

There was a time when Japan really stood out for unsustainable debt load - but Japanese debt load is falling as the US is rising - which is what you expect in a rising wage, strong stock market environment. The continuing rise in US debt is very unusual.

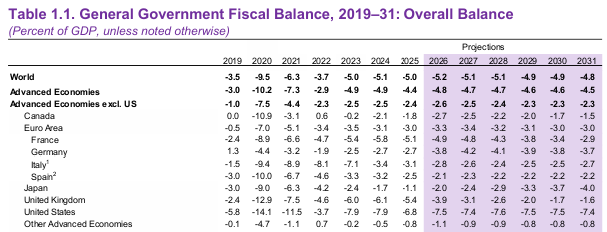

US 7% of GDP fiscal deficits are very eye catching - especially given relatively strong economic growth.

As is the reliance on short term debt for the US. The implication is that if the Fed did raise rates, the US debt dynamics would worsen very rapidly.

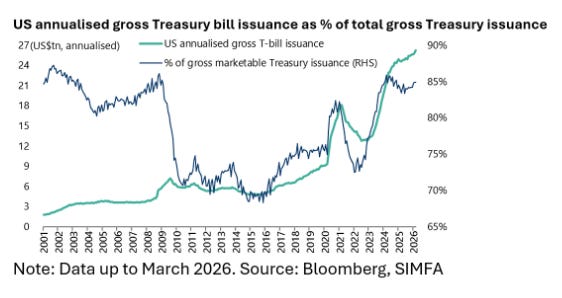

You can see how much bill issuance has increased in the US. This chart is from Chris Woods.

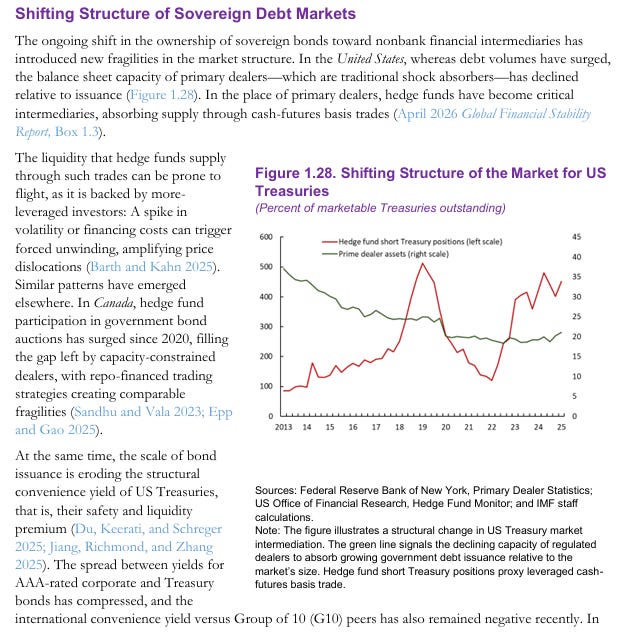

For long time readers, they know I hate the clearinghouse reform. It essentially moves risk pricing in markets from forward looking banks, who can go bankrupt if they get it wrong, to backward looking clearinghouses, which cannot go bust - and then require governments to bail out markets when they get it wrong. Much of the demand for treasuries come from basis trades, which the below article makes clear. The basis trade is run through clearinghouse these days. When margin calls are made, treasuries can and do fall as cash needs to be raised for margin calls, which can then exacerbate liquidity issues. The Gilt Crisis after the Liz Truss budget is an example of this.

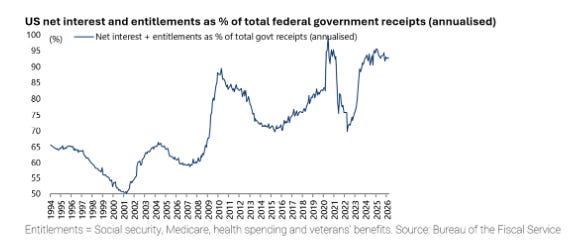

Probably the most killer chart from Chris Woods is this one. Net Interest and entitlement make up near 100% of government receipts - even though interest rates still look too low to me, and unemployment is low in the US. This is probably why treasuries fall when recession fears arise - there will be no money to pay for treasuries.

While this note is about TLT, it also answers one of the questions I have been asked to address in my upcoming investor day. Do we need long/short funds? My read, for what it is worth, is that much of the US growth story is a pure fiscal one. All the extra money that inflation and growth generates the US government is just spent - nothing is now saved for a rainy day. Or in other words, back in 2006, the US was abusing the mispricing of mortgage backed securities, today the US is abusing the mispricing of sovereign debt. The simplest trade might indeed be just long gold - but back in April of 2025, we saw treasuries sell off during the Liberation Day Tariffs sell off.

For me, this was a sign that the Treasury market was breaking, and that the growth story for US equities was weakening. When this was followed up with the break out of gold versus the S&P 500, and general weakness in private equity/credit - it felt to me like it was time for a long/short fund, and time for weakness in TLT.

All of this makes for a good story, and so far matches up with market action. But I am also aware that it could just be a good story and market moves are just spurious correlation. But all good trades start with a good story - and this story seems to say that TLT should be a good short. Lets see.