There was a time when a prospectus was a dime a dozen. As an analyst in the 2000s, my main job was to read them and then go the management lunch, and work out if they were a buy or not. I love a good prospectus - its the only time management has to be clear and up front about risks. But with the rise of private equity and venture capital, IPOs have become much rarer. But today we get to go through a truly interesting prospectus. Above picture is taken directly from the prospectus. You can have a read yourself here. For such a momentous IPO, basically the key feature is that the IPO is needed because the capex into AI is larger than the cash that can be generated from its excellent rocket launch and connectivity businesses.

Not included in the above is that the IPO will allow SpaceX to purchase Cursor USD 60bn. There is quite a hefty termination fee, so obviously Elon is very keen on this deal. Cursor is an AI powered coding company, and was something that Grok was missing when compared to the other big AI companies. It also provides a ready made corporate client list.

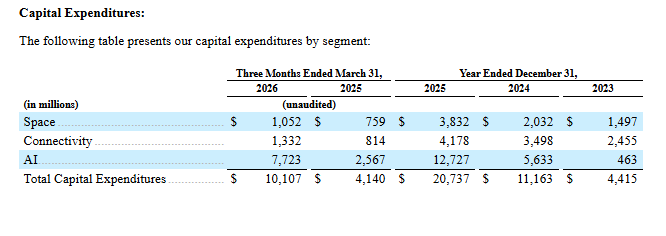

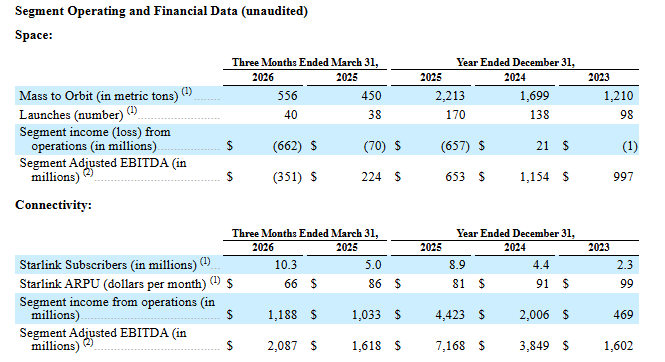

I am not going to give you a detailed financial analysis, AI and plenty of other Substacks can and will do that for you. But I will give you my read. Its pretty transparent that you are getting two excellent businesses, the launch business and Starlink, and one speculative venture. The Space business only lifted 2,000 metric tonnes into space, or about 5 International Space Stations (420 tonnes). If a moon base is to be built, this number will have to go up exponentially, and it has a huge cost advantage. Starlink has 10m customers now - and with a ARPR of USD 66 per month is not that expensive. Not hard to foresee 100m subscribers in this business.

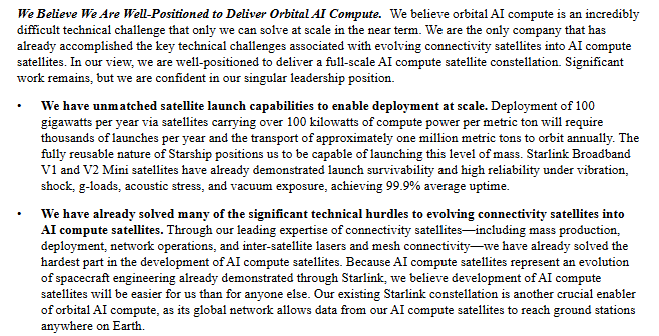

AI is a cash sink, but it is meant to be. But its pretty explicit that the AI business is the business that could really surprise to the upside. The theory of space based data centres is very interesting.

So far as expected. But I have two different takes on the SpaceX IPO. First of all, it confirms in many ways, the rising cost of capital theory. The rising cost of capital for governments is beginning to force some changes in capital markets. There is no way not to see equity valuations as expensive relative to government bond yields.

But the credit market has been increasing harsh on companies borrowing for AI. Softbank and Oracle CDS has been showing that.

So we are seeing the return of equity markets as the source of capital. For years the share count for the S&P 500 was falling, but now we have seen a turn as equity gets issued. We are not at dot com levels of issuance yet - but with the IPO pipeline opening up, this should climb higher, especially if government bond yields keep rising.

The second observation I would make on SpaceX IPO, is that Elon Musk really hates Sam Altman. I am using the word HATE, about Sam Altman. I suspect Elon Musk has a driving urge to be number 1, and a overdeveloped sense of vengeance on those that have done him wrong. For me, the SpaceX prospectus make it clear that Elon wants to destroy OpenAI.

So what has he done to make me think that? Not only has agreed to purchase Cursor to have a more competitive product, the prospectus also notes that the entire Colossus facility has been lease out to Anthropic at a cost of USD1.25bn a month.

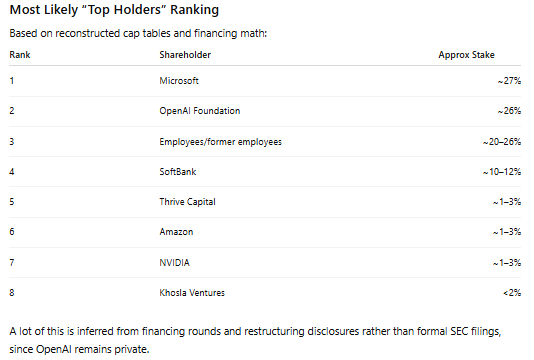

He also has been relentlessly pushing Grok in twitter - which obviously allows him to compete with ChatGPT on the consumer side, if not competitively yet. All of this raises an interesting questions about the potential OpenAI IPO. With Microsoft moving away from OpenAI, and Elon Musk supporting Anthropic, OpenAI will need to raise a very substantial amount of capital from the market to compete. If Microsoft also looked to sell some of its stake - would this supply overwhelm demand?

I guess what I am saying is that capital has become a competitive weapon - and it still looks like OpenAI is at a disadvantage. Softbank has bounced on the OpenAI IPO announcement.

But its CDS remains strangely unmoved. Credit markets tend to be more “show me the money” type of markets (not always - but can be).

This makes sense to me, as SpaceX IPO is signalling even more capital is going to be invested in this area. As long as growth rates remain good, equities should be okay I guess, but the rising cost of capital is causing equity issuance to pick up. This is a change from the last 10 years or so. Is OpenAI still in trouble? Well if Oracle catches a bid, then we can assume the IPO will solve the capital raising issues. Time will tell.