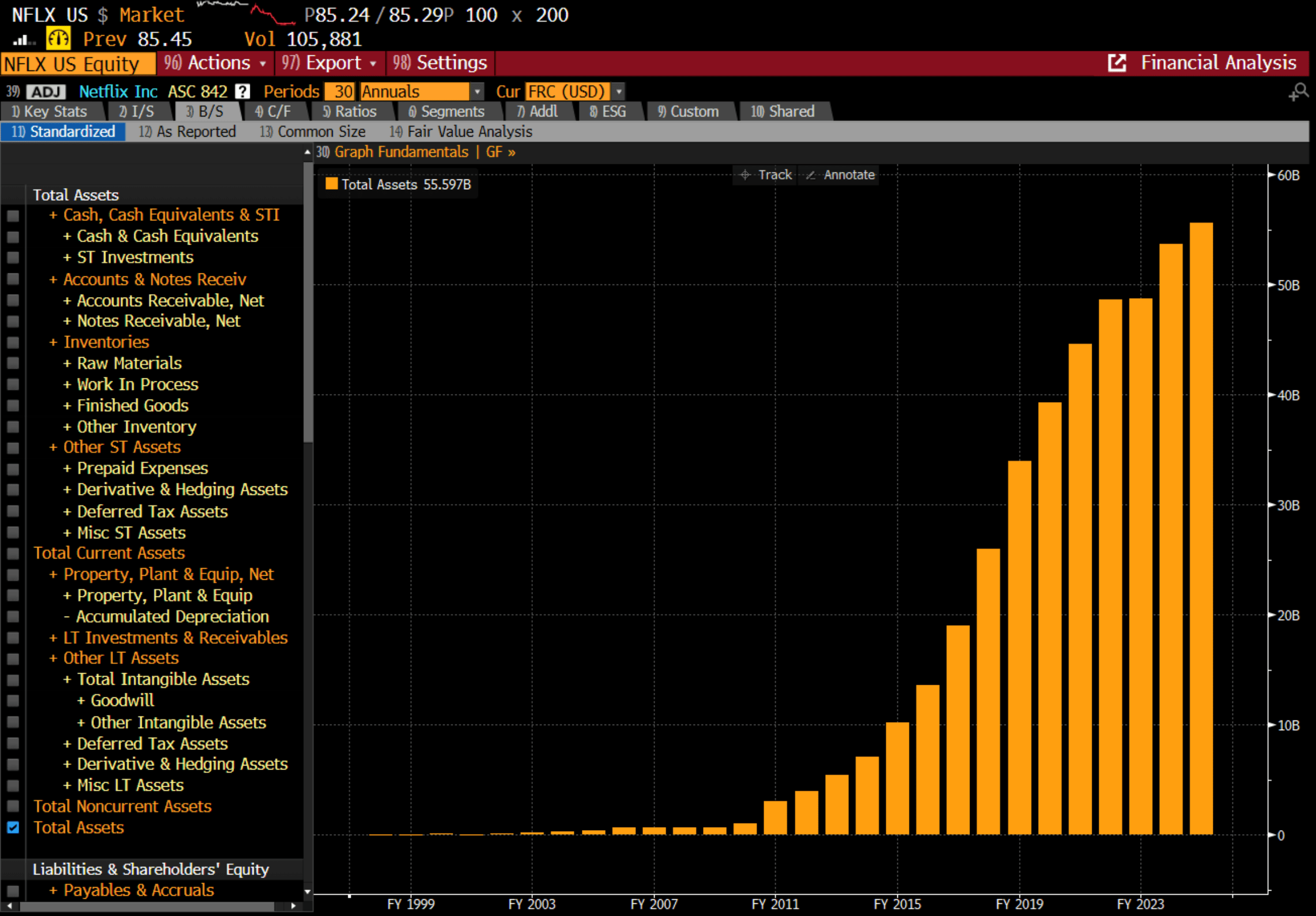

There was a time, not that long ago, when the cheapest provider would be the corporate winner. Remember the days when online shopping was always the cheapest option? Or when streaming was much cheaper than buying DVDs? This was a period when government enforced competition, which has sadly disappeared. These days, particular in tech world, its how much capital you raise that is the most important factor in determining a winner. A good recent example was Netflix, who during the “streaming wars” massively increased its balance sheet which drove up the cost of content.

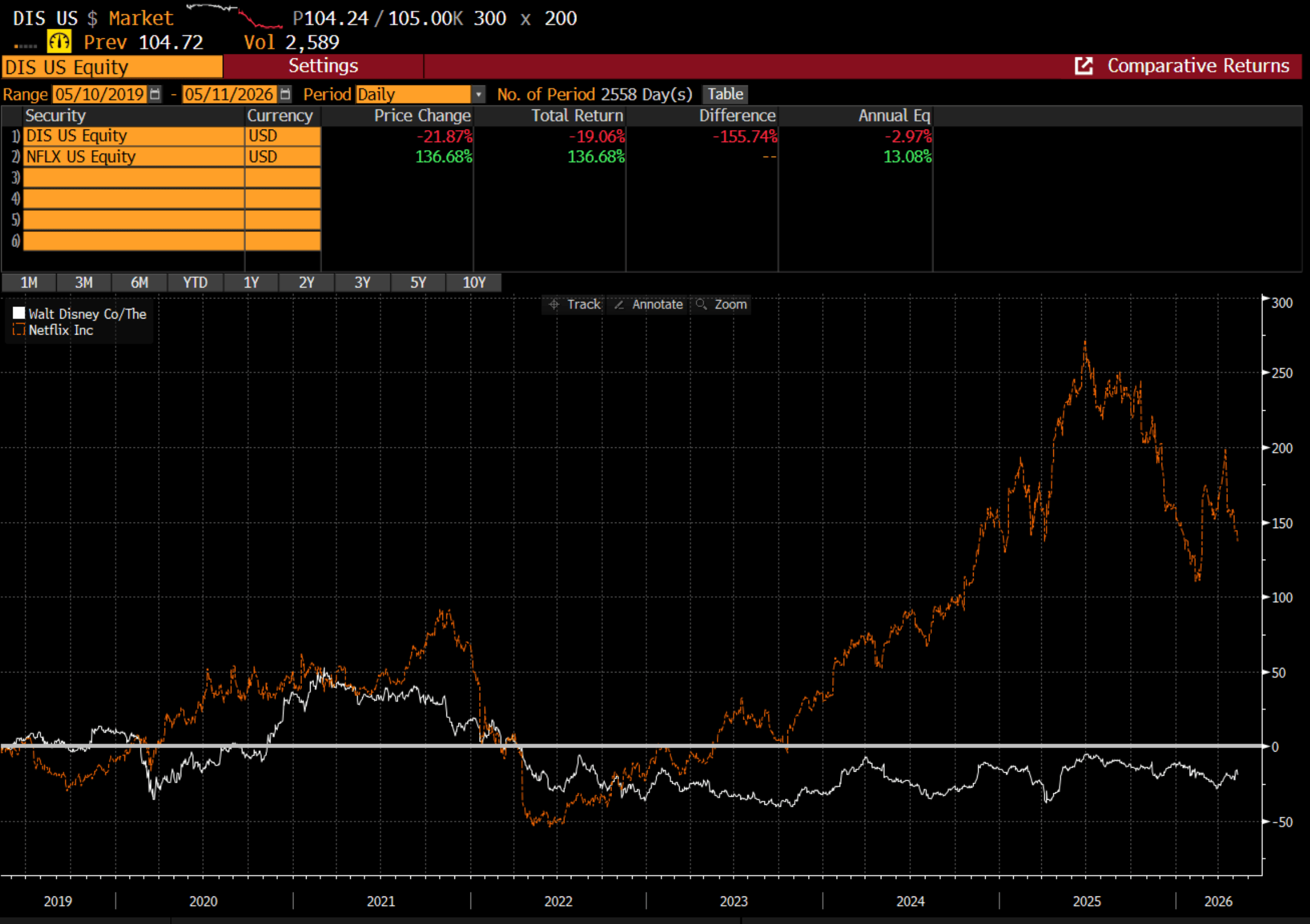

Disney tried to compete for a while, but ultimately Netflix won.

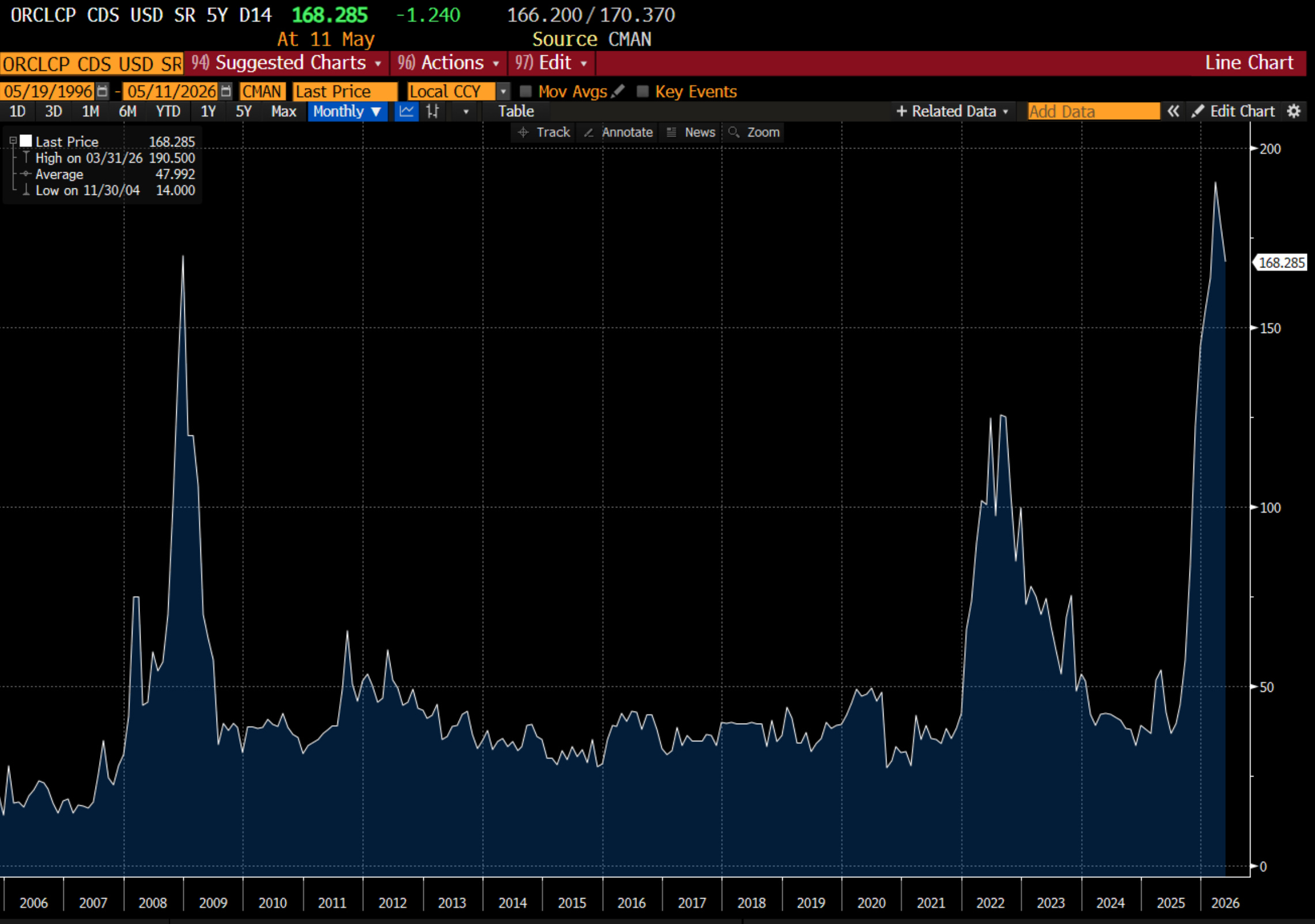

And once it won, content prices fell again, and content creators got squeezed. In AI, we are seeing a similar dynamic play out. Masayoshi Son, the founder of SoftBank, virtually invented blitzscaling with an early investment into Alibaba, where he encourage Jack Ma to build quicker, or his capital would go to competitors. In the AI race, we have the hyperscalers, and the AI labs, OpenAI and Anthropic. One of the more intriguing aspects in the current AI boom has been the weakness in some of the AI names CDS. Oracle CDS has been weak.

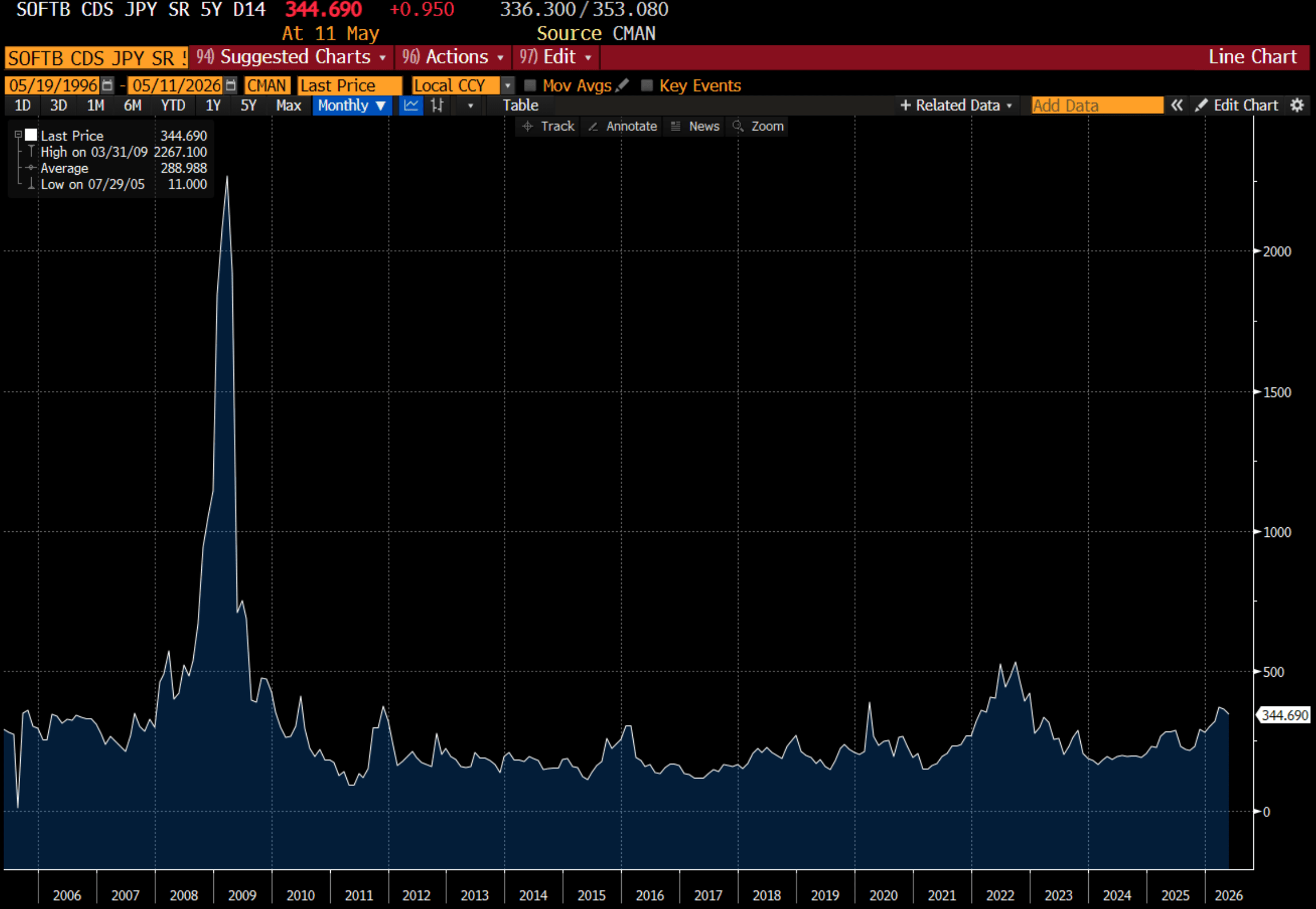

As has Softbank Group.

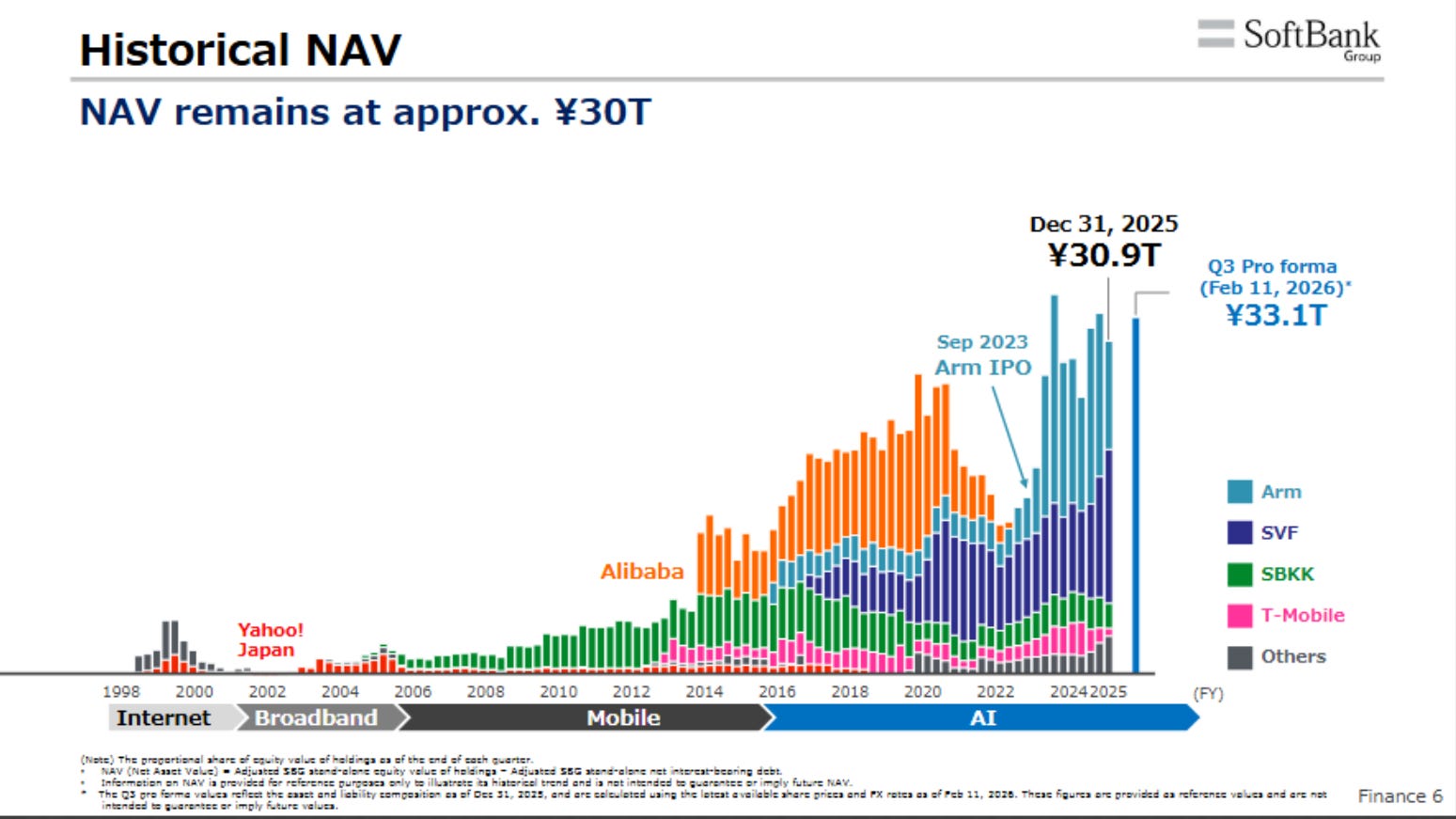

Softbank is really more of a concentrated investment firm, with a number of high profile investments with a mixed track record. Alibaba was a great success, WeWork not so much. In recent years, is has been busy turning itself into an AI focused investment vehicle.

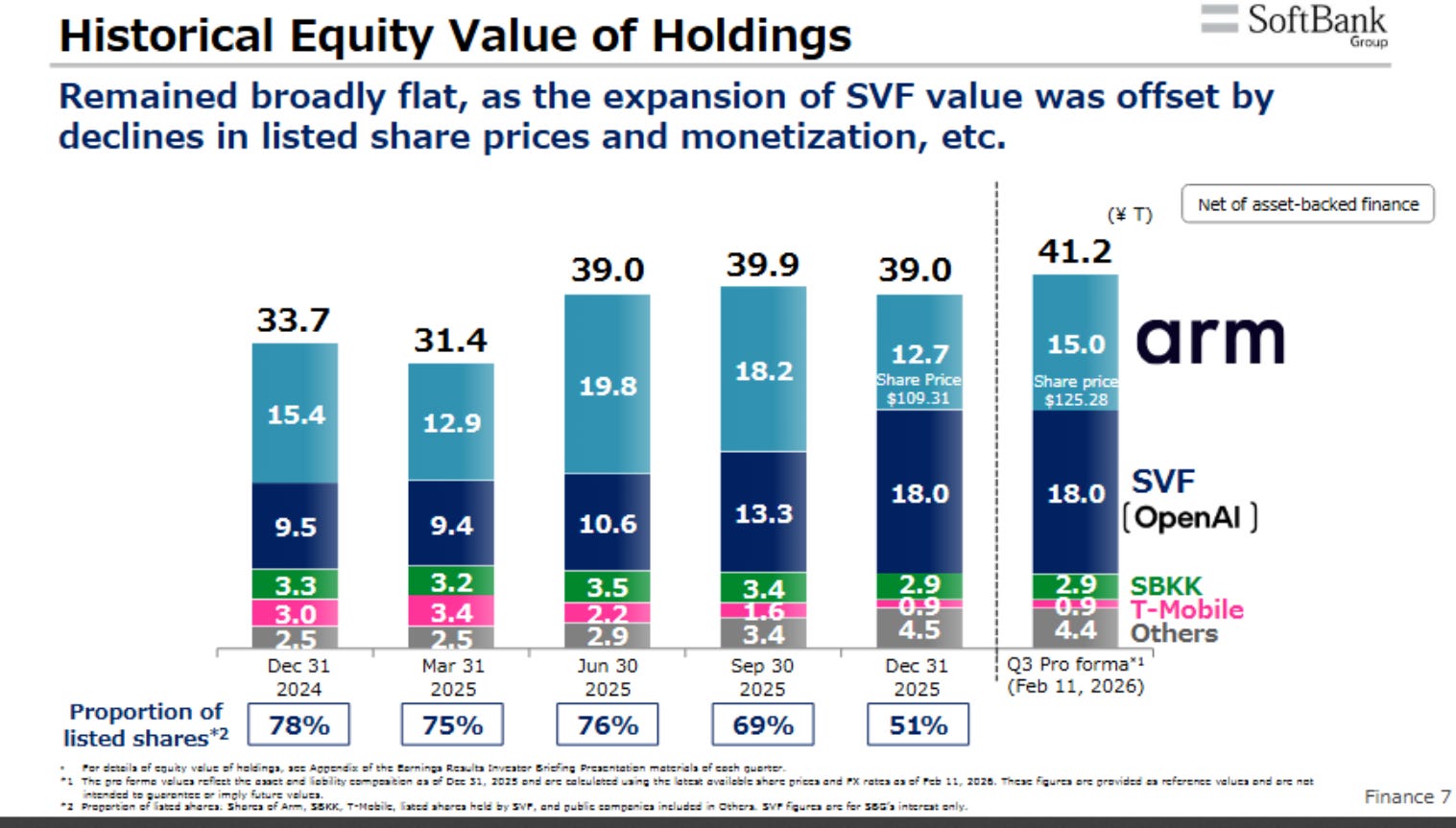

As of today, ARM and OpenAI are its two biggest assets.

Softbank was looking to raise capital by taking out a loan backed by its share holding in OpenAI, but saw some push back from lenders.

Softbank also have about USD 20bn of margin loans supported by its holding in ARM. ARM is one of the more expensive tech stocks out there - trading at 45 times EV/Sales.

SoftBank, Oracle, OpenAI some other partners have attempted to blitzscale the AI market with its Stargate project.

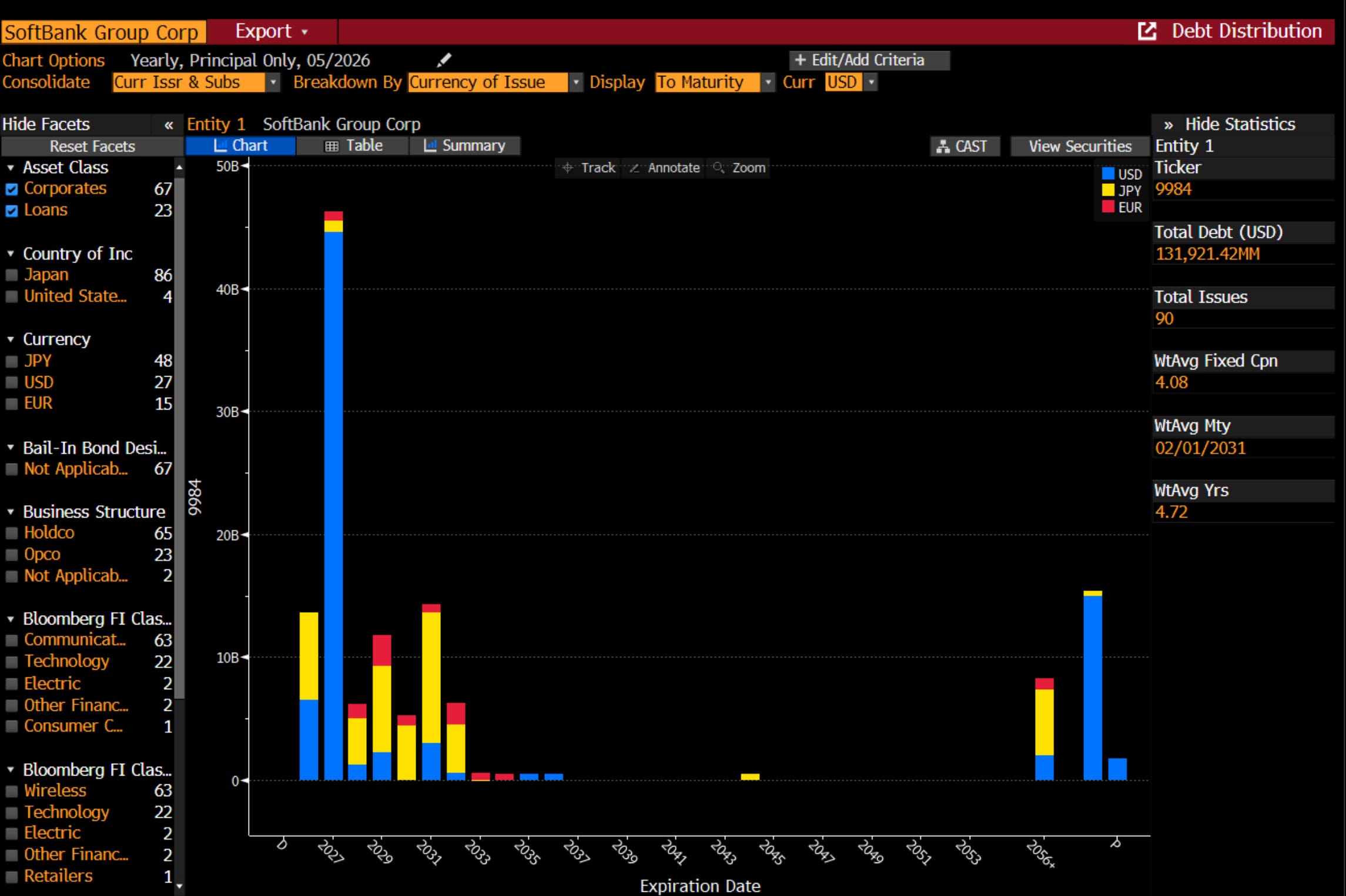

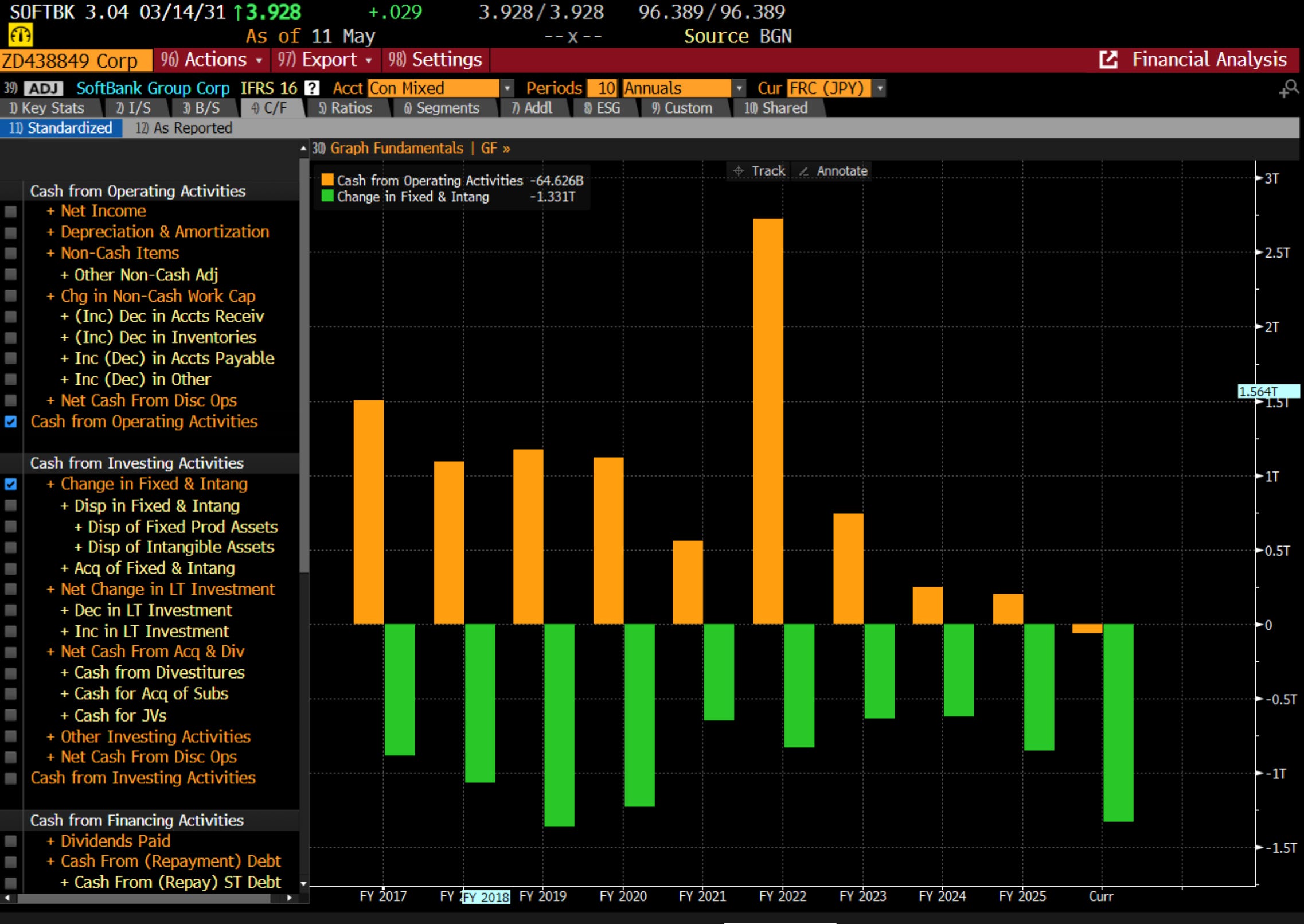

Softbank is increasing looking like the “soft flank” in the OpenAI v Anthropic battle for AI supremacy. Softbank has USD 130bn of debt outstanding (not including margin loans against ARM and OpenAI). Most is in USD, but there is a fair bit of Japanese debt as well.

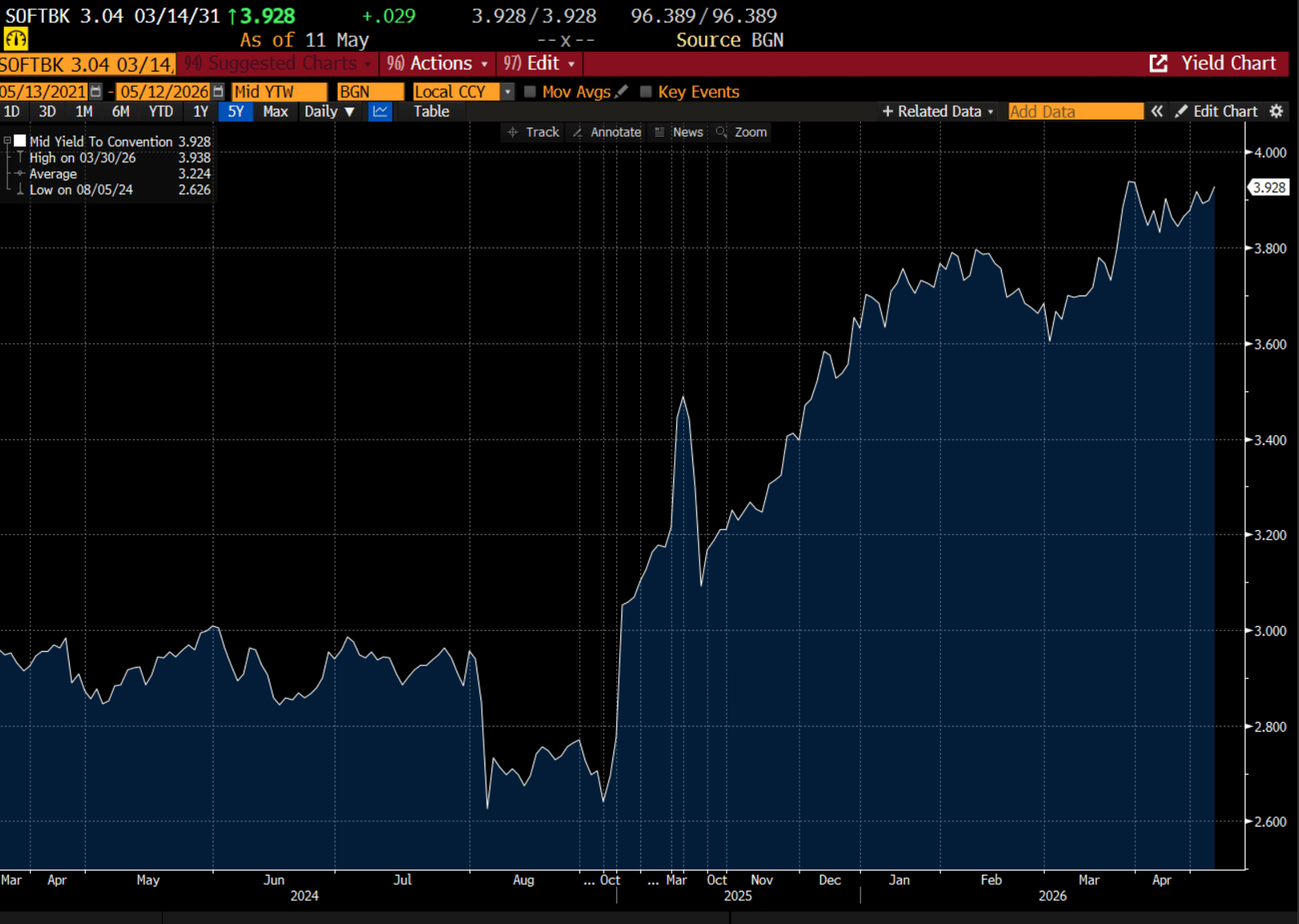

In line with JGBs, the yield on this debt has risen substantially.

Not hard to see why - operating cash flow is poor, but capex is high.

One of the reasons I have been cautious on markets is that I saw capital becoming scarce - and we are now seeing that in the AI space - as these huge corporates keep tapping the market for more and more money. The question is when do bond markets break? When do markets stop asking how much do you want to borrow, and start asking when are you going to pay me back. We may be getting closer than you think.