It is fairly widely known that a weak USD dollar tends to be good for commodities and for emerging markets in general. I always thought the transfer mechanism was two pronged. One, US dollar debts become much easier to service, improving credit conditions. And secondly, a weak dollar encourages capital flows out of the US and into carry trades, which also improves capital flows. South Korea has always been a good indicator of this strong currency good, weak currency bad type of scenario. Against the US dollar, the Asian Financial Crisis and GFC are very clear periods of a weak won, and since 2020, Won has been pretty weak again.

This sell off in the Won in 2020 is hard to match up with a bullish S&P 500. Where is the financial crisis? But if we look at Korean won terms in Yen terms, things make a lot more sense. Using the capital flow model, when Yen devalues its also puts downward pressure on the Won. In 1997, this led to Korea having to break its dollar peg, and in 2007, led to another huge devaluation as various credit structures blew up in Korea.

What is odd about the current Yen/Won exchange rates is that its is back at 1997 levels, despite CPI in Korean having doubled in the period, while Japan has maybe risen 8%.

Given the movement in exchange rates, you should not be surprised to see the Nikkei doing better than the Kospi. Since 2013, Nikkei is up over 300%, while Kospi is up 25%.

This affects all of East Asia in particular. Taiwan runs a 12% of GDP current account surplus, and has dominant market share in high end semiconductors. You would expect its currency to be surging. It is not.

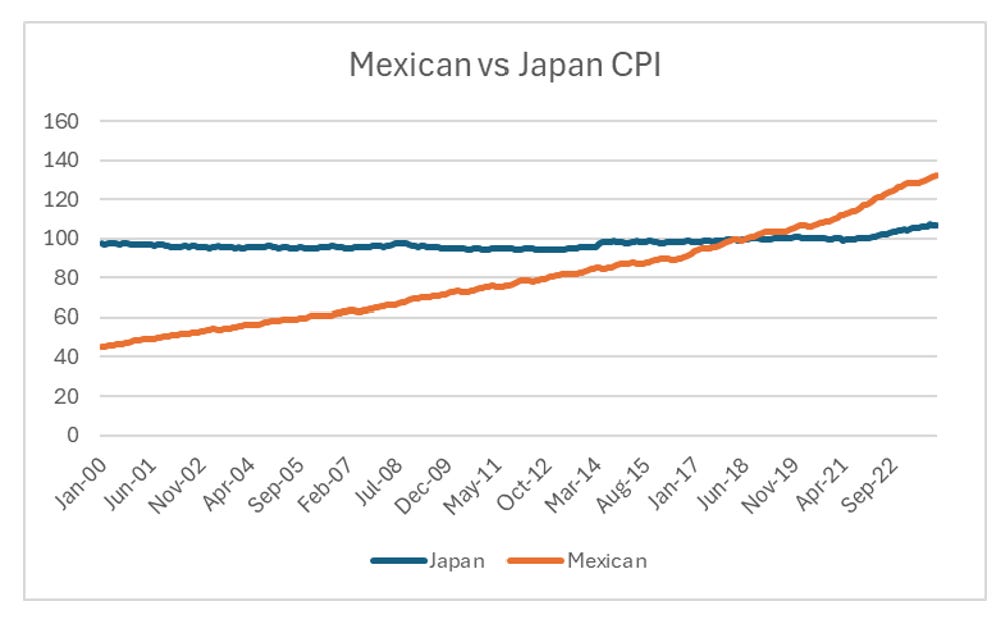

The distortions in Yen are truly epic. If I a look at Yen v Mexican peso, it is back at levels seen in 2004.

Mexican CPI has doubled over that period.

Just like Korea, equity returns have been lacklustre.

Historically speaking, the Japanese devaluation policy has been a massive own goal, with huge financial losses in the AFC (caused by Yen devaluation) and the GFC (helped by Yen devaluation). But this time, China has chosen to resist the devaluation pressure that a weak yen other weak Asian currencies is putting on Chinese Yuan. Certain financial types will hyperventilated over the 20% fall in Yuan versus the US dollar, but compared to real currency devaluations this is nothing. Japanese investors I think recognise that a Chinese devaluation does not look like likely, which is why JGBs are beginning to sell off, after almost three decade uninterrupted bull market. Note in 2015, when Chinese devaluation fears were highest, JGB yields collapsed to all time lows.

China and the world have turned pro-labour, which is putting upward pressure on inflation and bond yields. Somehow, the BOJ is still living in the past. When do they wake up and smell the coffee?