Japan is an unusual country. For decades it defied economic analysis. As Simon Kuznets said, there are four types of countries: developed, undeveloped, Japan and Argentina. And when I started working in finance, Japan was also given special treatment. The Japanese macroeconomic numbers of a large fiscal deficit combined with low interest rates should mean the Yen collapses, and inflation should be running rampant, which lead many funds to short JGBS - a trade that became the original “widowmaker” trade. I spent a lot of time trying to come up with a more “holistic” model of the world, that would explain Japan, JGBs and the Yen. The model, if that’s the right word, is that Japan is the Saudi Arabia of savings, and where it capital flows to booms, and when it pulls its capital you get a bust.

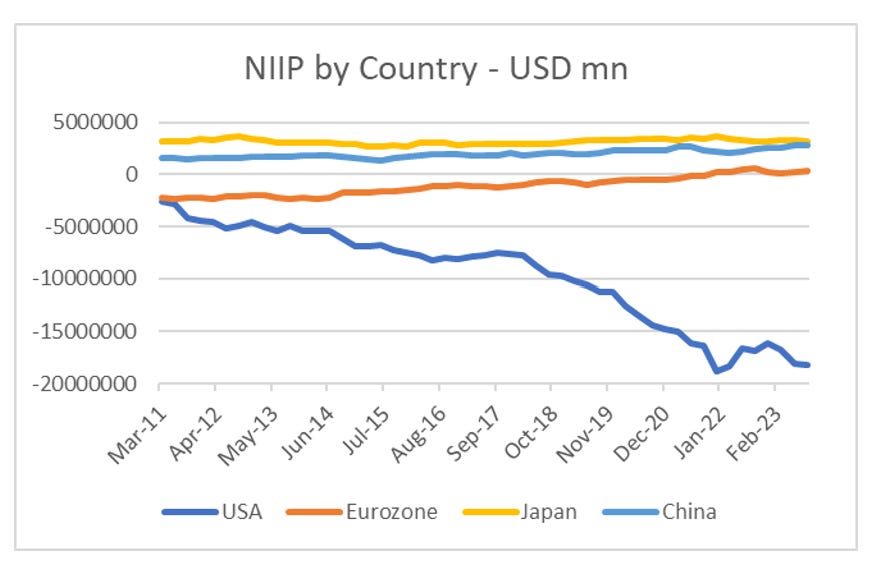

Anecdotally this feels right. In every big financial crisis, Japanese institutions tend to me knee deep in financial crap. But anecdotes are not rigorous analysis, so I set out to try and prove it. One of the first data points I looked at was net international investment position (NIIP). Japan consistently has the largest positive NIIP in the world. And historically speaking, a large negative NIIP was a warning sign, although this has not worked with the US from 2016 onwards.

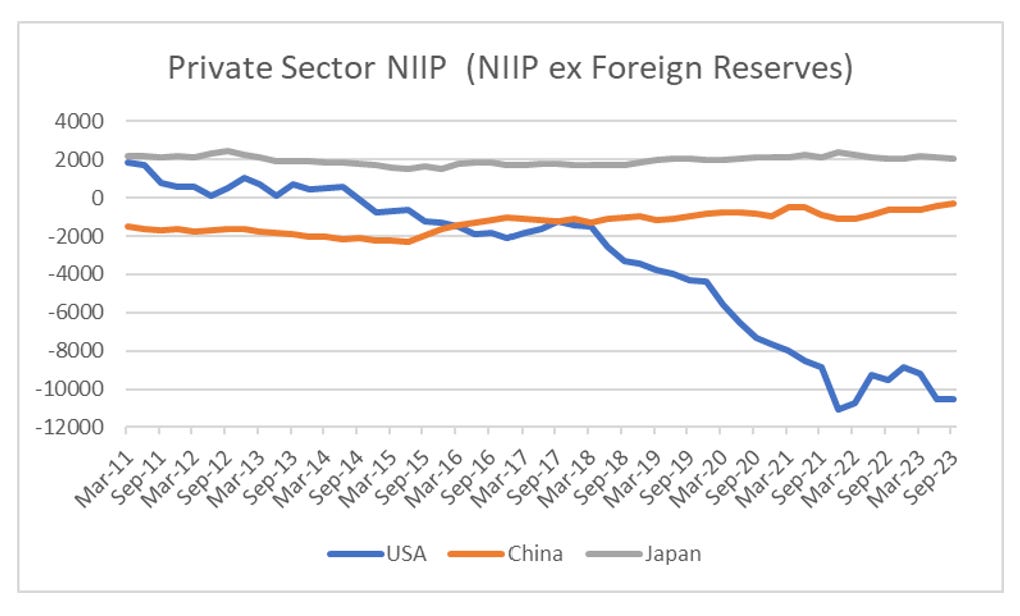

NIIP data mixes private sector and public sector holdings. In particular, foreign holdings of treasuries tend to mean the US always has a negative number. So I strip out this data from China, Japan and US data to get a “private sector” NIIP. Private sector NIIP tends to shift with asset and currency performance. The long bear market in Chinese assets have pushed this positive. Japan, despite the performance of the Nikkei constantly remains positive, a sign of how flows in Japan tend to only be outwards.

Globally NIIP should add to zero - but it does not. The outlier is the US. Its private sector NIIP used to oscillate around zero, but in recent years has exploded higher. I suspect this has to do with US corporates and their tax avoidance strategies, but will just focus on Japan at the moment. NIIP is a big macro data point that captures relative movements in currency and stock markets, so it is possible just to argue that America and American corporates are awesome, and everyone wants to be invested. While I would not put in that terms, I would say the ability of US corporates to get laws enacted that benefit their own interests are without comparison in the rest of the world. But we can look at different data points to get an idea of Japanese influence. The BIS collect data on location of banks claim and liabilities. Japanese non-banks are the biggest lenders to the world.

If we look at how the Japanese non-bank claims have developed, ever since the Japanese bubble burst, the non-bank sector has rapidly increased claims overseas.

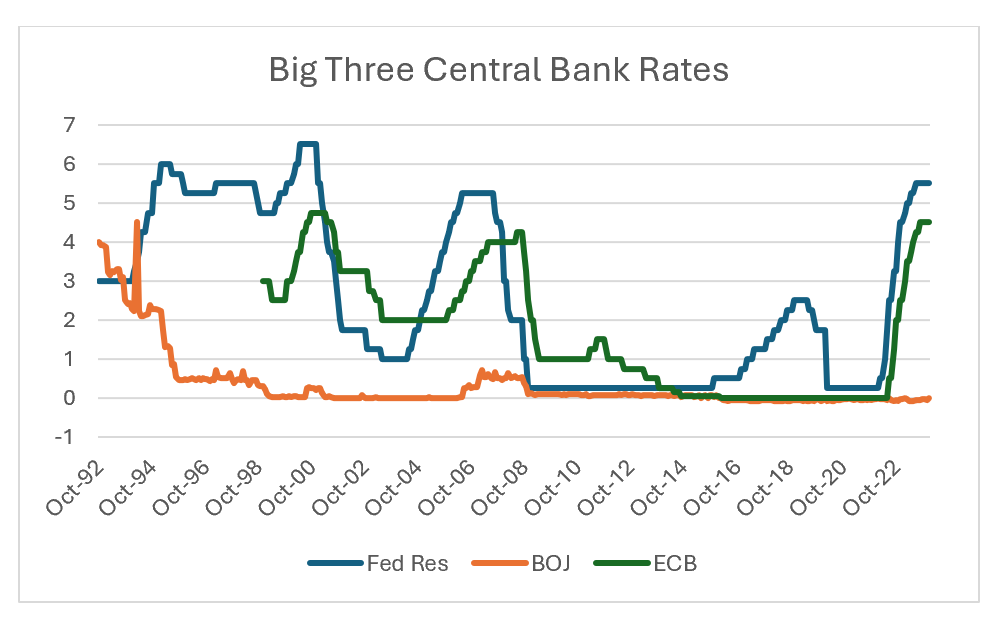

My argument is when the BOJ taps (not steps) on the brakes, all hell breaks loose. Very short rates have only risen occasionally in Japan. 1996 - Asian Financial Crisis; 2000 - Dot Com bust; 2006 - GFC and 2007 was the last time the BOJ raised rates.

Anyway, that’s the background. I will spend the weekend reading BOJ materials to see the likelihood they might actually raise rates, and then try an answer the more difficult question of what that means in a pro-labour world.