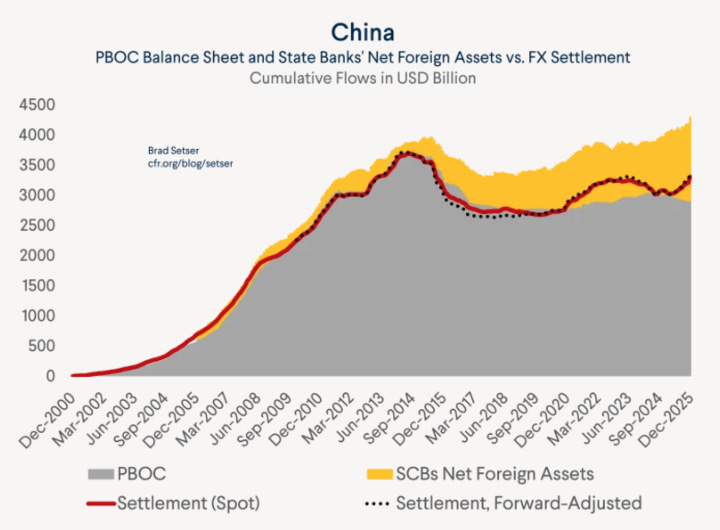

I have a lot of time for Brad Setser. In a recent FT article he claimed that China was still buying treasuries, but just via policy banks rather than as official foreign reserves. He provides this chart to support his view. Not the most intuitive chart, but basically the red line goes up when the Renminbi goes up, showing that banks in China buy more treasuries when the Renminbi goes up. The implication is that the banks are trying to slow the appreciation of the Renminbi.

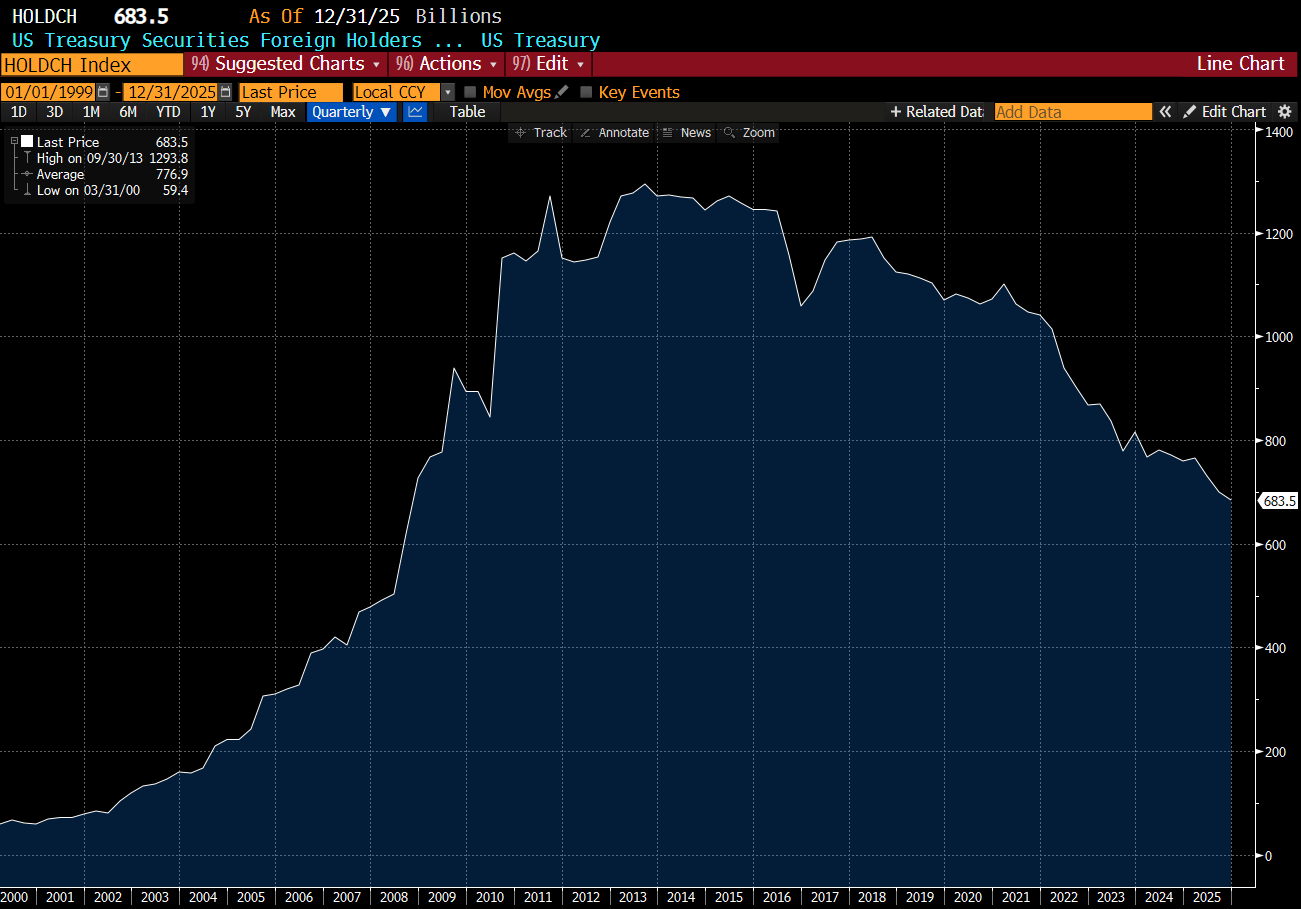

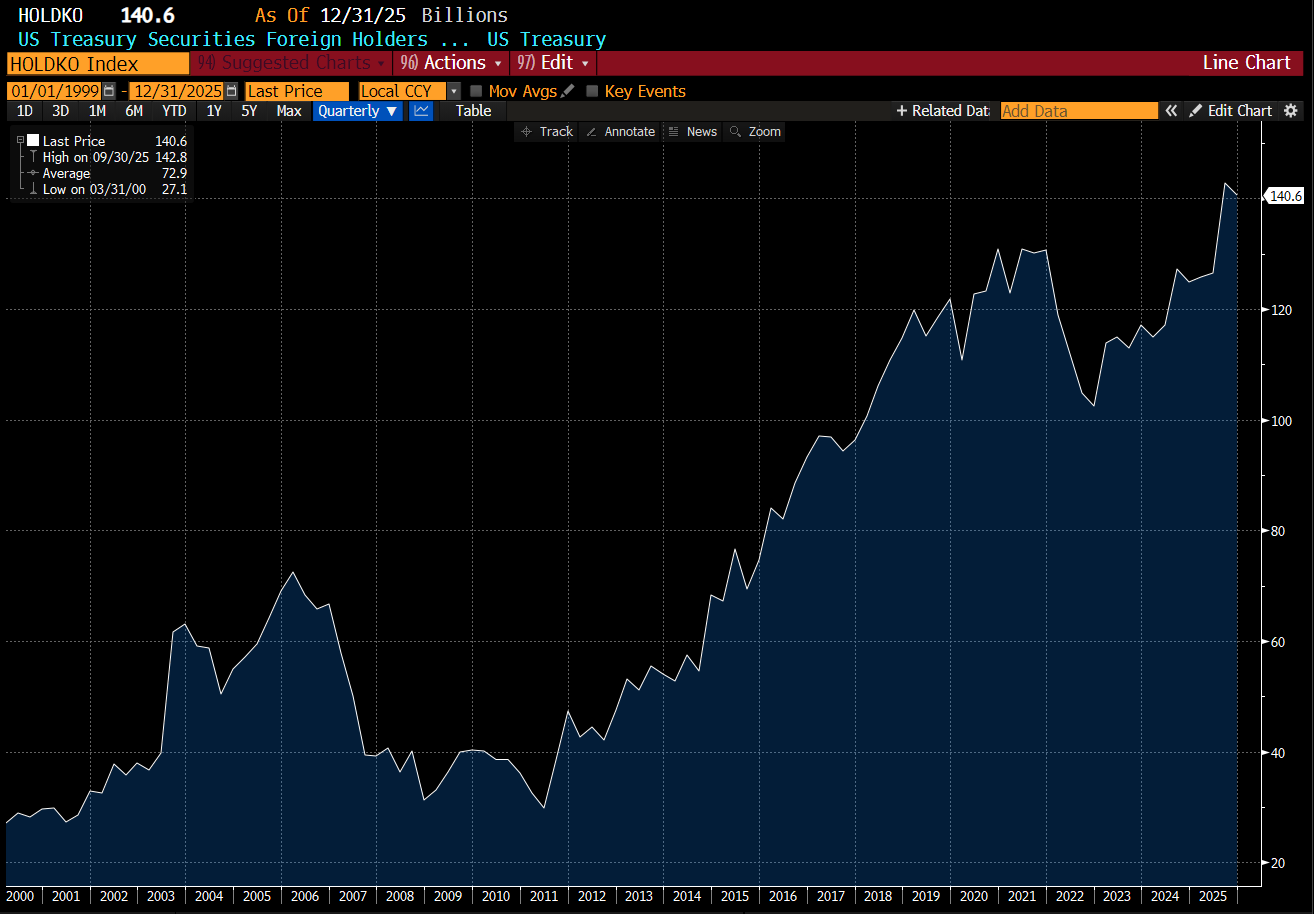

His article claims state banks bought USD 170bn of treasuries in December and January. This is a big number. For context, reported official holdings of US treasuries by China fell by USD 600bn over 10 years, and these number would suggest 25% of this fall was reversed in two months.

To be fair, China is running a USD 1.2 trade surplus, so if they choose to sterilise this flow, then there has to be a LOT of buying of something. Given the freezing of Russian foreign reserves in 2022, I would have assumed that China would not buy treasuries, and just gold. This has been one basis for the GLD/TLT trade - which has worked great.

The FT article is a shorter version of an article that Brad published earlier this year. The most interesting chart would be this one, which basically says that China is back at peak net foreign assets.

I always find China a funny place. Its definitely not an open western democracy, so knowing what exactly is going on is not always easy. But these days, trying to fully understand US economic policy is also not that easy either. But one thing about China is that the government generally tells you what it plans are, and then does it. So I think China is still trying to get out of it US assets - its problem is that it runs a huge trade surplus, and these trade surpluses are controlled by corporations and individuals. When they see the Renminbi appreciate, they want to bring money back to China, which forces the State banks into offsetting trades. And the Renminbi has appreciated this year.

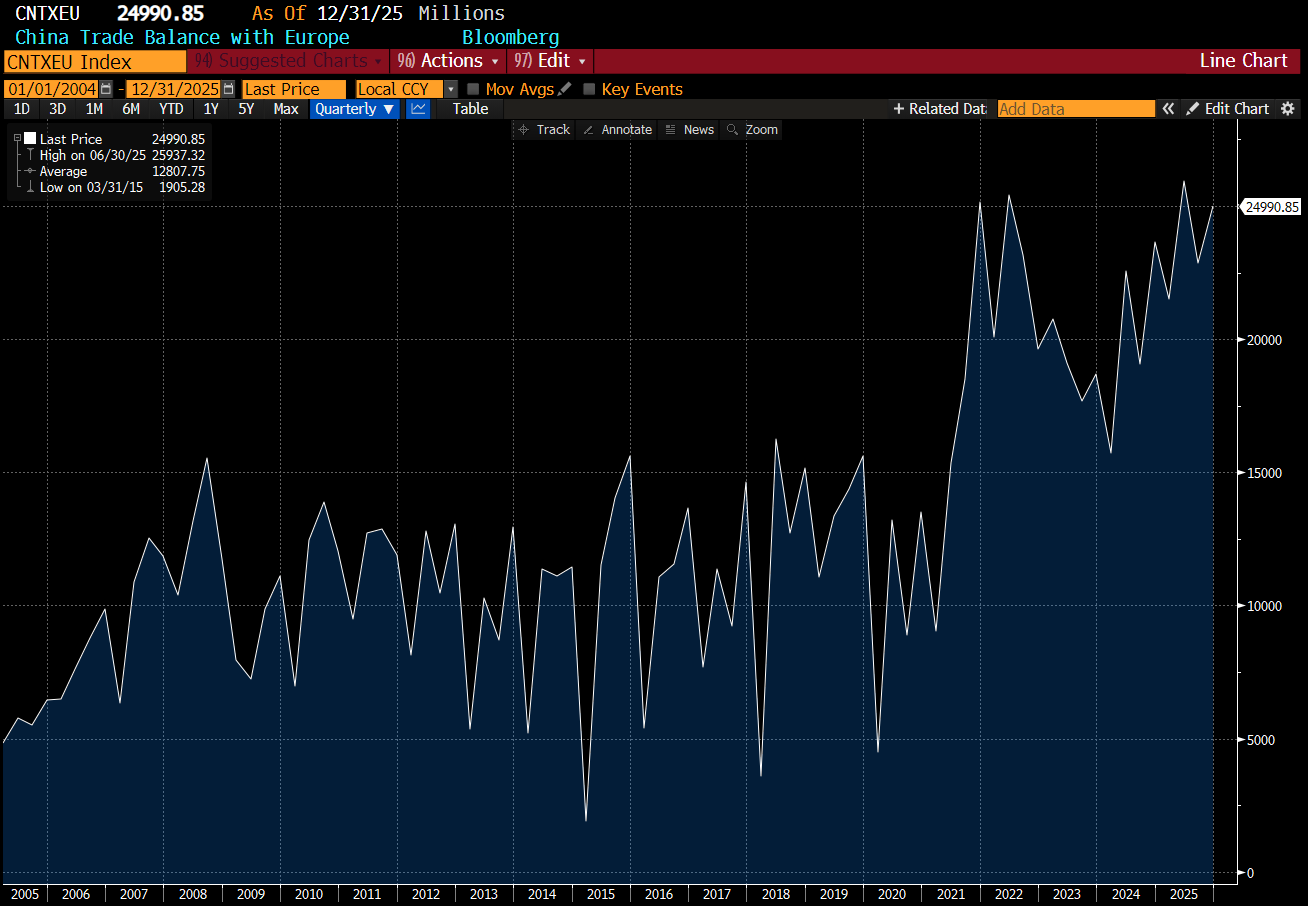

The problem China has is that its currency does look cheap now. If we ignore the US, China’s trade surplus with Europe is at record highs.

But the EURCNY cross rate remains at close to 10 year highs.

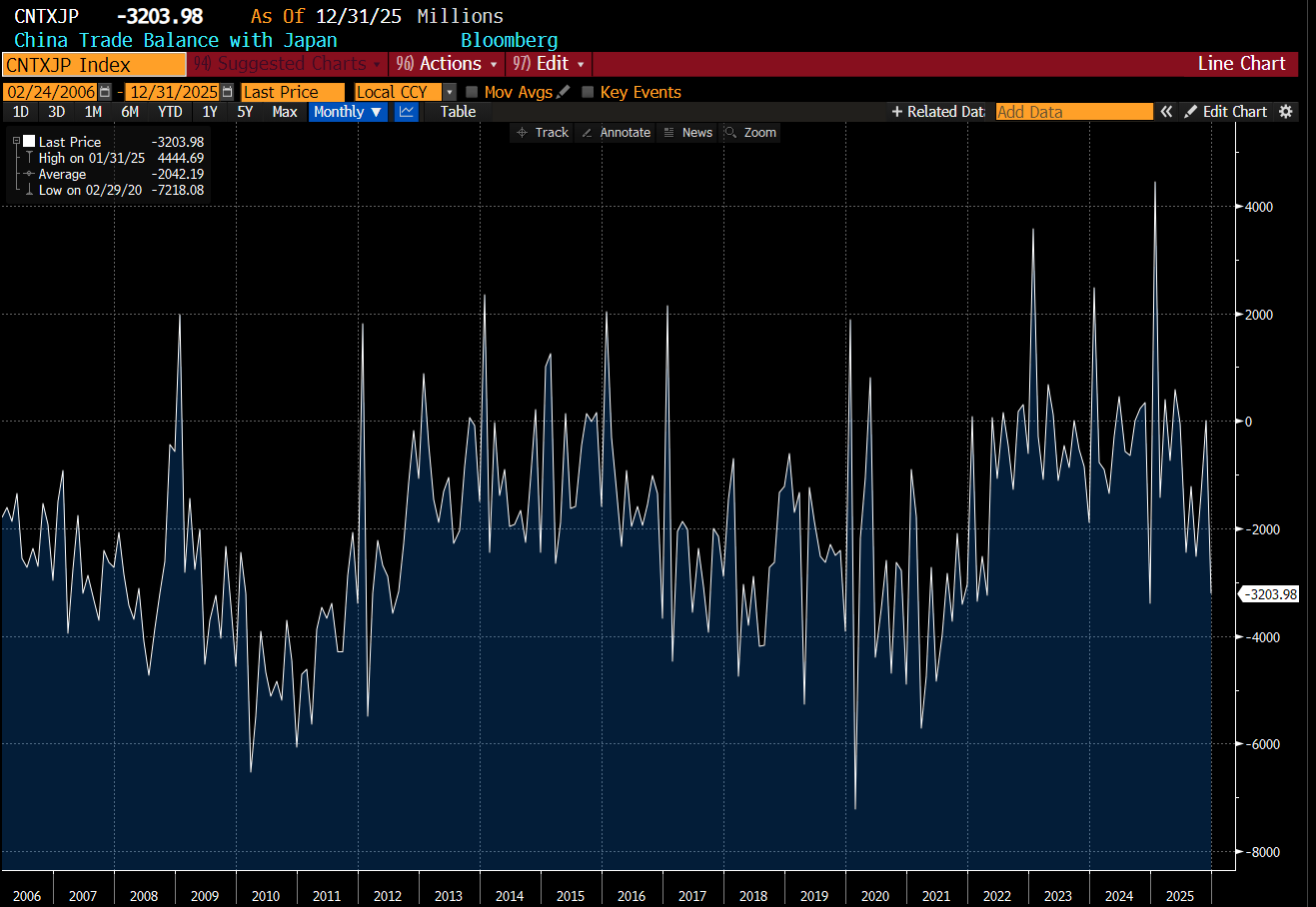

By comparison, China runs a trade deficit with Japan.

But the JPYCNY cross rate is at 30 year lows. That is CNY is strong.

To my mind, China might be buying treasuries to offset retail and corporate buying of Chinese Yuan. But this is in part driven by the much bigger macro mystery - why are other Asian currencies so weak? Yen has been weak, but so has Korean Won even as Korean exports of semiconductors surge.

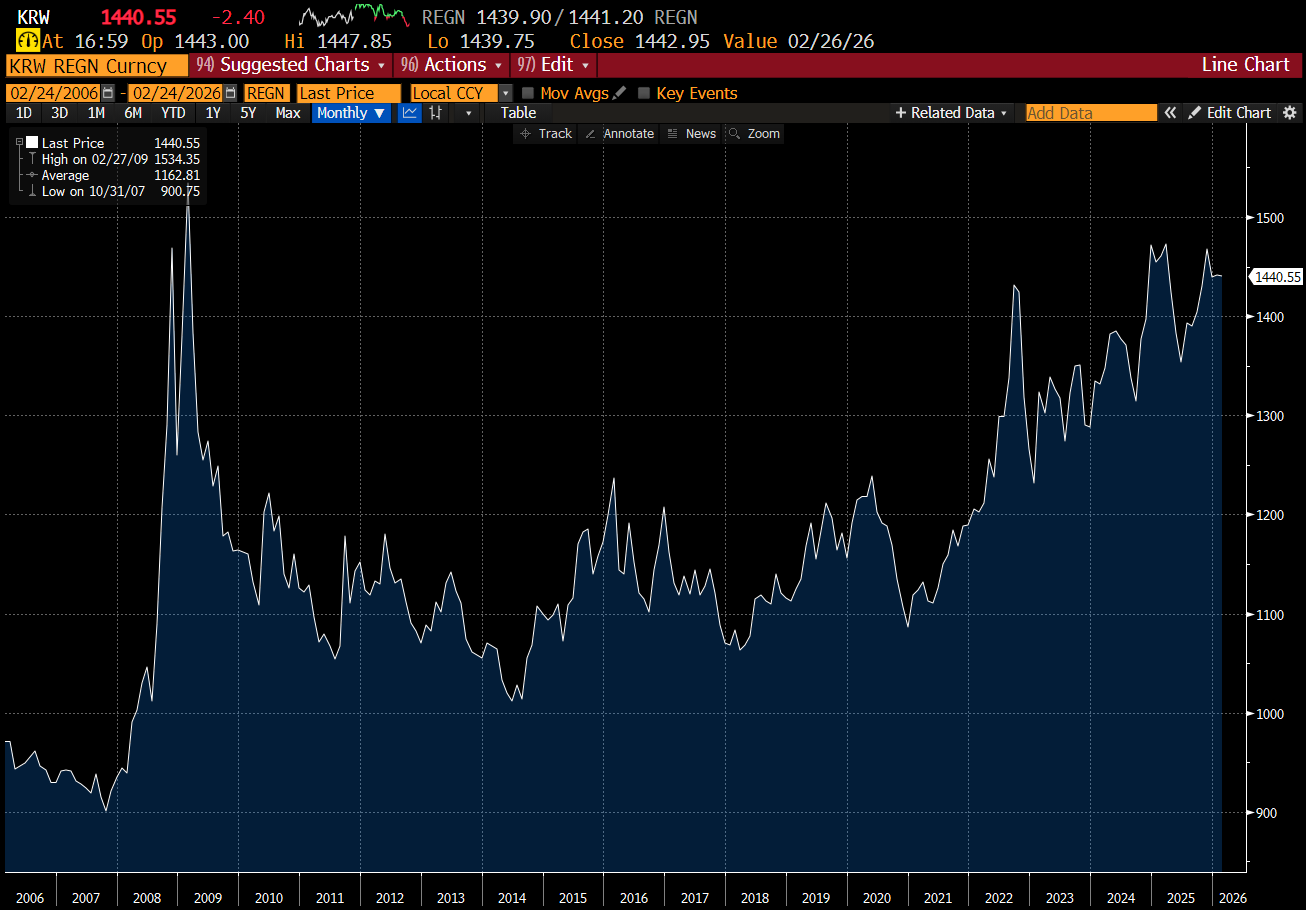

For me, the Chinese numbers I understand. And the Renminbi is strong in an Asian context. But why is the Korean Won or Japanese Yen not stronger? Korean official holdings of treasuries are at new high.

What I think is happening is that big nations of the world - US, Europe and China have turned pro-labour. Which means they want a strong currency. But Korea and Japan, remain pro-capital, which means they want a weak currency. Both have surging stock markets as well. If Japan and Korea ran pro-labour policies, I am sure their currencies and the Renminbi would be stronger too. To my mind, Chinese government has not changed policy - they do not want treasuries - but with such a huge trade surplus, when the Renminbi does appreciate it forces treasury buying by the banks to offset retail flow. The more interesting feature will be when Japan and Korea get serious about raising real wages. Then I think the real fireworks in the Treasury market will begin.