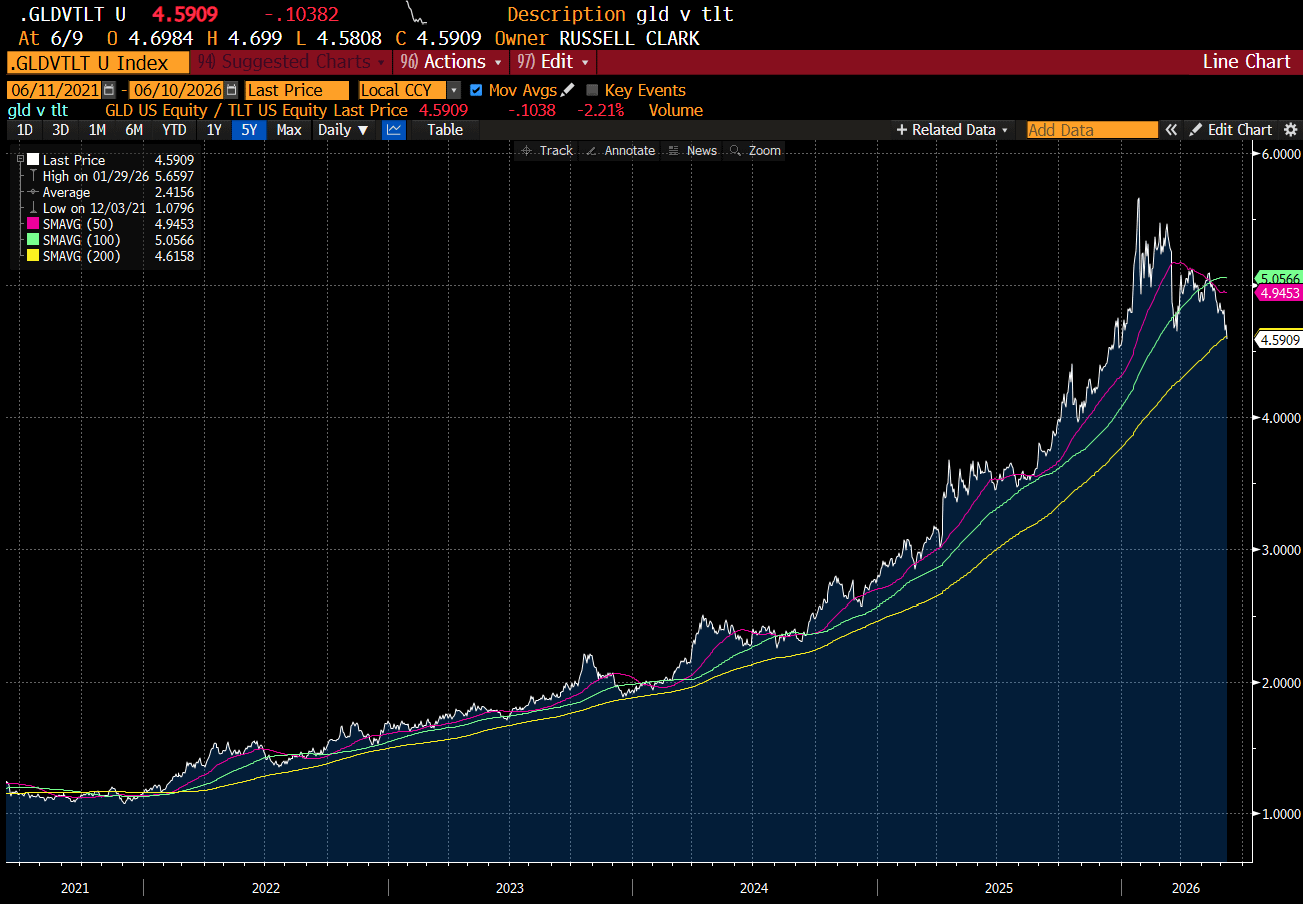

I have like gold as part of GLD/TLT trade for a long time, and it has been a great trade - but last few months it has been very lacklustre. It has traded right back and now through its 200MDA, which might mean its time to add, or its breaking down. What follows is a stream of consciousness analysis…..

The truth of the matter is that all the price action has been in the gold part of the trade. I think the market got VERY excited about gold when it started to outperform S&P 500. This meant you could be BEARISH (owning gold), and outperform the S&P 500. Sadly, this trade, GLD/SPX, has smashed through the 200MDA to the downside, and as of today has created what “technical analysts” call a dark cross. That is the market is saying you should sell gold to buy SPX.

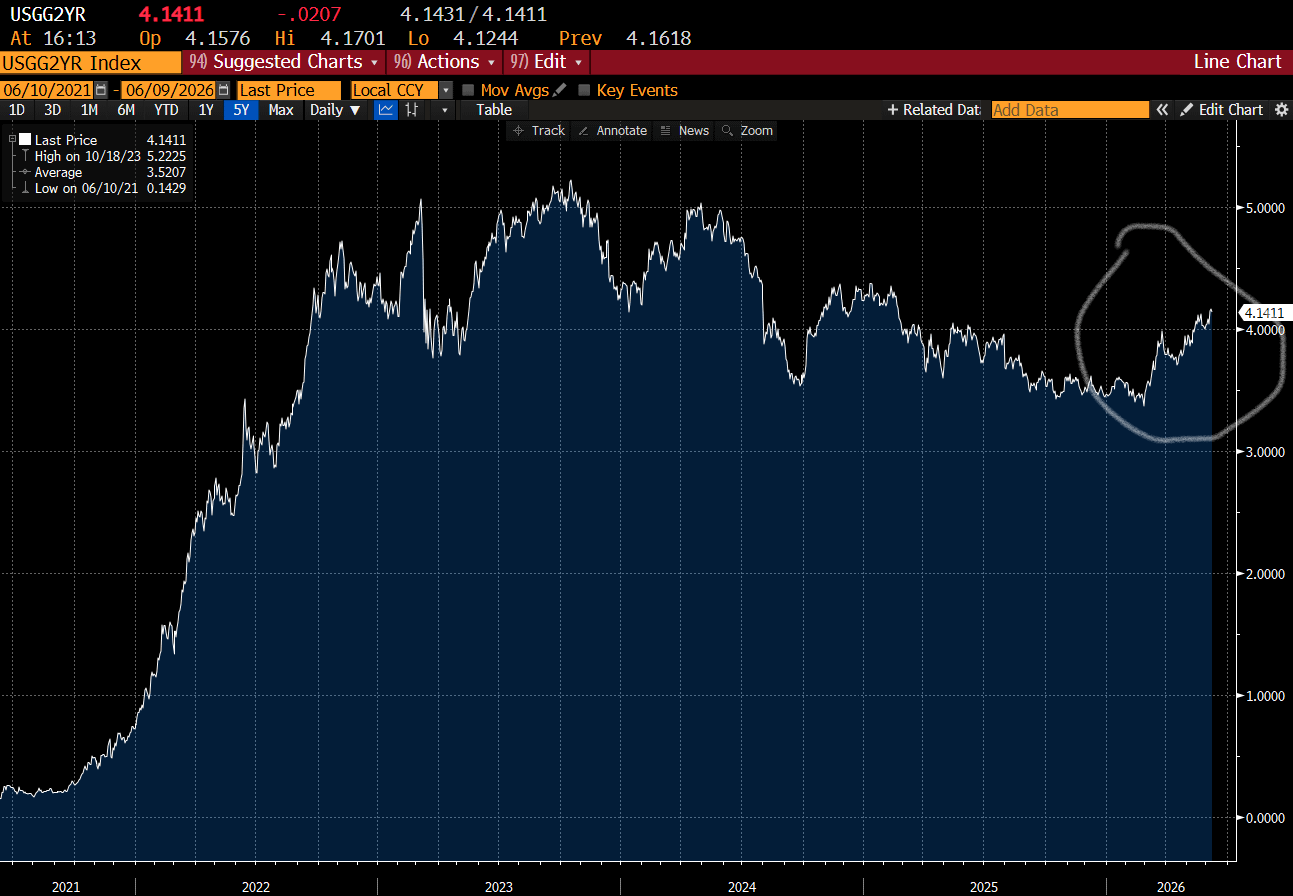

What’s the problem with gold? In the last few months, and contrary to market expectations earlier this year, markets have started to price in the Federal Reserve ACTUALLY doing its job.

Gold has been far more sensitive to central banks tightening than the long end of the bond market or equities.

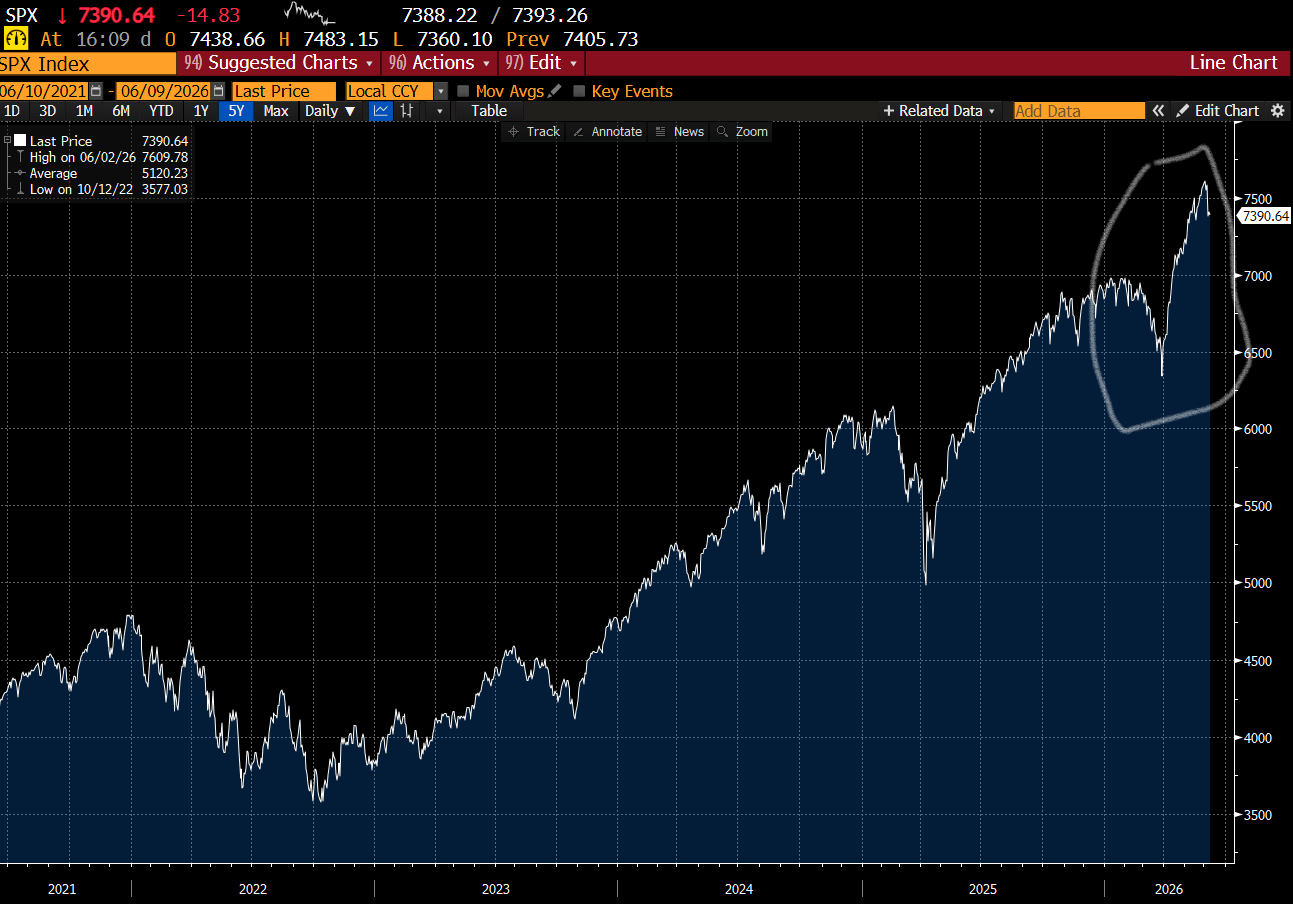

Equities have not being bothered by rising bond yields at all. That is financial assets have been very resistant to rising yields.

I guess another way to put even when bonds have a higher yields, investors still prefer equities.

So the problem with gold, is that it has reacted EXACTLY as you would expect to higher bond yields, but equities and long dated bonds (or financial assets) have not. To be fair, some financial assets such at Bitcoin and Private Equity have been weak, but broader indices have been fine.

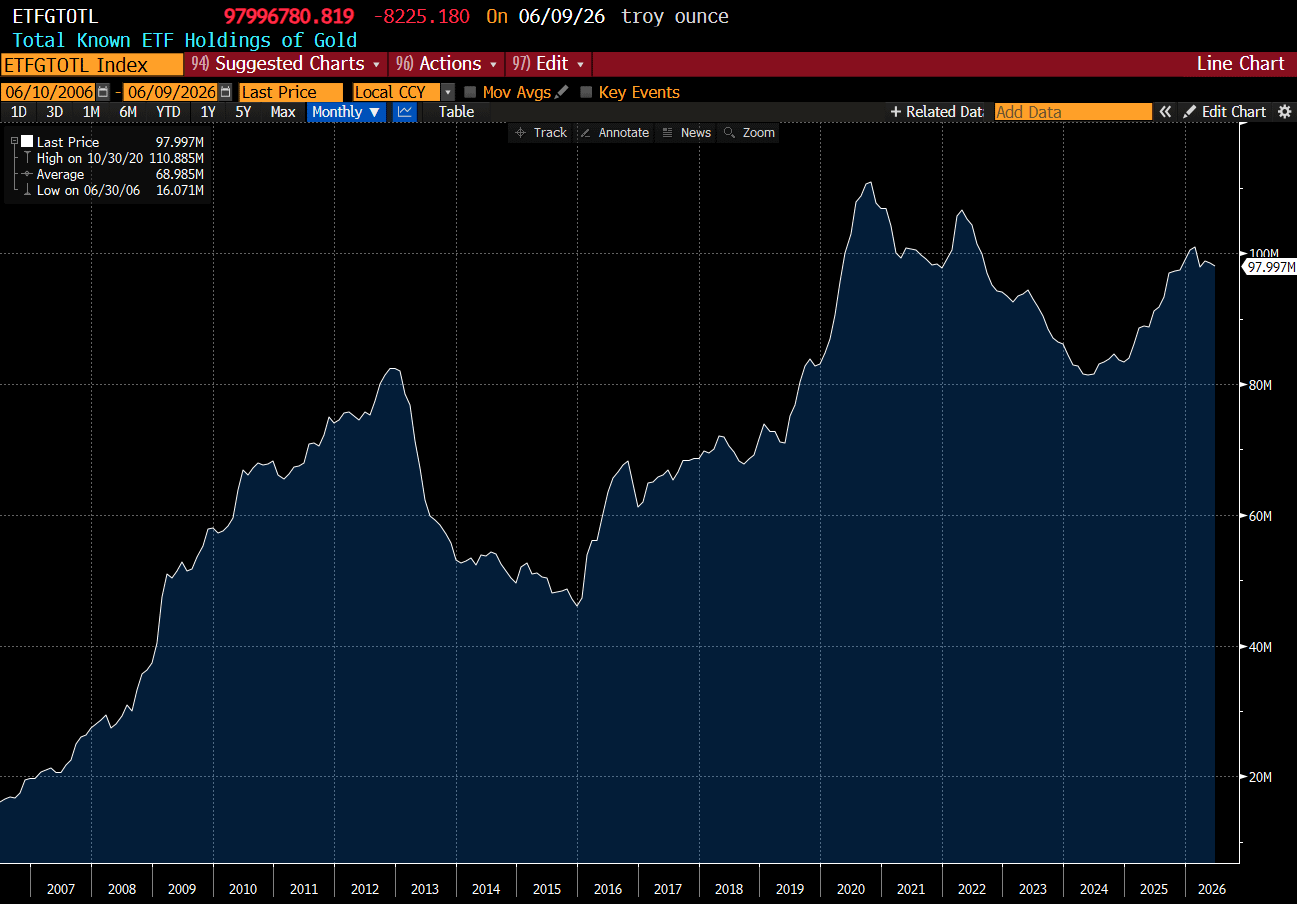

While I had a good fundamental reason for buying gold - mainly on central banks getting out of treasuries - I did worry about speculative excess. There was only limited signs of excess in gold. Back in 2012, we had seen ETF holdings of gold rise from 20m troy ounces to 80m, and in the 2016 run up it went from 50m ounces to 111m ounces. Both marked tops. So far we have seen a run up from 80m to 98m troy ounces. This was not screaming speculative excess to me.

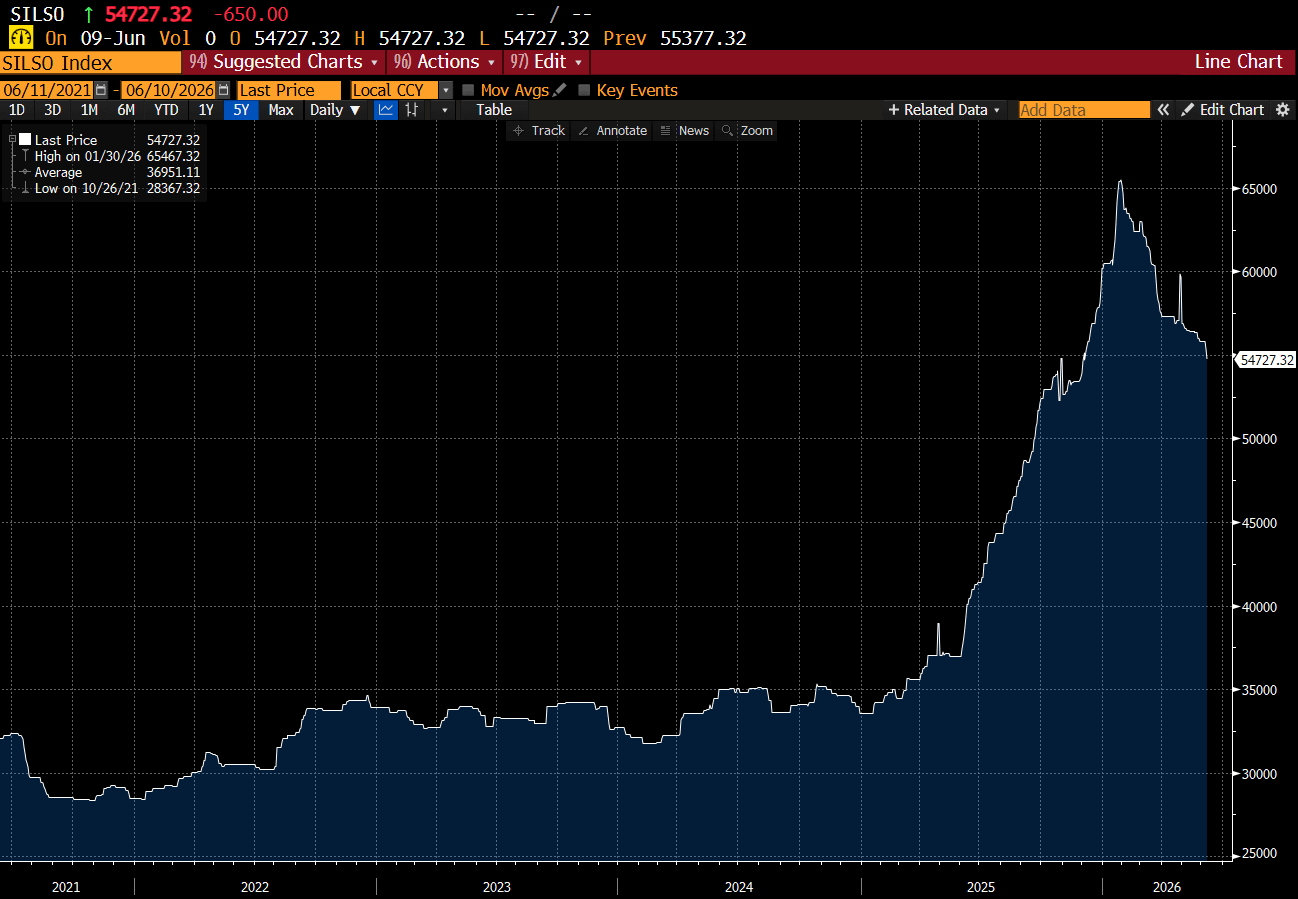

On the other hand, silver did take on a speculative nature in late 2025 and early 2026.

Looking at flows into a silver mining ETF (SIL US), it definitely became excessive - but has seen some meaningful outflows recently

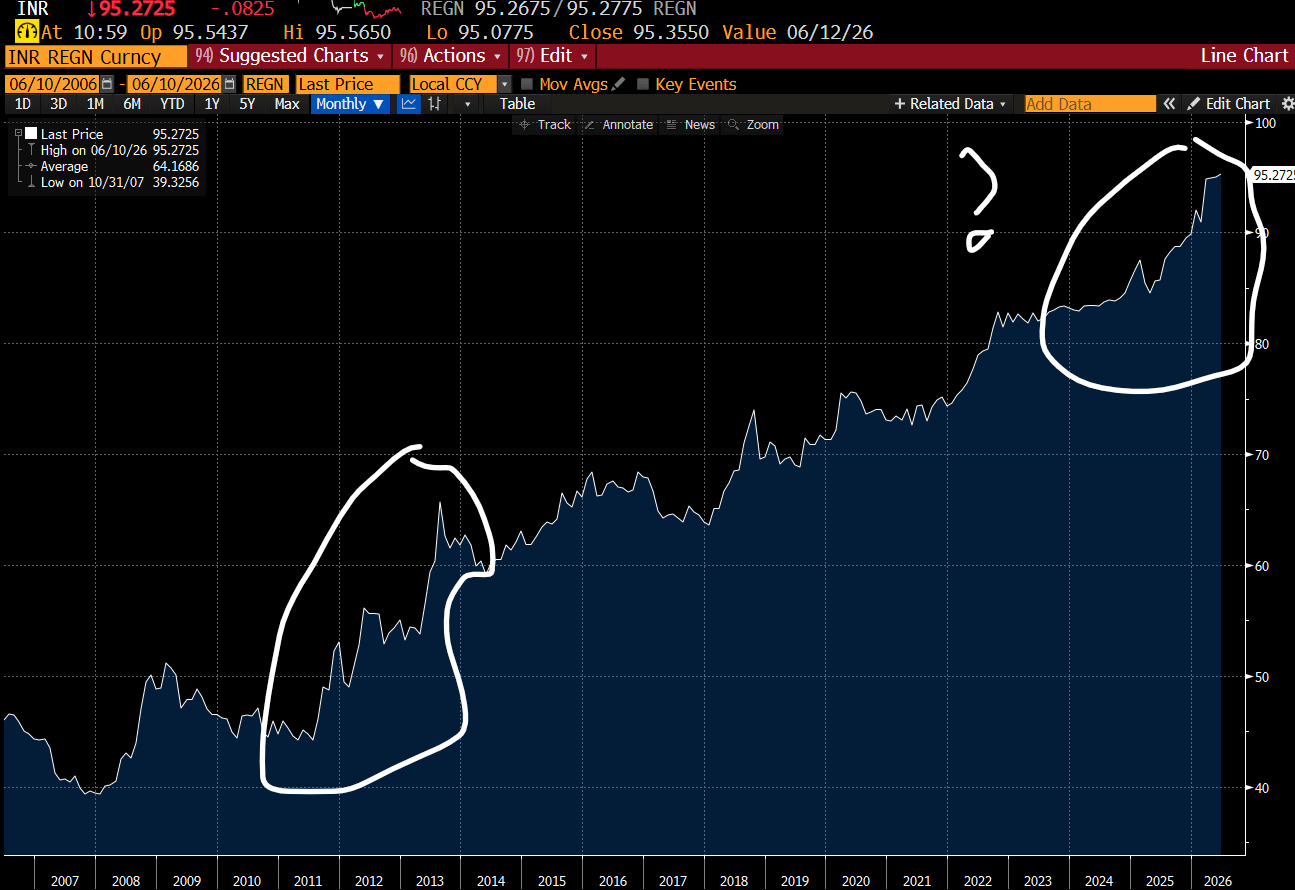

Unlike most people, I have been bullish and bearish on gold in different parts of my career (my experience is that people choose to be either bullish or bearish gold, and then never change their views). Back in 2012, I was bearish on gold, as I saw Indian Rupee weakness and broad based US dollar strength being bad for gold. Indian are big buyers of gold. However in this market, gold has moved independently of the Indian Rupee.

I had assumed that the most recent bull market in gold has been driven by central bank buying out of China and Eastern Europe. I have no reason to believe that this buying has ended. China still has an annual USD 1 trillion trade surplus that needs to be deployed somewhere, and it is not going to be US treasuries. And here we get to the crux of the problem. Do I believe that the US is about to undergo fiscal austerity? No. Do I think that Donald Trump won’t try and influence monetary policy again? No. These are bullish for gold.

The real problem is whether I think AI trades makes a better hedge than gold on monetary craziness? Now we get to the crux of the problem. In the 1970s, oil and gold was the best hedge on monetary craziness. Are semiconductors a better hedge these days? Is this was SPX/GLD already saying? If the 1970s was about cars and oil, maybe the 2020s are about compute and semiconductors? If we do Philadelphia Semiconductor Index (SOX) v gold chart, then we get a very interesting chart indeed.

What I love about this chart is that it did pick up the when you should have flipped from gold to semis in 2012, and it does give exactly the mixed vibes on gold versus equities that existed for the last few years. And it does pick up the very toppy vibe in semis that exists today. But also suggests that the craziness might not yet be done. But the story seems clear - hyper competition is driving a capex frenzy, that will end in a bust. At that time, a US fiscal deficit of over 10% will likely drive a weaker dollar, higher gold and probably a weaker long end of the treasury market. Just not yet, or that is, the gold trade is still early.