There are many reasons I like gold - but I am not a gold bug. To me its just an asset choice among many. One thing that definitely disturbs me about gold is that it has become very popular among retail investors and second rate macro analysts. I also find the recent popularity of silver also a big warning sign. Below is a graph of silver.

The tops in silver in 1980, 2008 and 2011 were also tops in the gold market. It has just been that gold has been much better than silver.

I liked gold, because I thought it would do well if the Federal Reserve was too dovish. The US 2 Year Treasury is a good measure of “dovishness” - it has recently spiked - so not oil that is pulling down gold, but changing market views on Fed dovishness.

Looking at the US 2 year - there was a brief spike in the 2 year in 2024. Was gold weak then? Less weak - but stagnant. The biggest drawdown you had to wear was 6%.

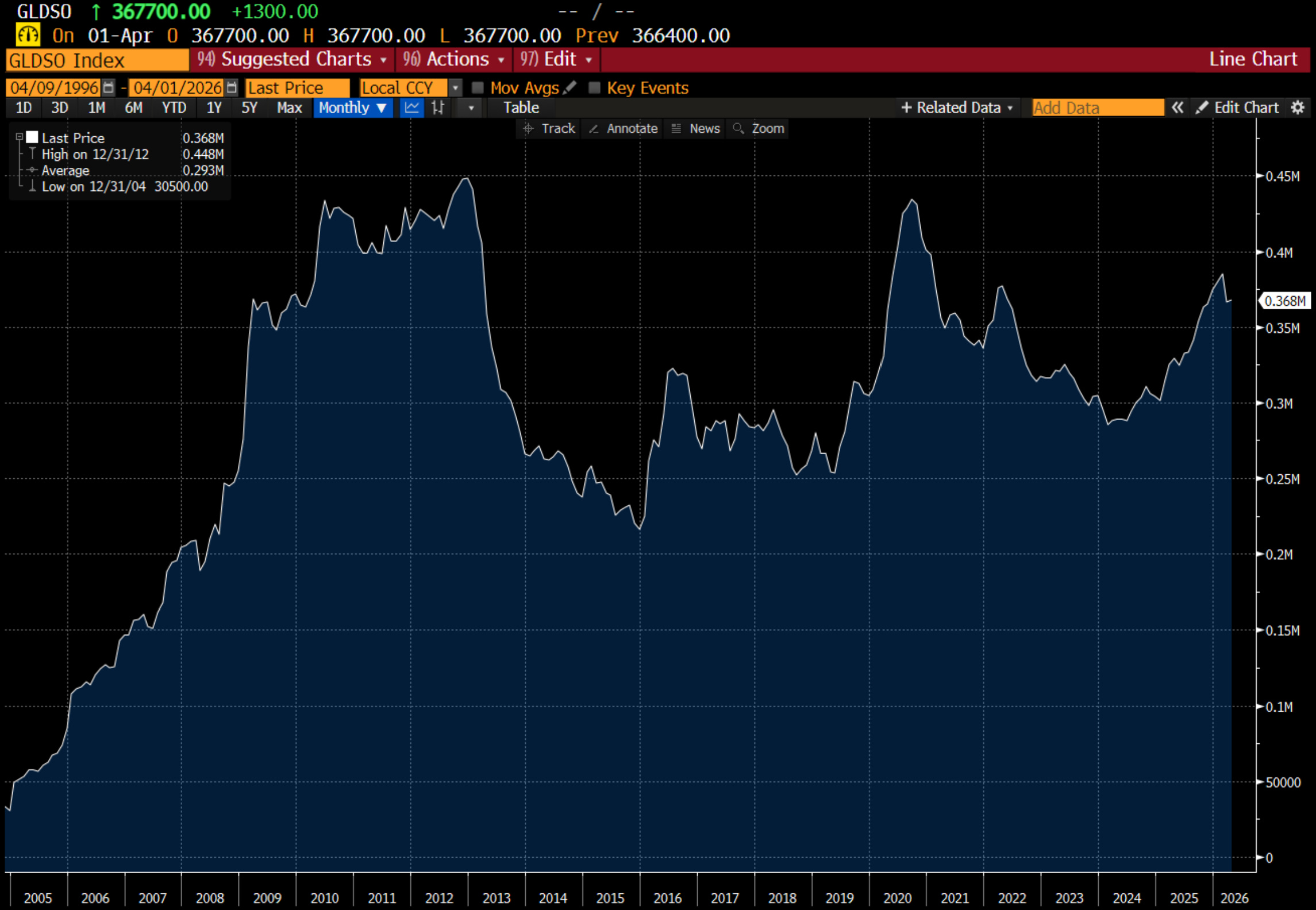

Obviously gold has become much more sensitive to changing views on interest rates. Also back in 2024, interest in gold was much less, which we can see from shares outstanding in GLD. In 2024 it was at a low, but today it has risen, but not that much.

So is gold going to get the Bitcoin treatment? Bitcoin since peaking at USD125,000 USD has dropped back to USD67,000.

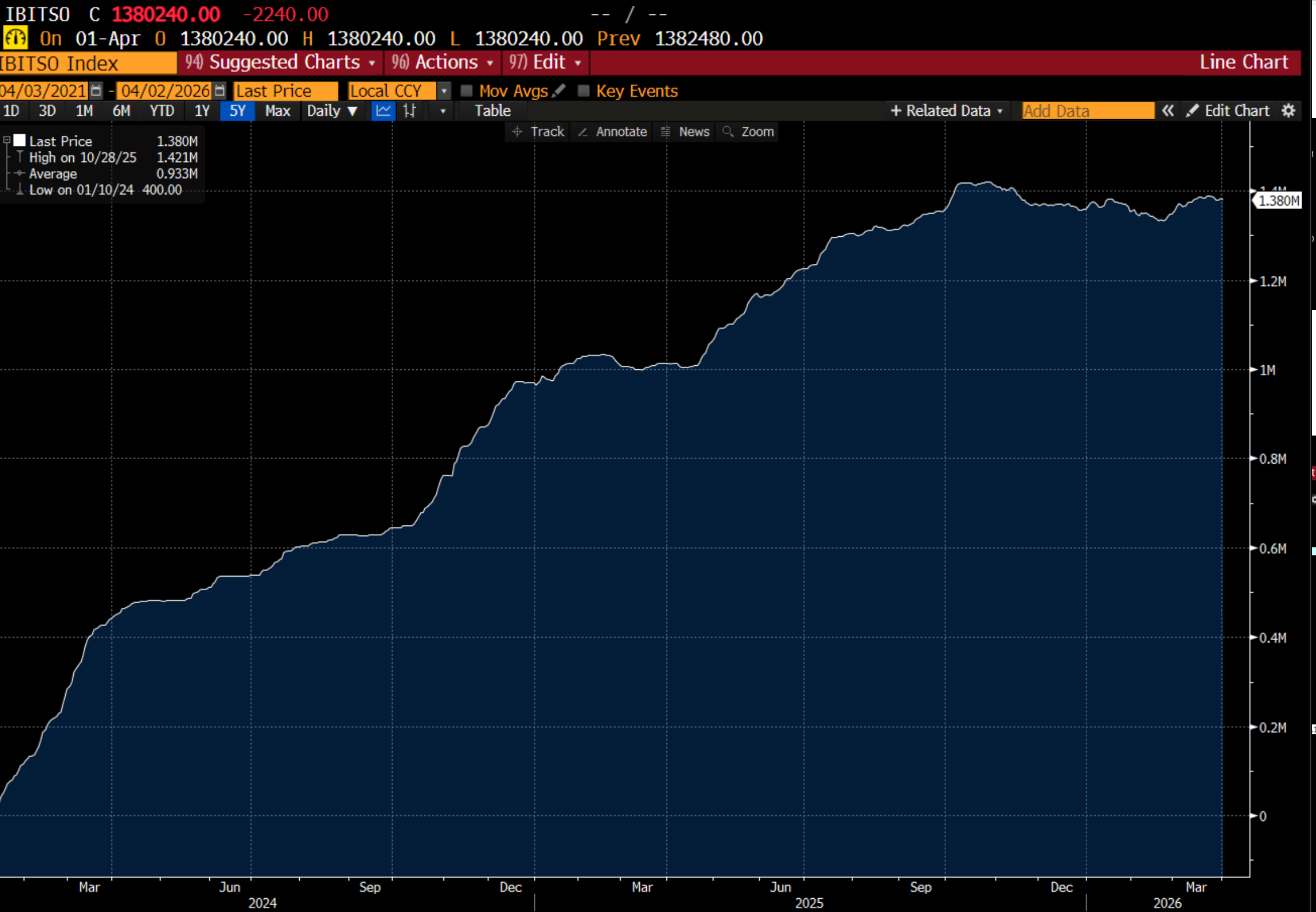

The most bearish signal I found on Bitcoin was surging shares outstanding in IBIT US - which have yet to fall. That is investors remain committed to bitcoin despite the fall. This is never a good sign. Bear markets tend to end when everyone has given up.

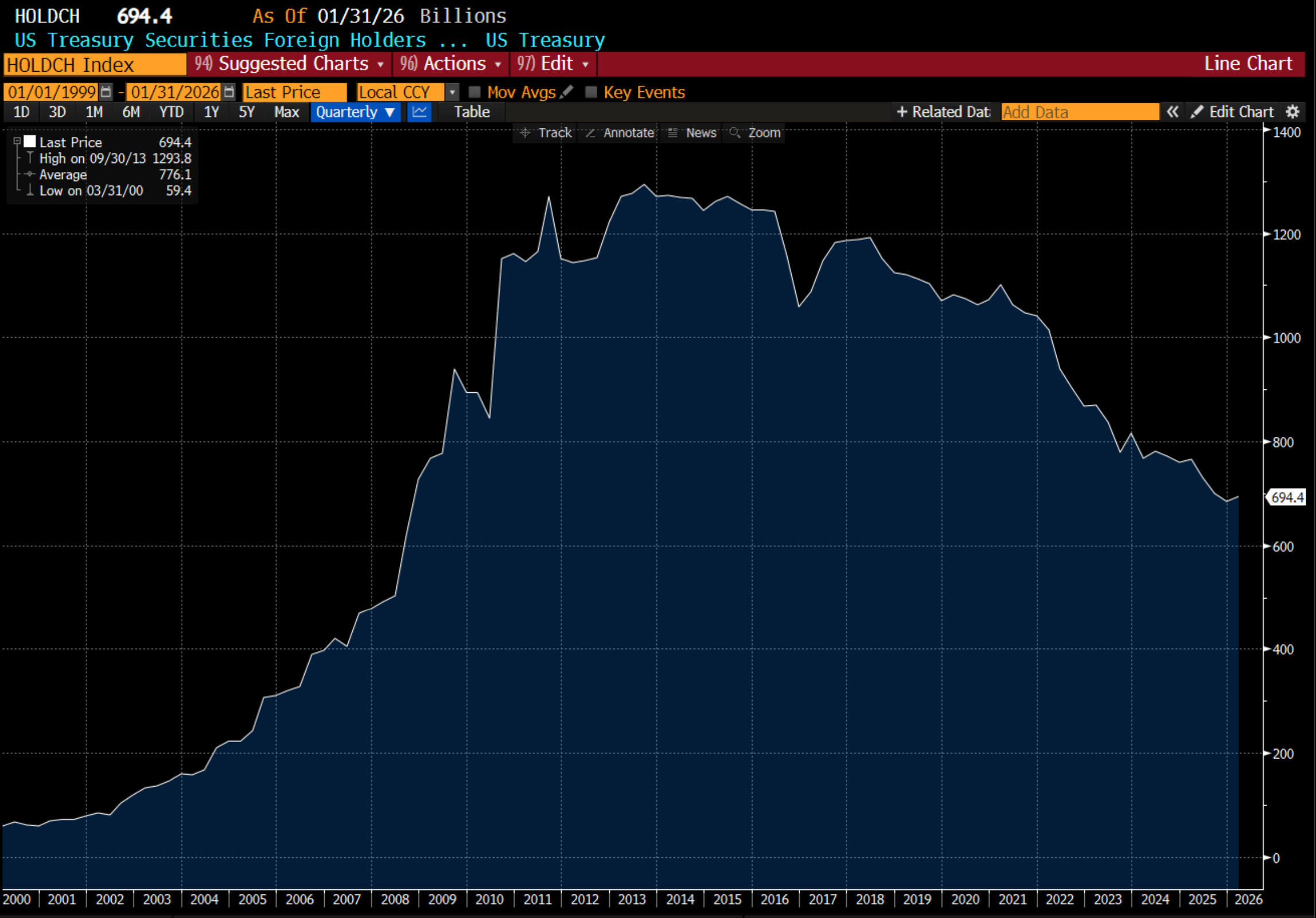

One reason I preferred gold over Bitcoin, sliver, copper or any other physical material was that there seemed to me a committed buyer - namely central banks. If China is running a USD 1 trillion trade surplus, but also does not want to buy treasuries - which is what official holdings data shows, then the only option is gold. (Brad Setser argues Chinese commercial banks are now holding treasuries instead - which may well be true - but does not affect the argument for gold).

There are other central banks, and much has been made of Turkey lending out gold to prop up its currency - but China is really the big daddy here. If China had felt it had enough gold, and it stopped buying, then we would really have a bear market in my view. How likely is this? Official Reserves of gold in China are about 2,300 tonnes - which is about USD 350bn at todays valuation. US official reserves are closed to 8,000 tonnes - which I think it a reasonable target for China. Assuming some undercounting by the Chinese, and lets say they are at 4,000 tonnes, this still leaves some 4,000 tonnes to buy, leave USD 650bn of buying. This is greater than current ETF holdings of gold, and this also ignores other nations potential diversification away from Treasuries into gold.

Ultimately the problem with gold is that is has been a great trade, and it has run ahead of other assets. I like gold on a “relative” basis. Gold versus TLT has been great, but it is still a long way from its 200 day average.

I also prefer gold to S&P 500. But has the same problem - its a long way from its 200 MDA.

Lets assume I am mindless technical analyst - and we assume TLT and SPX do not move, how much could gold fall? Gold could fall 10 to 15% and still be in relative bull trends. I am of course bearish on both the S&P 500 and TLT - so we could get another March, where gold falls more than TLT and SPX - which could mean golds fall more like 20%. That type of thinking then puts gold at USD 3,800. If TLT and SPX falls further, gold could also fall further. All of this implies I should probably just go massively short the market. And there is a time when I would have done exactly that - but as you, I and everyone else knows, President Trump has a habit of managing to markets. When I think about an investment strategy - it has to past the “sleep test”. The sleep test is basically can I run that strategy and still sleep at night. The corollary of this is that if I am not sleeping at night, I need to cut risk. Naked short does not pass the sleep test.

What would the above thinking mean for silver? Well lets say gold falls 20%, and silver correct back to a ratio of 80/1 that has be the average of the last few years (it is at 65 now) - then that would imply a silver price of USD 48/oz, basically putting it back to the price in November. This feels relatively likely to me - mainly judging by the “quality” of the silver bulls. I am tempted to short silver miners like WPM US and PAAS US - I suspect it would be a lot of fun, as they are widely held names these days. But I also know I would have no holding power in these shorts - that is if they rallied I would probably cover. To really have conviction on shorts like this, I would need to have clarity on the War in Iran, and on a much more hawkish Fed - which I do not. These are both Trump trades now.

Ultimately, what I am think I am saying, is that we could finally be in the bear market that I have wanted for a long time. In this bear market, I expect the S&P 500 and Treasuries to decline, and gold to decline “LESS” than these assets. My worry, is that in the short term gold MIGHT fall more that treasuries and the S&P 500, but I think it is too big “political” risk to not have gold to offset bearish positions.

To answer my original question - yes - gold could do a Bitcoin. But if gold is doing a Bitcoin - then other assets will likely be doing much worse! And ultimately, I think the Chinese will be buyers of gold, even if it is a bit lower than where we are today. Bitcoin (and silver) does not have that backstop.