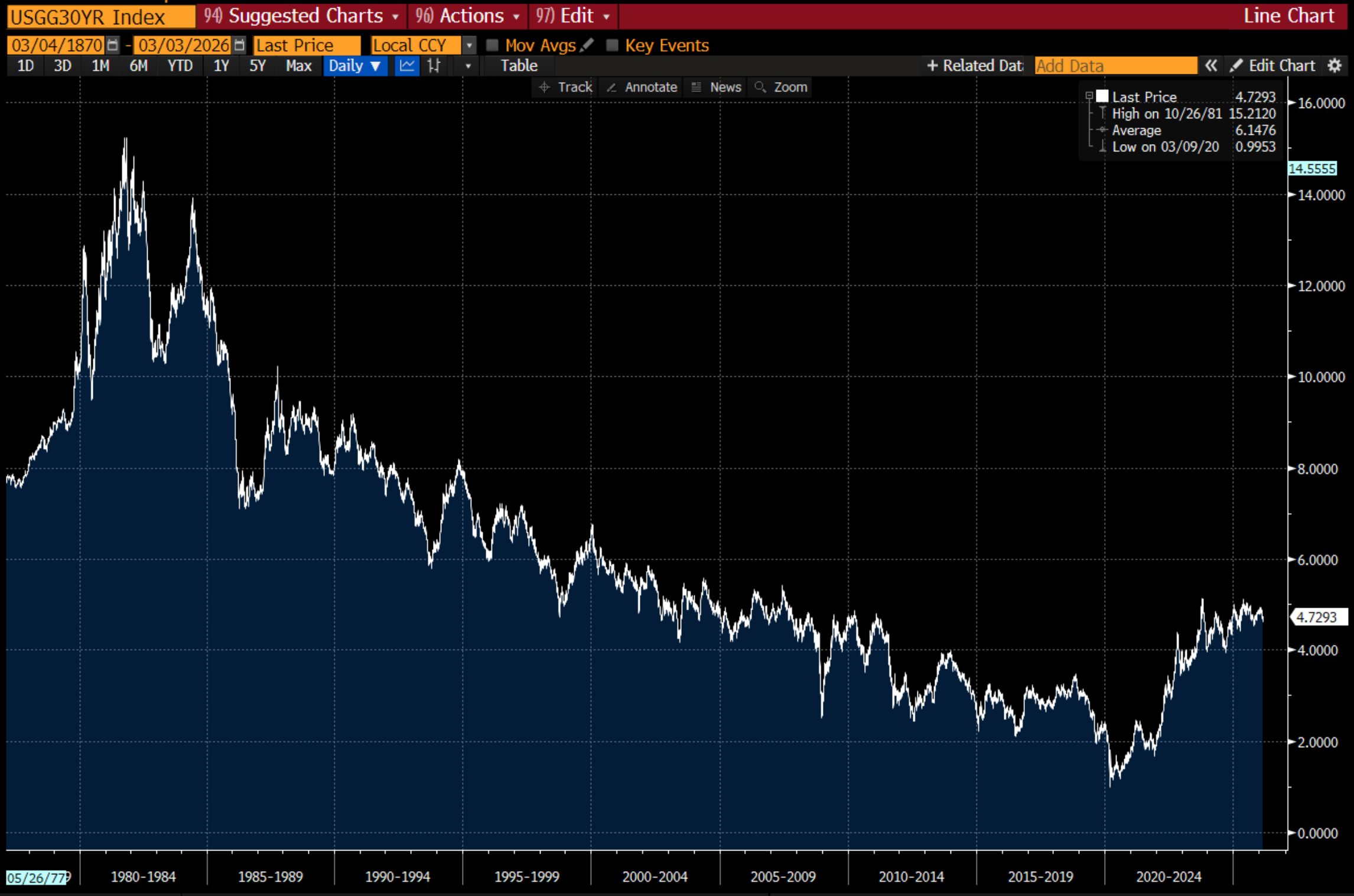

The current catalyst for a market shift is the war in Iran - and as it is a crisis, the market thinks all moves are temporary. For me, crisis tends to accelerate what the market is doing anyway. In the 40 year bull market in bonds, there were always crises, which would drive yields lower, but that was just an acceleration of what was an obvious trend. In hindsight the deflationary crises of the S&L Crisis, the Tequila Crisis, the Asian Financial Crisis, the Dot Com Bust, the GFC, the Euro Crisis, the Emerging Market Crisis, the Covid Crisis and ever falling yields were two sides of same coin. Economic crisis was welcomed (in a way) as it drove deflation and lower yields.

What I am arguing is that we now have had a political shift from pro-capital to pro-labour shift. What that means is governments intervene to make sure that employment and wages do not fall. And with the obvious increase in defence spending that is required by every government, the political motivation and physical ability is there. That is government can and probably should mop up any excess labour to build out defence and AI infrastructure. This is the new world, and what is exciting about the current “Iran Crisis” is that bond yields are rising, not falling, just as this thesis would predict.

We have now seen this new dynamic in bonds a few times. Under Prime Minister Truss in the UK, and during the Liberation Day sell off under President Trump. To me the old world of falling interest rates and deflation is dead. What is interesting, at least to me is that markets are taking their time to price in this world. Or as I explain to investors, in the old world markets constantly mispriced currency moves. In the new world, markets constantly misprice yield risk.

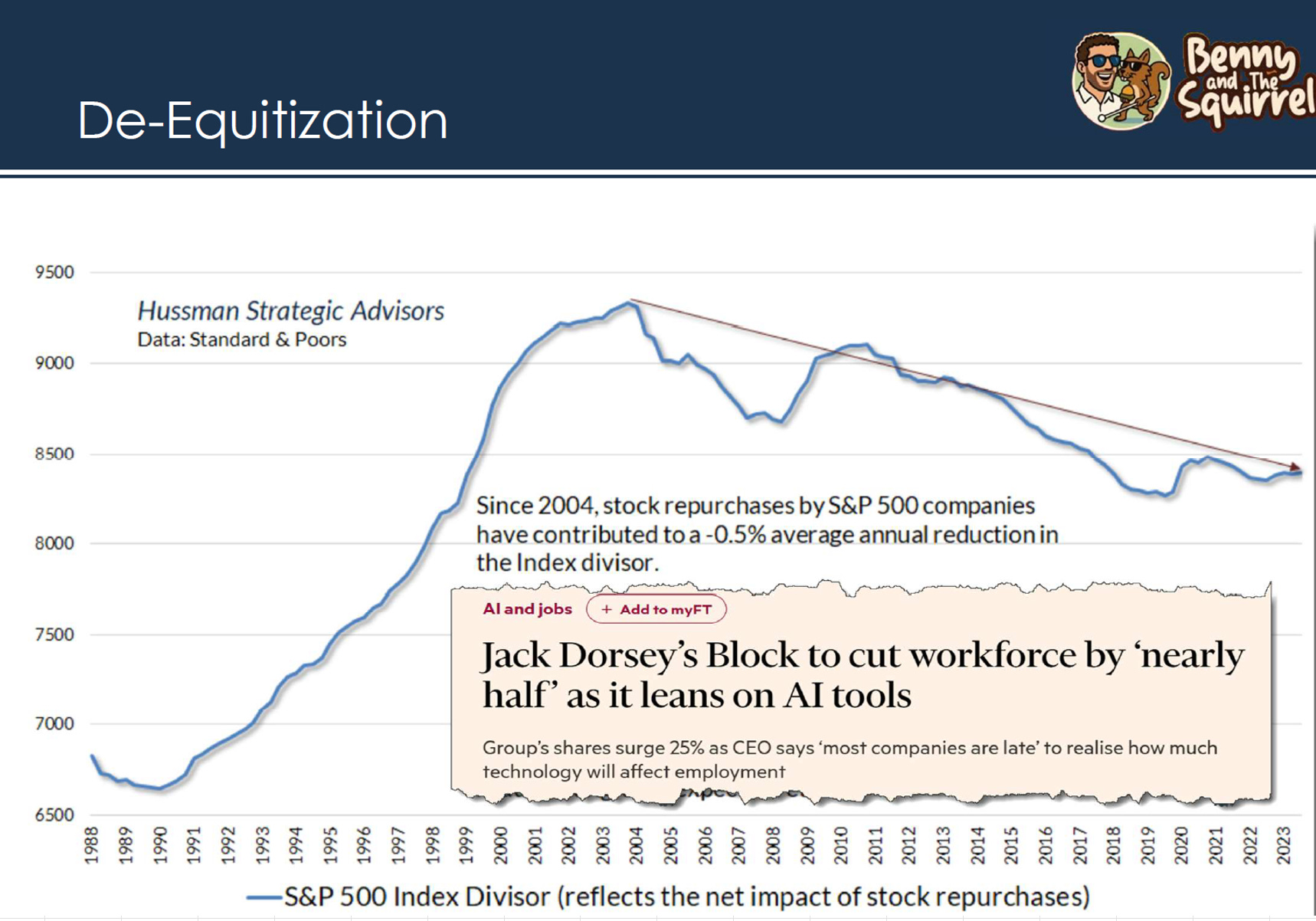

There are lots of ways to look at this shift, but one of the most profound ways is to think about where pools of capital sit. For 30 or 40 years now, big pools of capital have formed at institutions - be they endowments, retirement funds, sovereign wealth funds or corporate balance sheets. These huge pools of capital drove the cost of capital lower. Central banks acted to encourage this fall. During the worst of the Ben Bernanke led QE mania, central banks literally printed money to give to corporates. This represented the pinnacle of the idea that corporates and corporate managers are the best people to decide how money should be invested. The irony, which almost every man on the street understood, but was seemingly lost on the Central Bankers, was that corporates took all this extra money, and mainly used it for share buybacks as this was a risk free route to wealth, rather than actually risk money to invest. If you look at US durable good orders, the entire QE era was marked my minimal investment. Donald Trump may want a Nobel Peace Prize, but for me giving Ben Bernanke the Nobel Prize in Economics was a true travesty and devalued its worth forever. Not only did his economic ideas directly contribute to the GFC, his ideas led to huge growth in wealth inequality and the rise of populism. I struggle to think of greater failure in public life than Ben Bernanke. I digress. In recent years, as pro-labour policies have take over, investment has surged again, just as QE has receded. And more and more capital should be pooled at households, rather than in institutions.

So if QE did not lead to investment, what did it lead to? Well clearly it led to the “de-equitizaition” of markets. I found this good graph in a Blind Squirrel presentation, so have pilfered it (to be fair, it looks like it was pilfered from Hussman, who pilfered it from S&P. No honour among thieves!).

So with long and short book, I look for ideas that respond well to this new pro-labour world. I think I have found a couple more shorts.