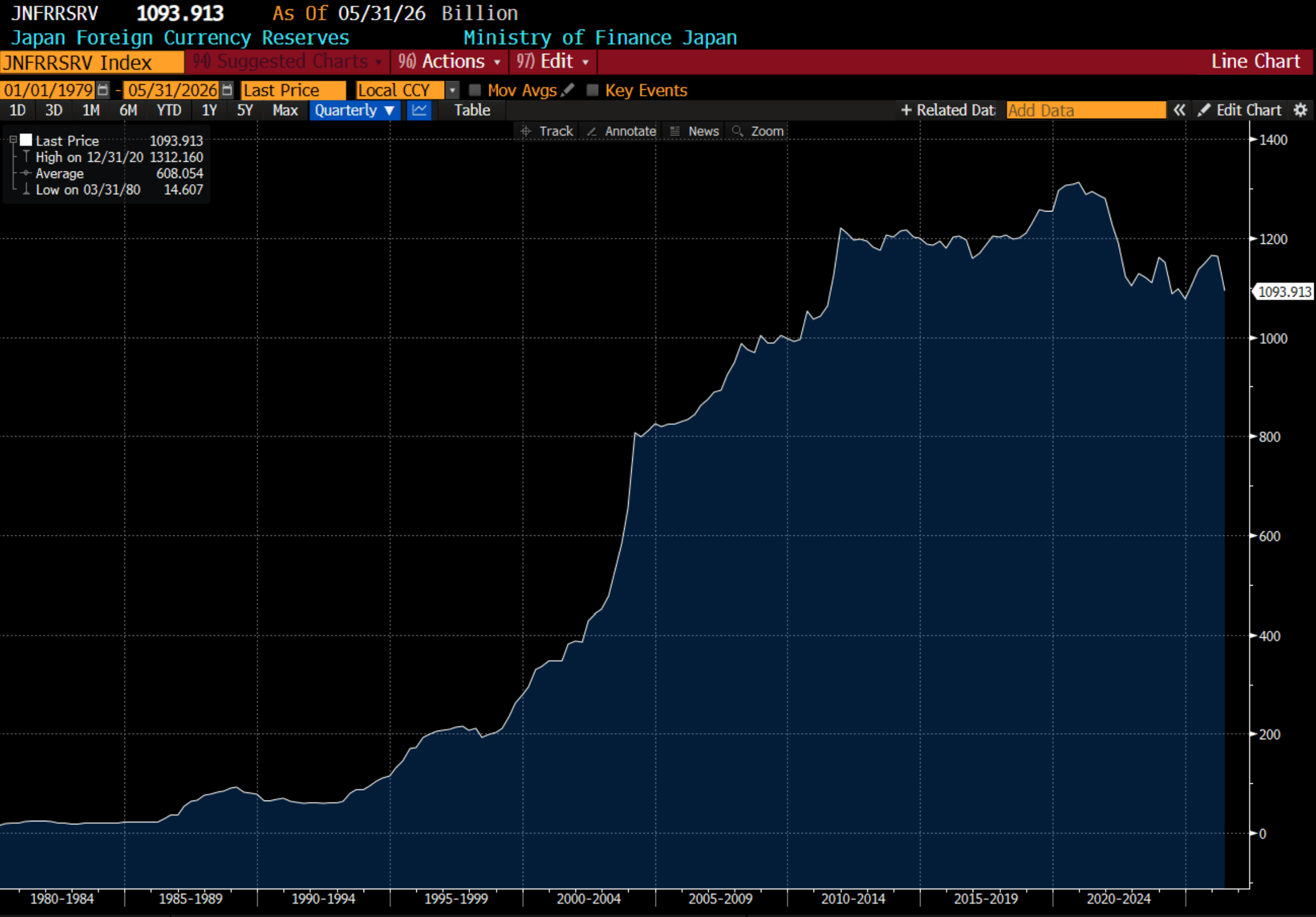

When I first starting to think about the idea of a pro-labour theory of markets, I assumed the cost of capital would rise for political reasons. The long period of "pro-capital” policy had lead to the creation of large pools of capital. The first, and most exceptional in my view were foreign reserves. The idea of buying another countries fixed income was a completely foreign idea before 1980. All foreign reserves were gold, but from 1980, led by the Japanese, buying US treasuries became accepted as a “better” form of foreign reserves.

It also happened that from 1980 to 2000 or 2015, owning treasuries was much better than owning gold, which reinforced the idea of owning bonds over gold. This has since reversed.

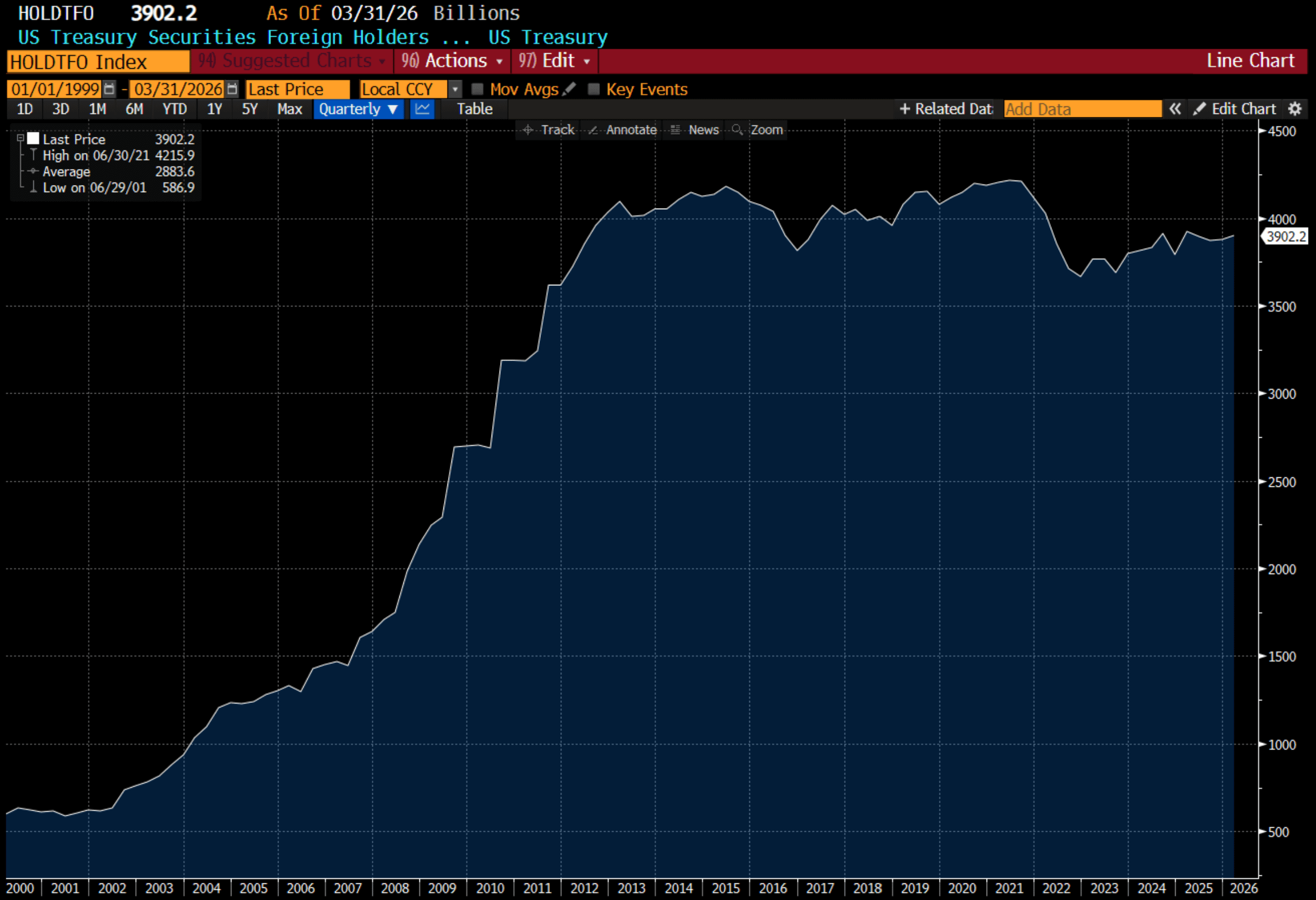

I saw buying treasuries as foreign reserves as pro-capital policy, as much of the Japanese buying of foreign reserves was meant to keep the Yen weak - that is to keep labour costs low. Competitive devaluations is most clearly a “pro-capital” policy (devaluations reduce labour costs, and boost competitiveness - which favours the owners of capital). In the new pro-labour world, I envisaged governments endeavouring to keep their currencies strong, and hence foreign reserve growth should slow or reverse. Japan shows this trend, but official holdings of treasuries have been falling for a while now. Total official foreign holdings of treasuries has been weak.

I also saw that rising interest rates should begin to kill interest in “alternative asset managers”. These businesses held huge amounts of “dry powder” - but it is hard to square this dry powder with redemptions that most of these businesses are now seeing. The performance of the Invesco Private Equity ETF confirms these problems. That is two big pools of capital - foreign reserves and private equity are already displaying signs of problems.

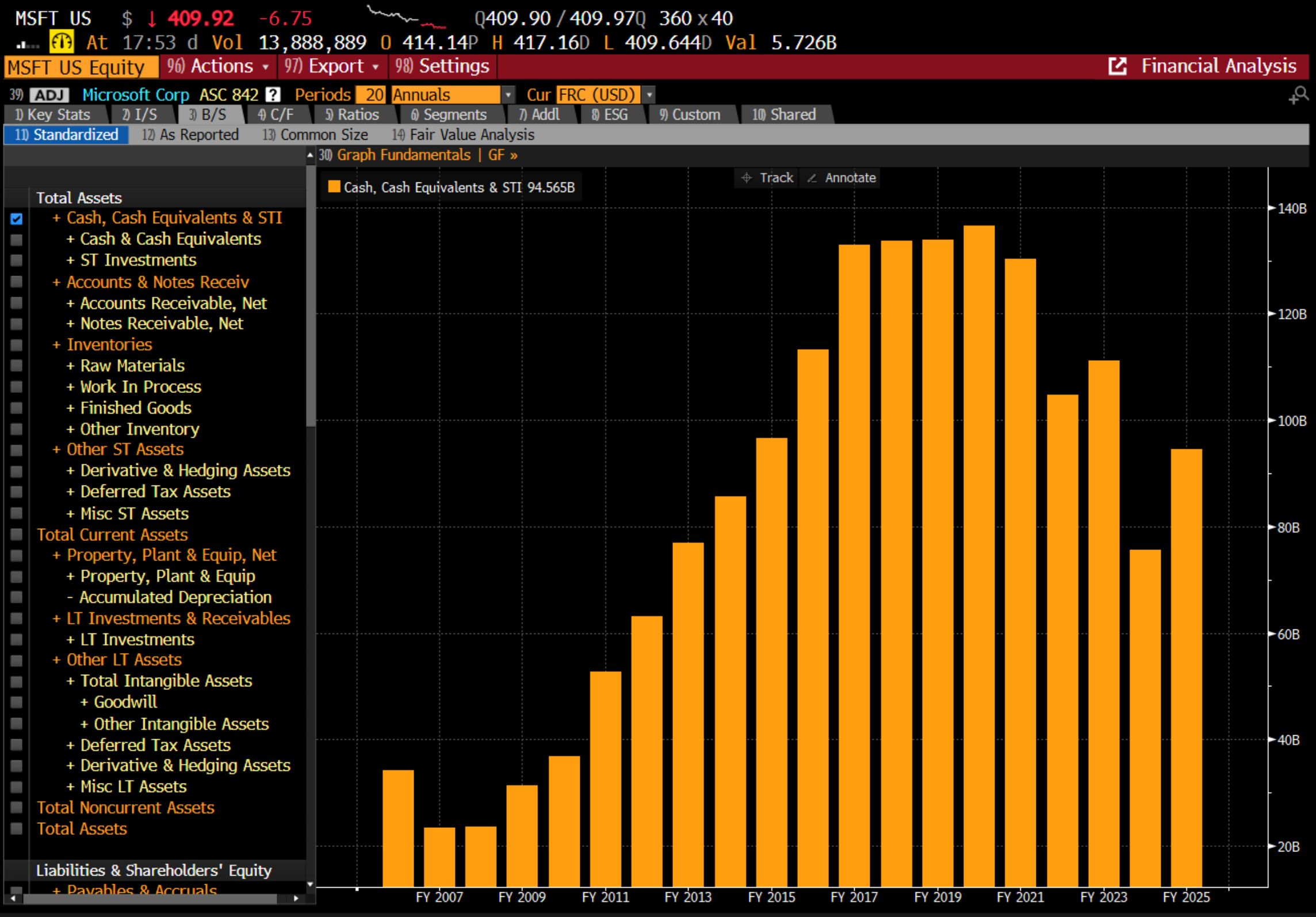

I also assumed rising wage demands would start to effect the cash piles that had grown in American corporates, the third biggest pool of capital. Microsoft for example had seen cash and equivalents go from USD 25bn in 2007 to USD 140bn in 2021. This cash pile has now fallen to USD95bn or so.

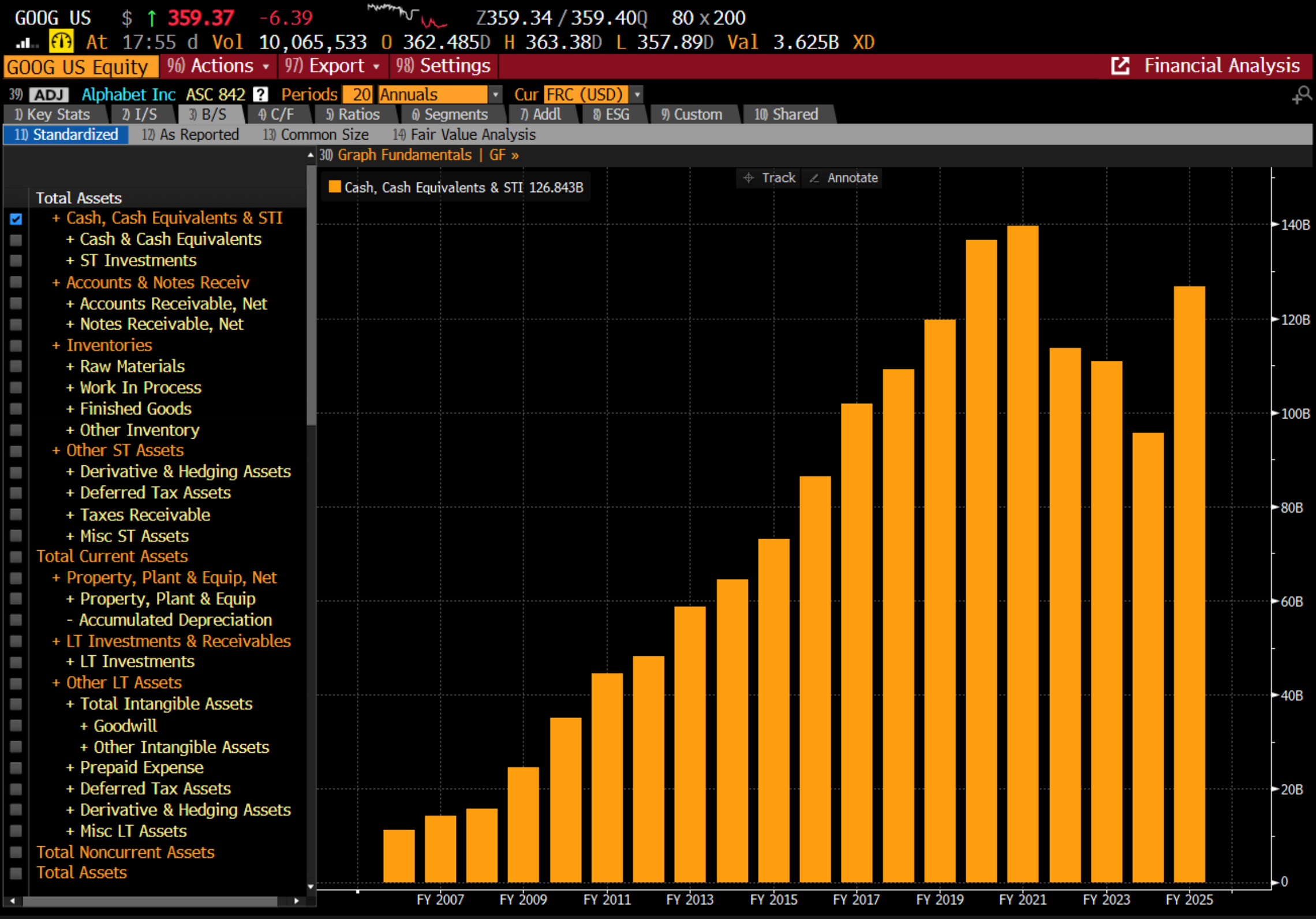

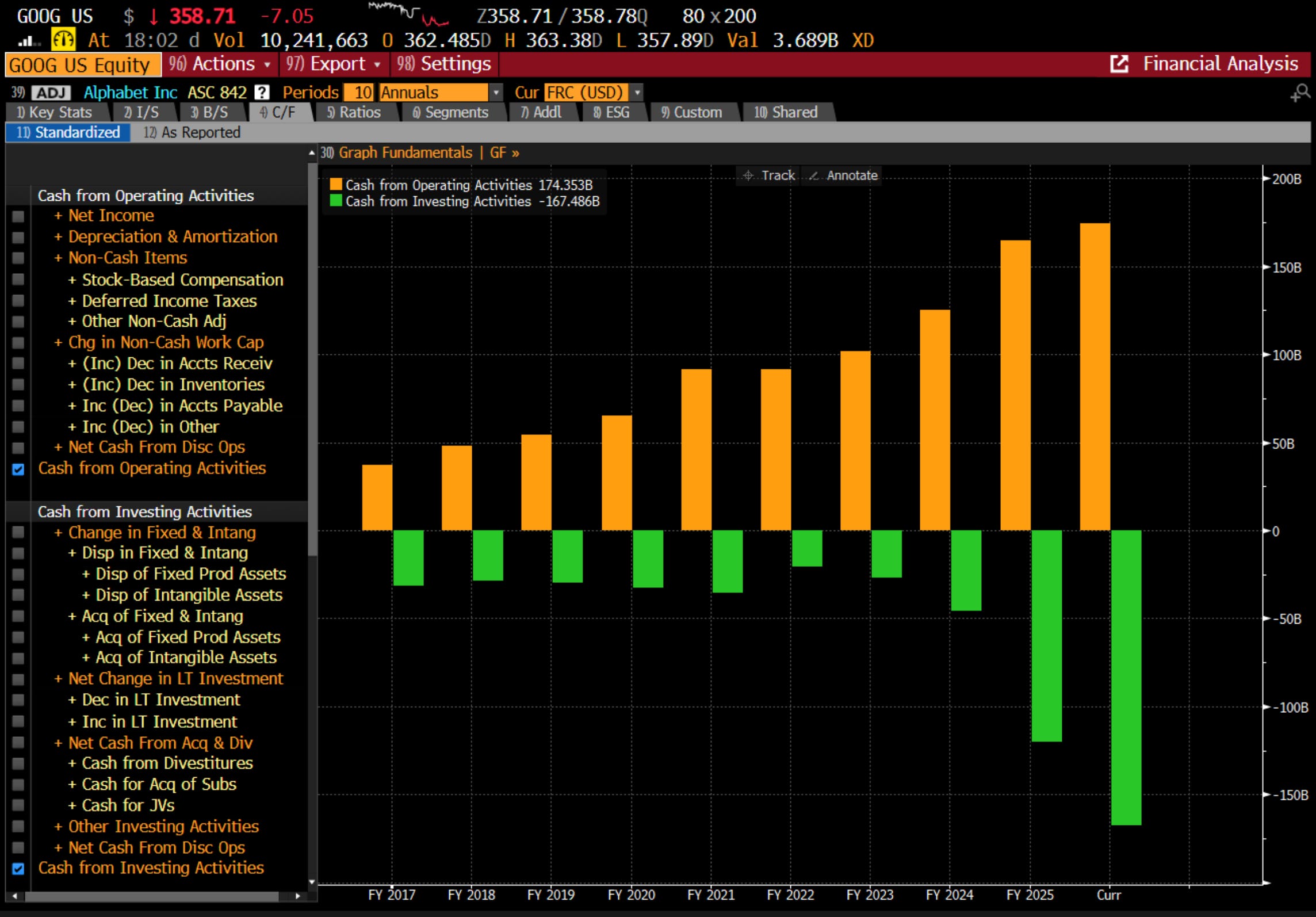

Google claims to have USD120bn of cash and equivalents, but are choosing to raise USD80bn in an equity raise.

Obviously, around USD 100bn of cash equivalents seems to be the line in the sand for Google, and they are already spending everything they make on AI. But they want to spend another USD80bn, so raising equity is the obvious answer.

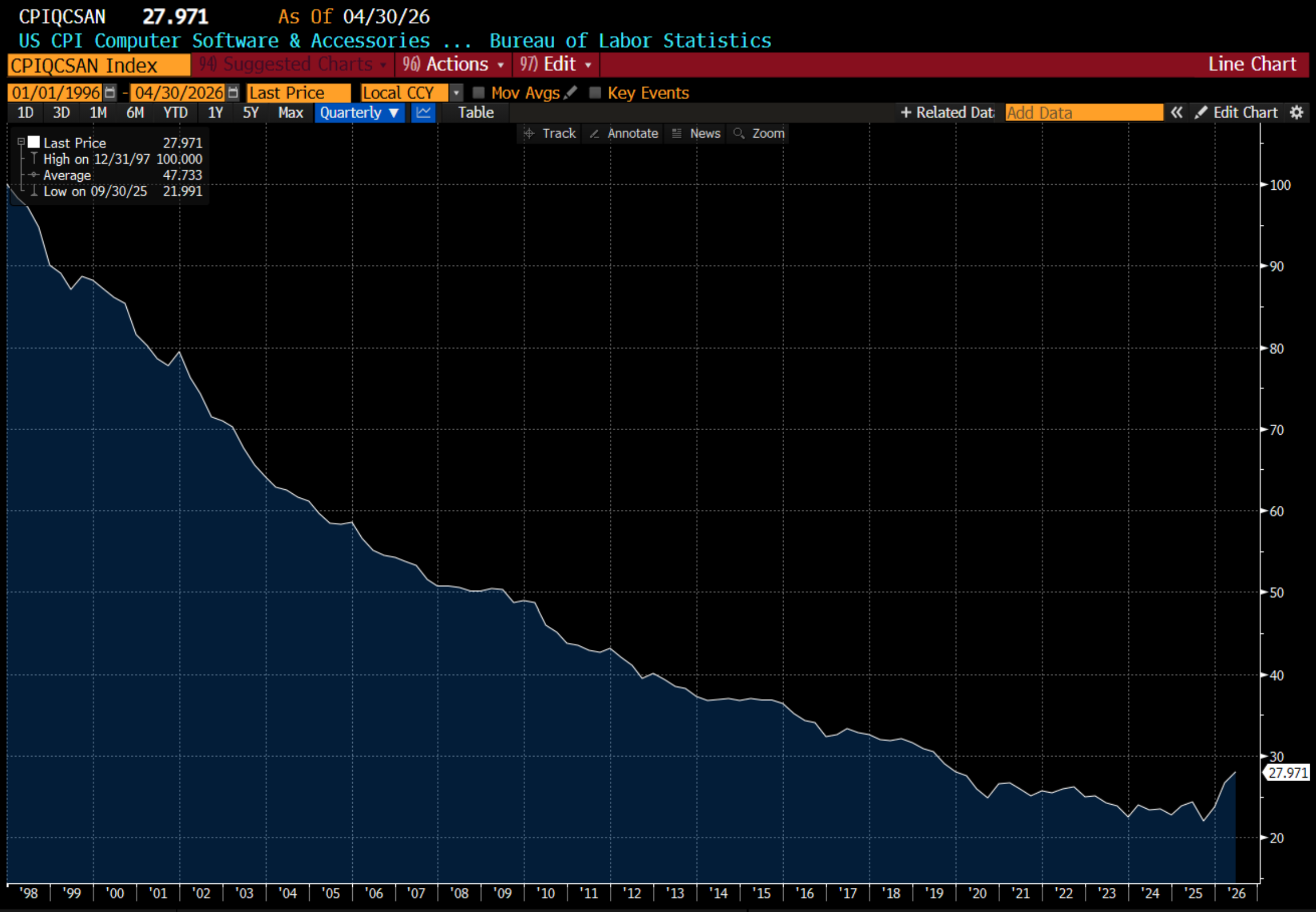

So to my surprise, rather than wages rising, it has been the price of semiconductors that have been the driver of inflation, or perhaps more correctly, the biggest beneficiary of governments working to halt recessions. For many other firms I look at rising labour costs have drawn on capital reserves, but with big tech, is is spending on semiconductors that has reduced their pool of capital.

And the AI boom has ended one of the enduring features of capitalism. Technology should make things cheaper. But technology itself is no longer becoming cheaper.

From what I can see, the rising cost of capital continues to work its way through the system. It has already stunted the use of debt markets and private equity. It has reduced the size of foreign reserves, and also seen central banks try and reduce the size of their balance sheets. Some how corporates have managed to keep their cost of capital relative to government costs very low, but for how much longer?

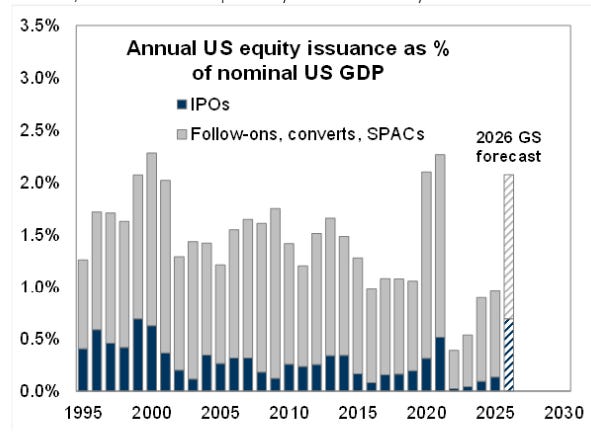

Hence corporates are now turning to one final source of capital, equity markets. And here we can see that 2026 is big year for IPOs.

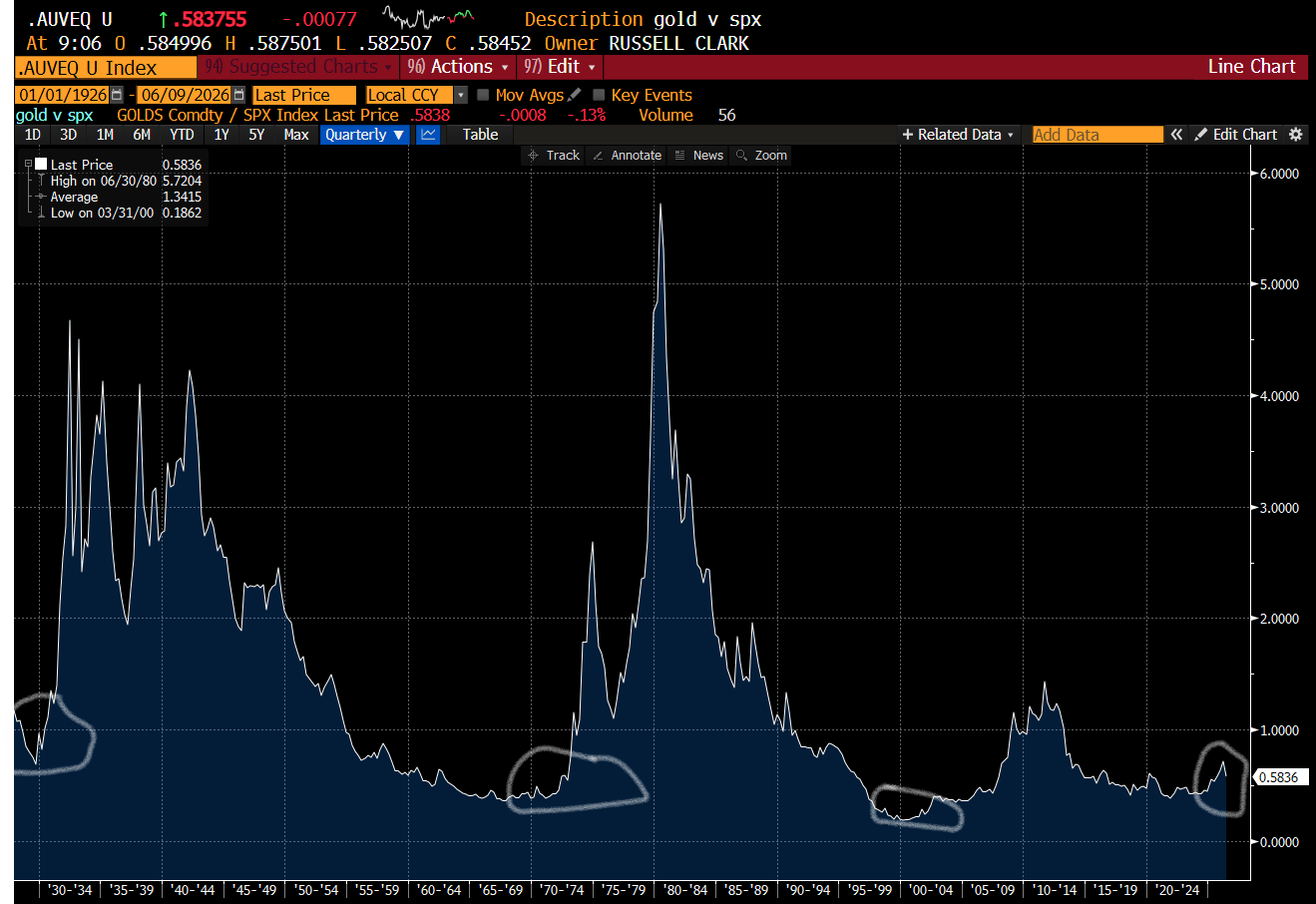

The question then is when or if does a rising cost of capital begin to impact equity markets? Or has it already done so? Gold vs S&P500 has been indicating issues for over a year now.

For big US corporates, they have engaged in “capital wars” with each other to dominate the AI trade. But how much capital is left? And it is making capital expensive for everyone. I can see the political winds shifting to try and get costs lower, but I can not see how that will come via wages or unemployment. At some point, governments will want to see price wars among corporates. I just don’t know when.