Back in January I wondered if semiconductors were the new oil. The price action this year probably says yes. Just as the Soviet Union tried to cripple the US in the 1970s through helping organise an oil embargo, the US is trying to cripple China through creating a semiconductor embargo. The US “war” with China was always about keeping China as a smaller economy than the US. From that perspective, it has been a resounding success. In dollar terms Chinese GDP has declined last few years.

The problem with embargoes, is that they heavily motivate those suffering from them to initiate policies to counteract and insulate them from a future embargo. In the US, the oil embargo led to reforms that reduced domestic demand, as well as encouraged increased supply from sources other than the Middle East. The end result of all these reforms was that we eventually saw the collapse of the oil price from near USD40 a barrel to USD15. With collapsing oil revenues, Soviet Union went into decline and eventual collapse. The unintended consequences of policy is often called blowback, and for the Soviet Union and OPEC, it was the eventually collapse of oil prices.

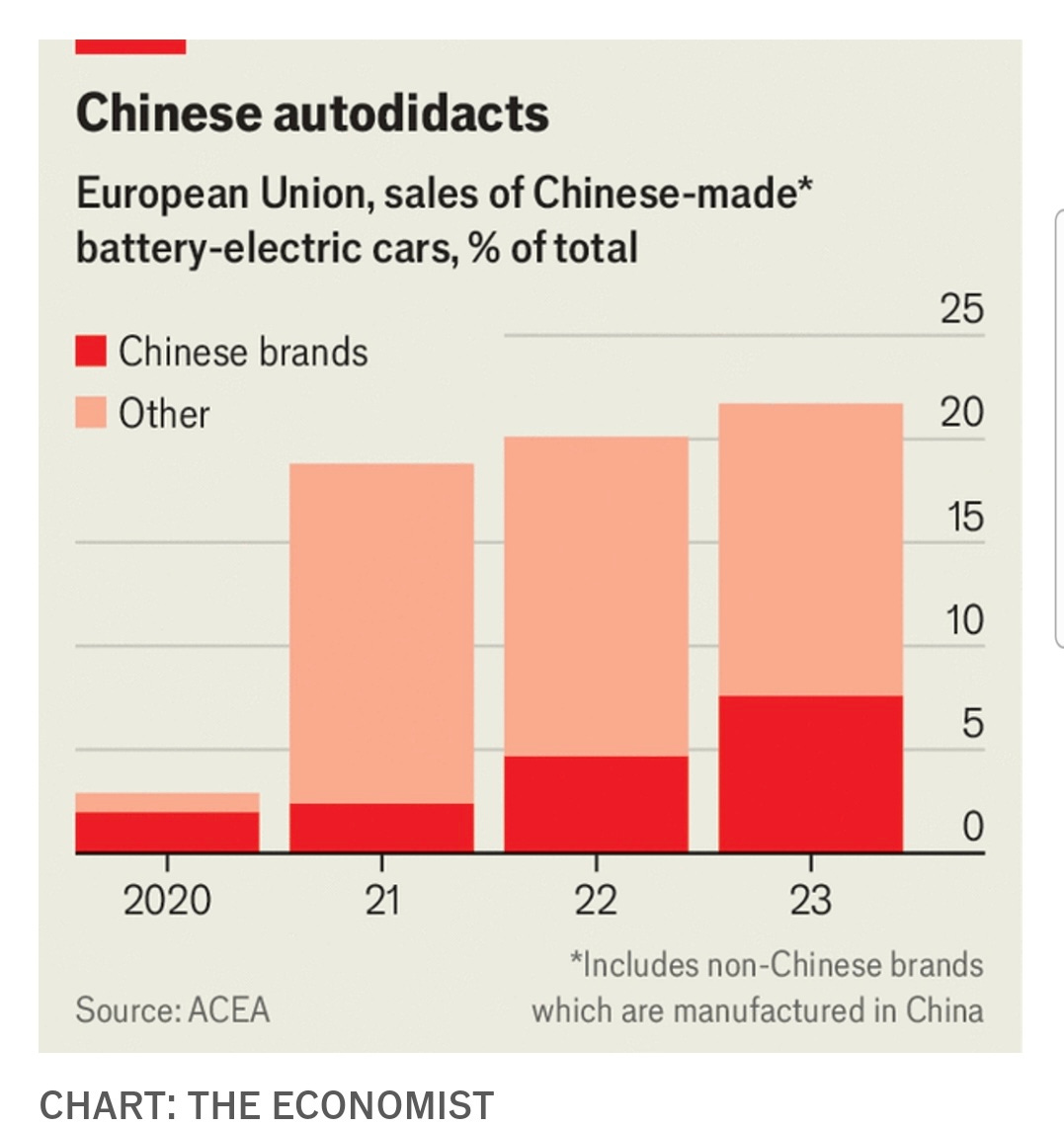

Banning high end semiconductor exports to China was meant to cripple development of high end industries in China. There is little evidence of this. China has become the world’s biggest exporter of electric cars. When I look at reviews of Chinese EVs on TikTok, they make Tesla look extremely second-rate.

EVs are not the main use for high end semiconductors - low end semis which China has pre-existing expertise in are probably sufficient. For AI and LLM, the very high end GPUs that NVIDIA sell are necessary. Even without access to high end semiconductors, there is evidence that China was able to approximate high end semiconductor performance through very aggressive use of low end semiconductors. Hence AI has ended up boosting the demand for all semiconductors. This would explain the phenomenal performance of Philadelphia Semiconductor Index. The embargo is creating demand across the entire semi spectrum.

A big driver in demand for semis has been AI and training large language models (LLM). It has been widely reported that a LLM price war has broken out in China. It is hard to understand how this is possible. It would be like seeing a price war among plastic producers in the US in 1974, just as their major inputs were soaring in price. After paying £14.50 for a Pimm’s at the cricket, I am shocked to see anything have a price cut - let alone the 90% prices cuts we have seen below. Some Chinese AI is now pricing at a 99.8% discount to OpenAI’s GTP-4. Whether this is a useful comparison is hard to tell, given the restrictions on access to Chinese internet (otherwise there is a huge arbitrage opportunity).

In a fully open free trading market, I would suggest the price war in China would have negative implications for Nvidia. And it might well end up that way - showing that AI needs a huge consolidation before it can be profitable. But what it does show is that Chinese policy of breaking cartels and fostering competition is producing exactly the results you would expect - lower prices. In the US, Meta, Google, OpenAI and Microsoft look determined to create a lock on high end Nvidia chips to starve out competition.

Increasingly the blowback for US policy to try and slowdown China, has been to spur an even more competitive Chinese tech industry, while creating a domestic tech cartel, with increasingly uncompetitive products : the iPhone continues to charge high prices for out of date tech for example, TikTok was destroying Meta and Google, while Microsoft remains Microsoft, Tesla looks pedestrian. Huawei has begun building an ecosystem completely independent of US tech. It would be no surprise if that system will produce substantially cheaper products.

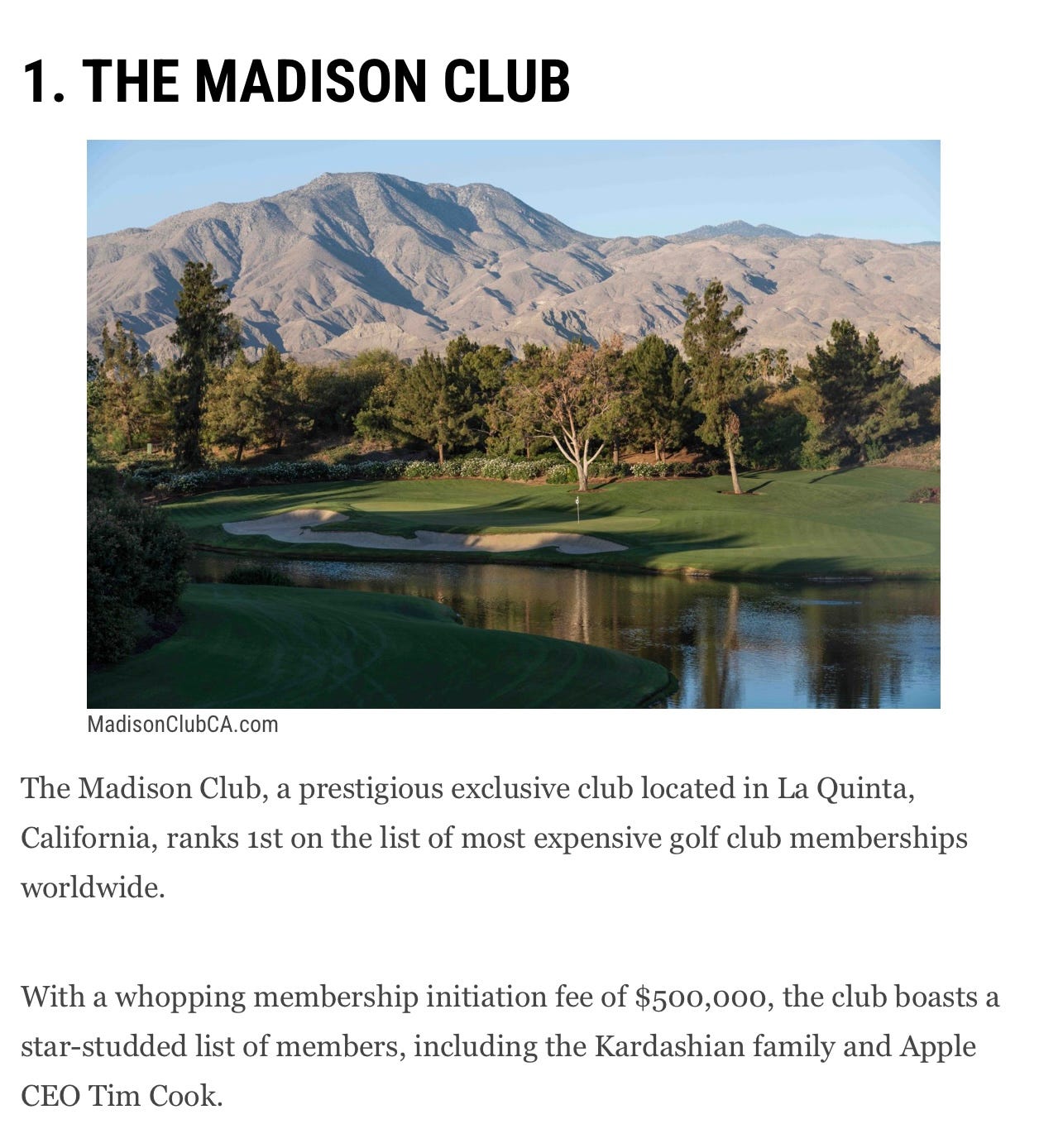

Combine this with US sanctions on Russian oil that has created a parallel financial system that cuts the US dollar out, it’s hard to escape the observation that US is making every single long term mistake possible. I am reminded of Japan in 1991, vaulting ambition just as it was losing competitiveness. The US now has vaulting ambition just as it was getting exposed on every single front. One very striking similarity is sky high golf club memberships. In Japan in 1991, golf club memberships were traded for millions of dollars. In the US, unlike Japan, there is no shortage of land, but USD 500,000 for a golf club membership does exist.

Unlike Japan, I expect the US dollar to take the brunt of decline in US industry. Our currency, your problem as the US government used to say - Switzerland is already showing the strain, having to cut rates even though they are already far below US rates. In a pro labour world, I thought growth would be strong, and higher rates would be the big problem for the market, but markets would flatline - and this has been true (outside of tech). But the more I look at the US, the more I think I maybe I wrong. Maybe we are headed to the greatest short selling market of all time - collapsing share prices AND amazing carry proceeds. Fun times - for short sellers anyway.