A few years ago, a friend of mine really got into the crypto area. I expressed my doubts, and he said I should listen to Michael Saylor. As advice to convince me of the merits of cryptocurrency, this was NOT good advice. As someone who made a career out of short selling, Michael Saylor videos were the ultimate red flags. The sail boat in the background, to the careful curation of “bitcoin resources” to be only on-message, with little talk of the potential downsides were classic red flags. Other red flags was a SEC investigation during the Dotcom boom for inaccurate financial reporting, that saw him settle. Typically when an executive has been caught out once, the disincentive to being caught out again is reduced. There is a famous Australia hedge fund manager who looks to short companies that employs people investigated by the SEC and other such financial organisations, who is doing quite well as far as I know. The website has a strong promotional vibe - another red flag.

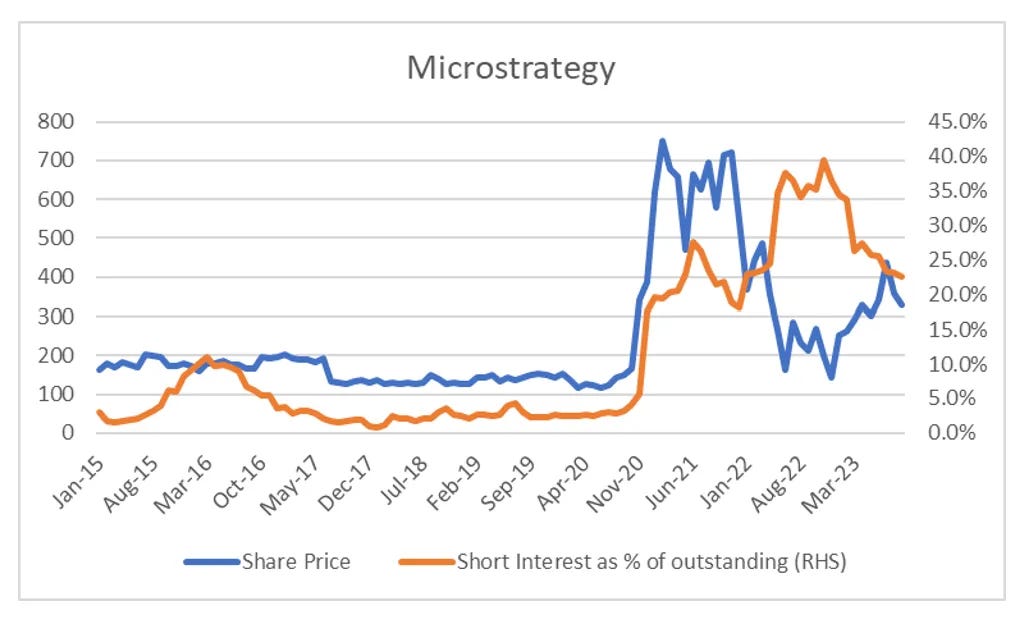

I was not alone in questioning both Michael Saylor, bitcoin and his strategy. Microstrategy quickly became one of the most shorted companies in the US, with over 40% of its outstanding stock out on loan, with a borrow cost of up to 35%. This was no doubt driven by the leveraged nature of Microstrategy’s investment into bitcoin, and the knowledge that there was potential for a margin call at USD 25,000

However, Michael Saylor and Microstrategy survived the crypto bust of 2022, and have just announced additional purchases of bitcoin to take Microstrategy’s holding of Bitcoin to 1%. The idea of controlling supply to drive up the price of an asset has a long and in recent years almost singularly successful history (Hunt Brothers tried to corner the silver market in 1979, BHP trying to buy RIO in 2008 are examples of failed attempts). I have to admit he may well prove successful in his strategy.

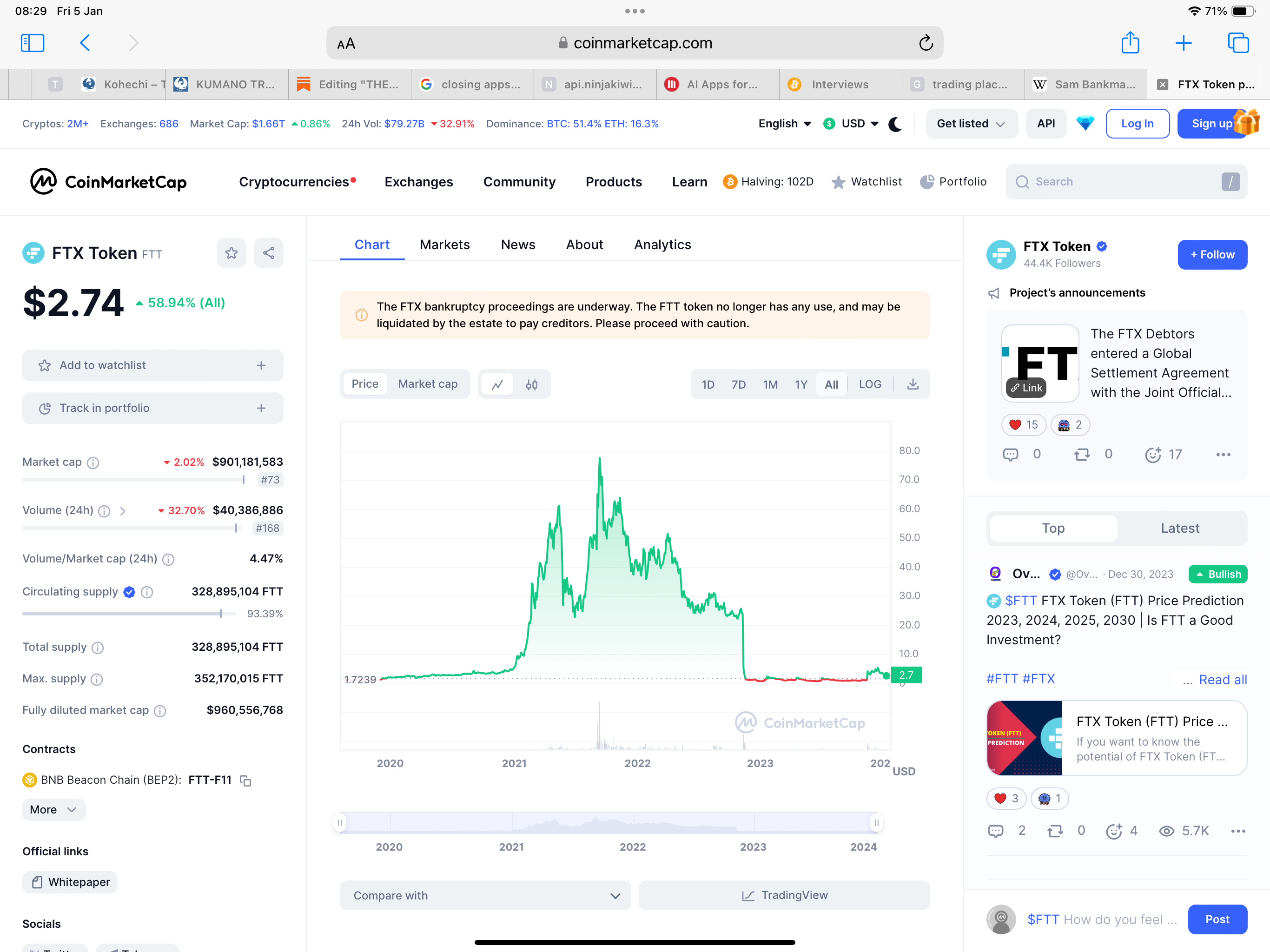

Sam Bankman-Fried (SBF) and Michael Saylor both studied at MIT and are now both heavily associated with crypto. In contrast to Saylor, SBF and his FTX were seen as “the good guys” in crypto, with big name investors and supporters. This good guy image meant there were clearly many red flags that investors glossed over. At the heart of the bankruptcy of FTX, was the failure of the FTX cryptocurrency FTT. (Full disclosure - a relative worked at FTX)

My point here is that as SBF was trusted, he was able to use his own crypto currency as collateral, and get away with poor corporate governance structure. The markets belief in SBF meant that it created a structure that could fail. The market’s (and mine) lack of faith in Michael Saylor meant that he needs to have a very transparent and robust structure. As far as I know, there has been no push, and no demand for a Michael Saylor cryptocurrency (If such a thing actually came about, it would be a good sign that crypto area was getting frothy again). And here is the irony, the current success of Michael Saylor probably owes a lot to the markets lack of trust in Micheal Saylor. Or as an old fund manager once told me, dodgy assets are ok, as long as they are priced as dodgy assets. The problems happen when dodgy assets are priced as good assets. The GFC, Eurocrisis and now FTX are reminders of the financial paradox of dodginess - that dodginess is only really a problem when it is not priced in.