Domino’s Pizza is one of the best performing stocks in the US over the last 15 years, and is up 75% from the lows in 2023.

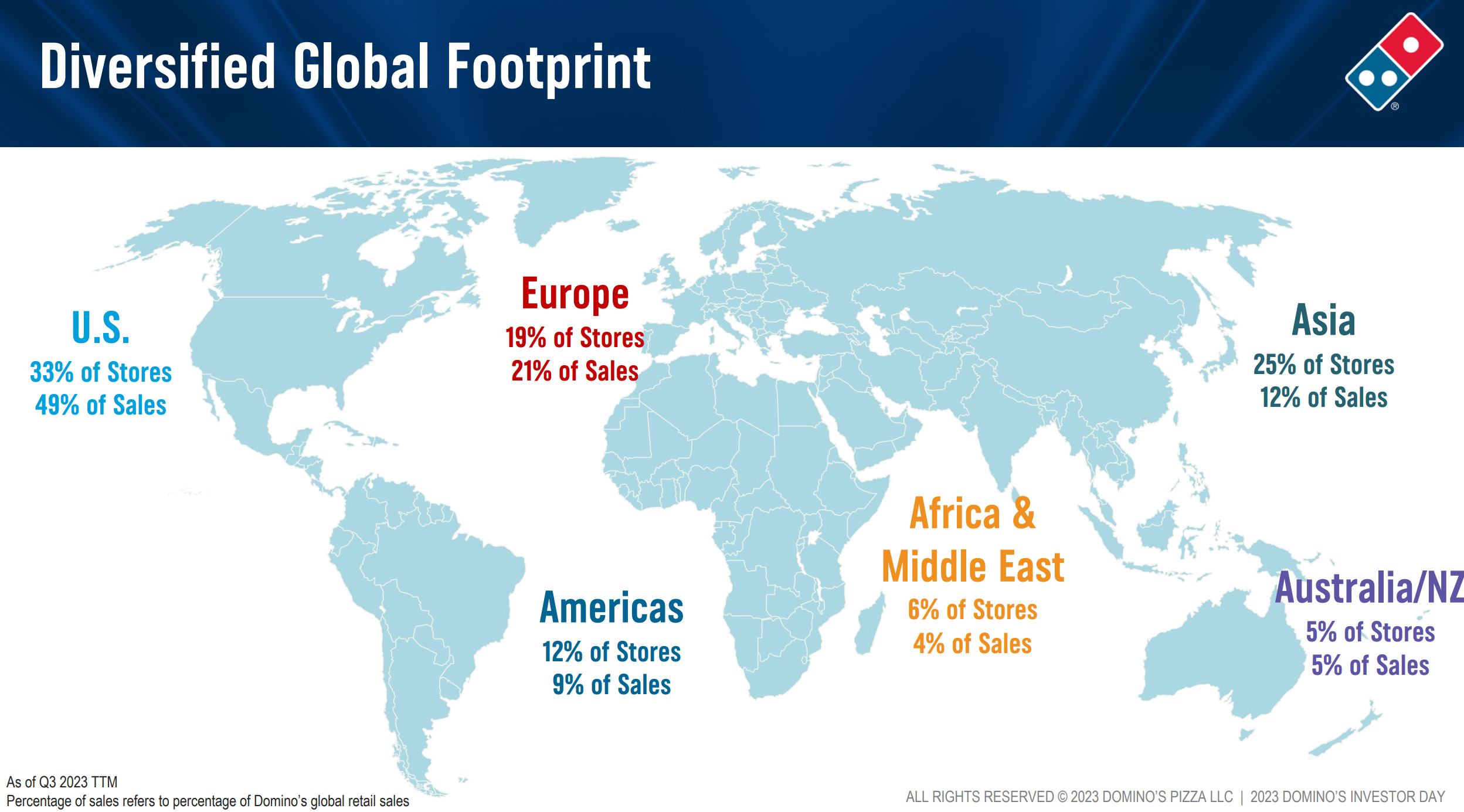

Dominos is a truly multinational business. 66% of its stores and 51% of its revenue is generated outside of the US.

Outside of the US, Domino’s runs a 100% franchised model, through what it calls a master franchise system. There are 46 master franchisee of which are 7 are listed.

What is unusual is that DPZ US, the parent company is close to all time highs, but Jubilant FoodWorks is back at USD levels first seen in 2020.

The Australian listed Domino’s is also the master franchisee for most of Europe and Asia, excluding India and China. As can be seen below, they are big in Australia, New Zealand and Netherlands, and looking to grow in Japan Germany and France.

The Australian listed Domino’s master franchisee is back at level seen 10 years ago in US dollar terms.

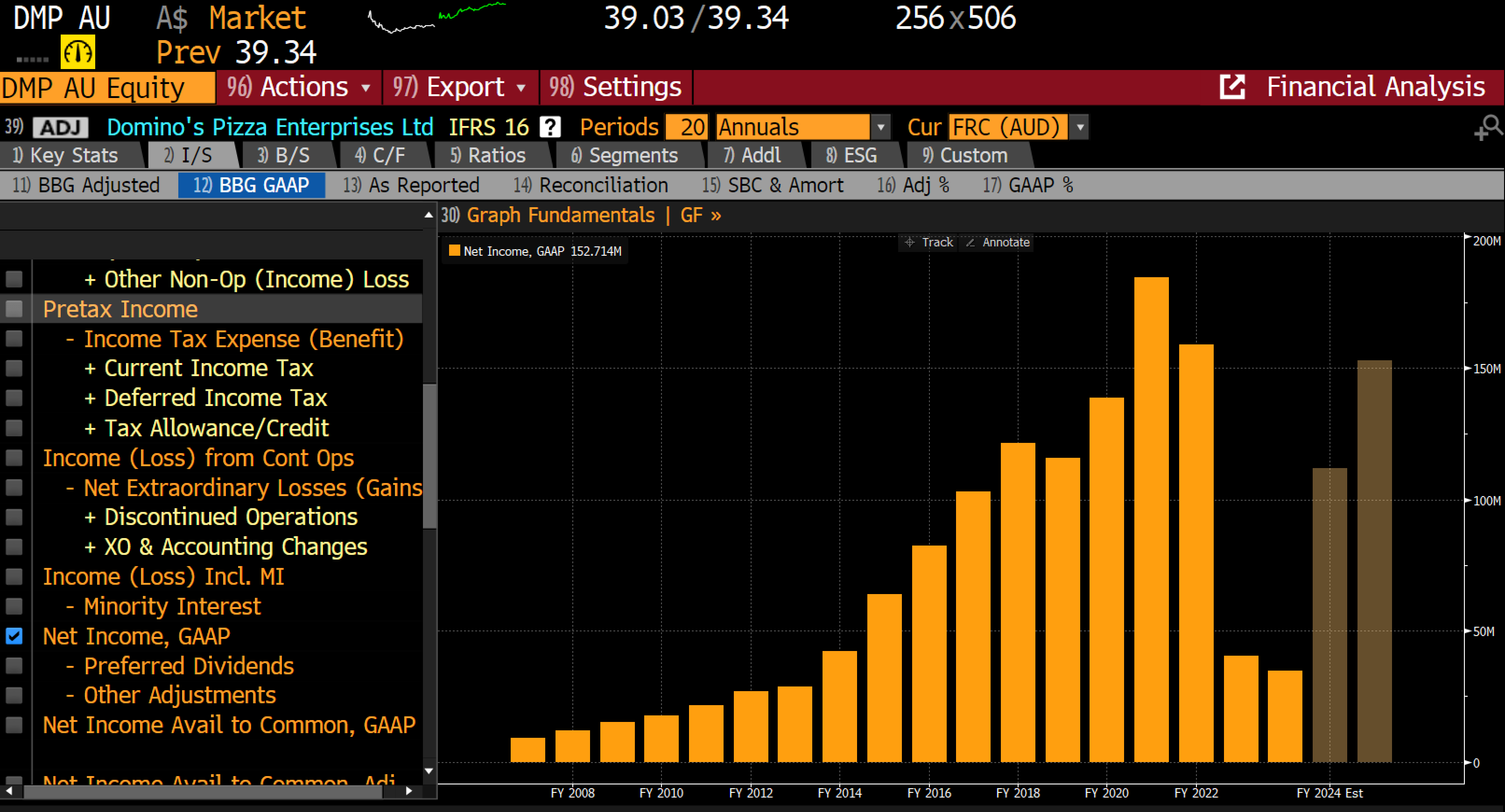

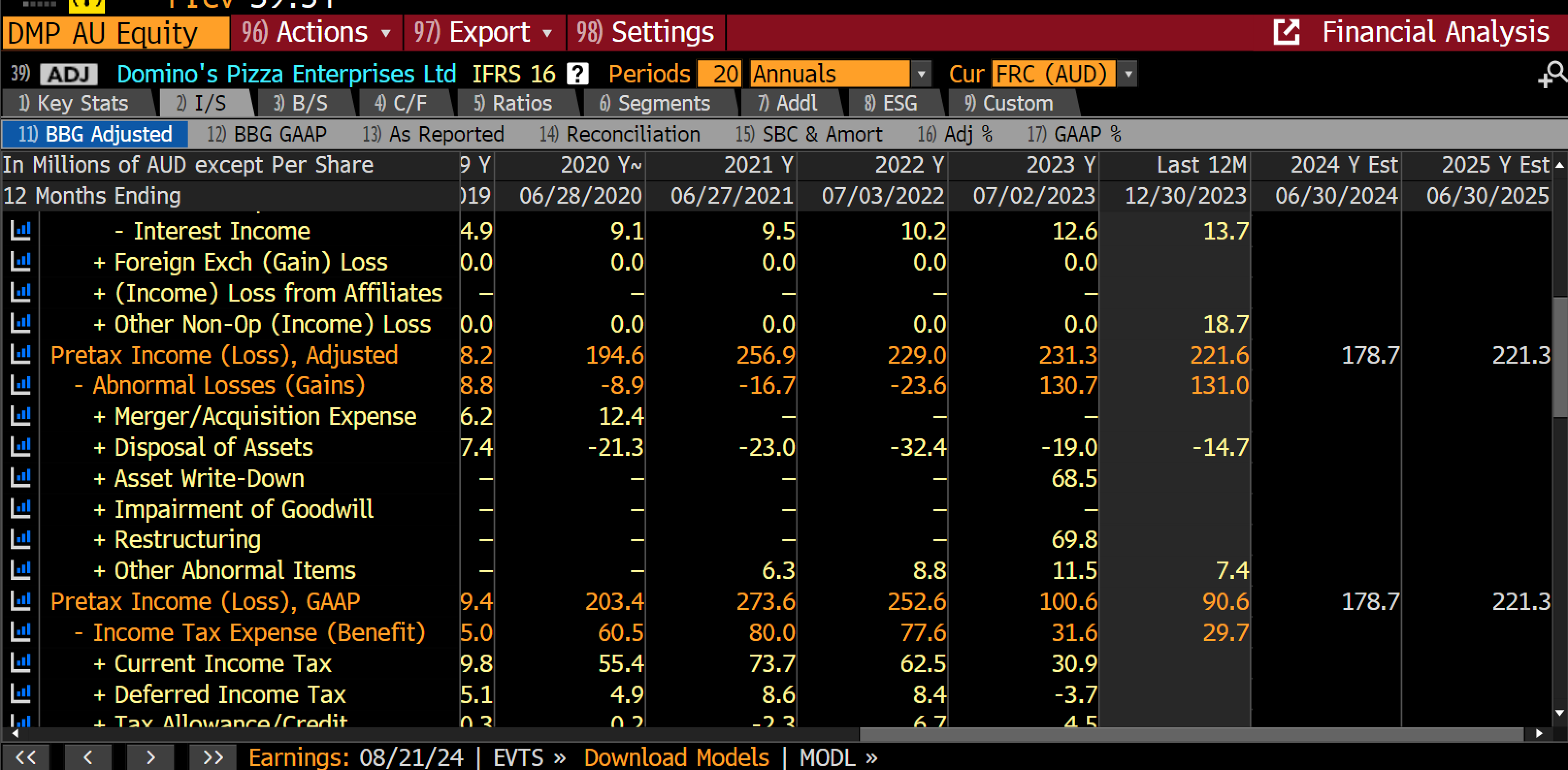

The problem for the Australian listed company is that net profits have collapsed in recent years.

The collapse in net profits have come from write down of assets.

Looking at the parent company share prices performance, this makes the weakness of the Australian listed company a bit hard to understand. However, looking at the half year presentation, there are some worrying metrics. The biggest one is that profitability of the franchisee is falling.

So here is where it gets weird. The US market, which is the most penetrated and theoretically competitive market, is driving the share prices of DPZ US, where as the growth markets of underpenetrated Asia and Europe, and growth markets of China and India show real problems, with franchise profitability falling. Logically, DPZ should be a no-brainer short, but I would have thought this 75% ago. Here is where you have to accept the “truth” or market pricing. Domino’s Australia has seen its share price fall with earnings estimates.

While the US Dominos (DPZ US) inflected higher as earning inflected higher. You could argue about the size of the rally in DPZ - but stocks follow earnings, and you should never short stocks with rising earnings.

Close competitor, Papa Johns, is struggling with a share price at levels first seen 10 years ago.

Intriguingly, Starbucks, which is still mainly a US focused chain, has falling earnings.

After going through all this, I am left with a quandary. If I look at the share price of Domino’s Australia, Papa Johns, Jubilant Foodworks, and Starbucks, I would come to the conclusion that fast food chains are struggling. But then Domino’s suggests that the US business is fine, and the stock market rewards it with a 75% surge in value. Do I short Dominos US? Do I buy the other listed Dominos companies? Do I just go with momentum, and buy Dominos and short Papa Johns and Starbucks? When I have shorted before, I have looked for a consistent message from the market - in this case I am looking for a sign that the fast food industry is turning bad. Logically I can see it - but the performance of Dominos makes me nervous to short. I will investigate further, but here is a worked example of the problem with short selling at the moment.