In my last post, I had guessed that something was brewing in markets. What I suspected was a sell off in long term bond yields. I still think that is going to happen, but what the market got was capitulation from Jerome Powell to President Trump. With this capitulation, there are no longer any independent financial institutions left in the US - or to put in another way, fiscal and monetary policy is now fully politicised. The market reacted in a predictable way - gold rallied, US dollar weakened and the likelihood of a recession was cut. One of my favourite indicators is 8mth generic VIX. When it is rising, recession risk is rising, and when it is falling the opposite is true. During the GFC, the Eurocrisis, China Deval concerns and Covid, it moved higher as investors hedge, and then falls as recession risk fades. It fell 3% on Friday, and looks to have turned lower.

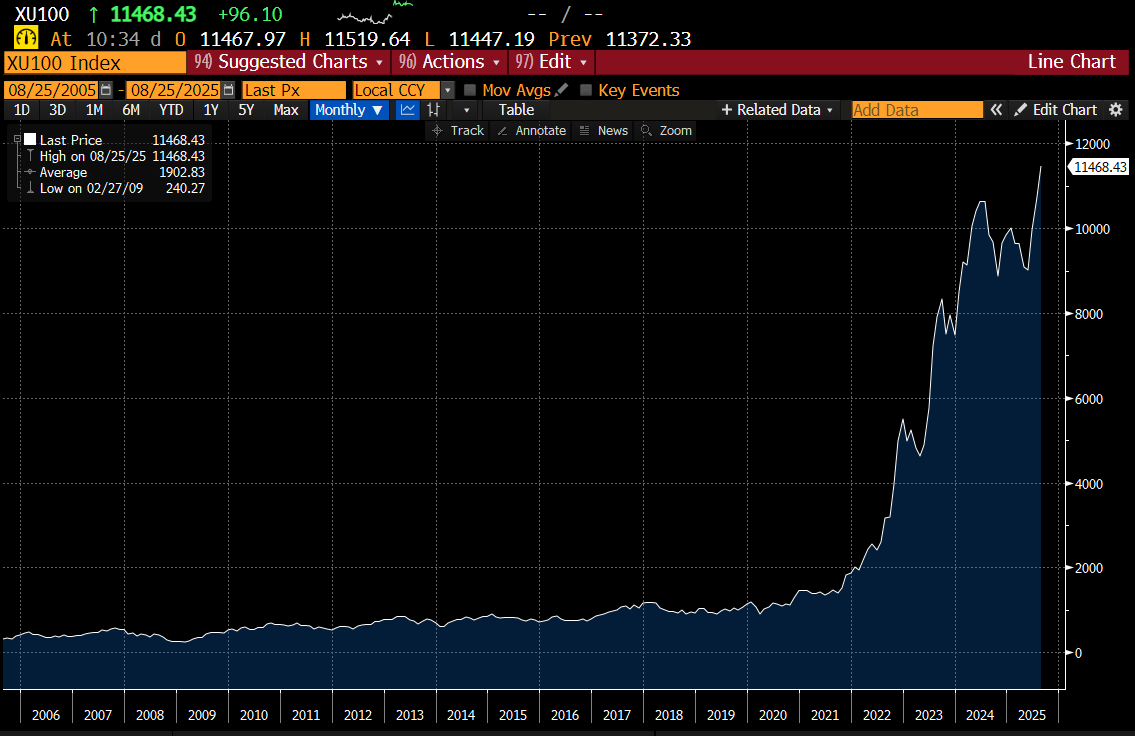

In a pro-labour world, weak assets prices are not really a problem. In fact they help reduce income inequality, and reset property markets. I see pro-labour tendencies in the UK and in Mexico. And for a while, I thought Trump 2.0 was a pro-labour politician. The “Liberation Day Tariffs” seemed very pro-labour at the time. But in practice, Trump is not really a pro-Labour politician, he is just a pro-Trump politician. In this respect, he most closely resembles Erdogan in Turkey, and to a lesser extent Putin in Russia. As it happens, I have been around for the investment journey with both these leaders. It starts off with some useful pro-market reform. And then is followed up by taking on unpopular vested interests (the army in Turkey, oligarchs in Russia), but while both were seen as improving democracy to start with, in the end it was to concentrate more power in the Presidency. After awhile, fiscal and monetary policy gets compromised, and corruption flourishes. This is all beginning to happen in the US. As is my way, I made money on the way up and the way down in Russia and Turkey - but principally from shorting the currency. Shorting locally listed stocks in Turkey is a not rational.

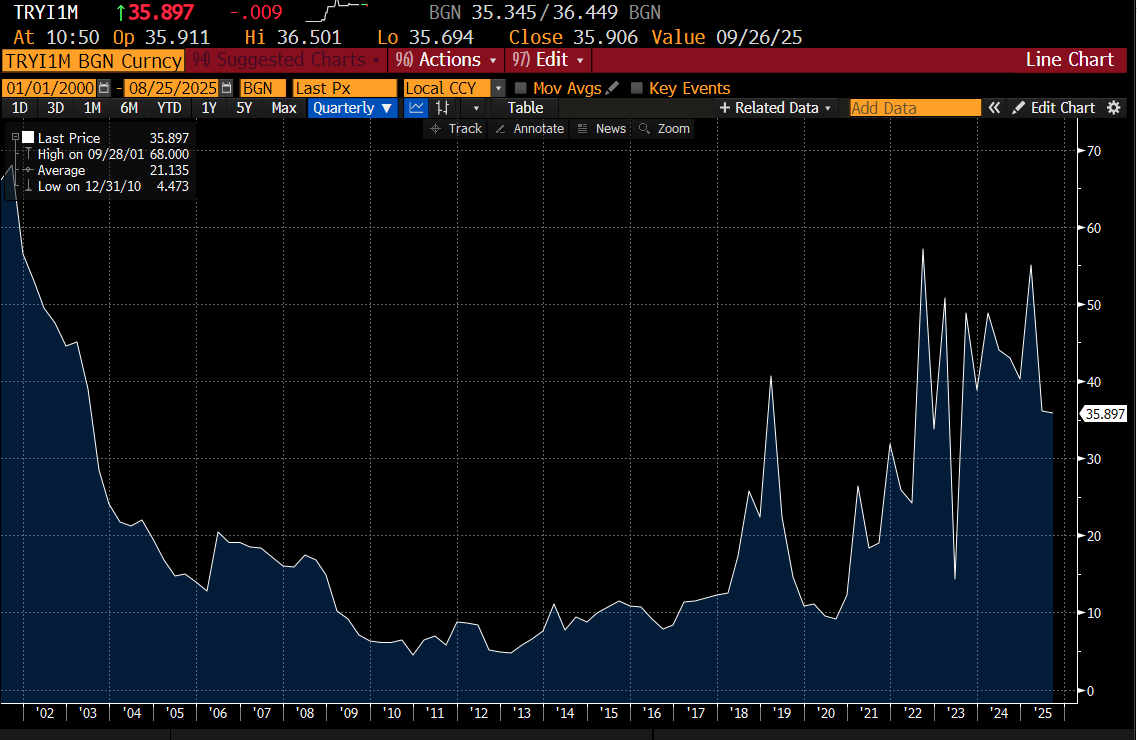

But being bearish on bonds in Turkey does work. 1mth interest rates have gone 10% ten years ago to 35% today.

From a simplistic point of view, the GLD/TLT trade should keep working. This looks ready to move much higher in my view.

I have been running a triple track of being bearish dollar, bearish treasuries and bearish US equities. It looks like Donald Trump is very happy to trash the dollar and treasuries to keep equities going, so its hard to be that bearish on US equities here. The question I am asking myself is does the rest of the world begin to adopt US policies to embrace growth? That is debasing their bond markets and currency to get economic growth. It certainly looks that way in Japan. Yields are at a new high.

I find myself drawn to Japanese inflation trades, partly because Japan looks so cheap relatively, but also unlike the US, Japanese households have so much cash. There are signs that deposit holders are realising they are getting fleeced, and money is moving to real assets. We have seen the Nikkei break out.

What does this mean? Well market strategists have called current investment strategies as ABB - Anything But Bonds. Hard to disagree with this. In practical terms, the strategy of long SPX/Short TLT has been very good - even delivering positive returns in 2022. From February to April, there was a brief period where you could think things were changing - but we have returned to normal coverage.

What’s the end game here? Well once people are wise to what is going on, they no longer leave money on deposit. Everything gets put into inflation hedges, and if interest rates are too low, then credit demand surges as people see borrowing as free money. Governments start running out of money, and they use all sort of wheezes to get cash. Current talk of stable coins acting as demand for treasuries remind of this sort of chat. Stable coins are to help people to get away from treasuries - not to support them.

Something wicked this way comes - is still true. But rather than weak asset prices, we are going to see accelerated inflation.