One ounce of gold currently buys 38 barrels of WTI oil. This ratio has only been seen in the great depression, before the dollar devalued, and during Covid.

There is a risk, we are really at the end of the age of oil. Then the only ratio we should be concerned with is gold/copper (copper being the vital commodity for electrification). But oil matters as it seems to be the commodity that drives inflation expectations, so it price movement remain important.

The big revolution has been in shale oil in North America. Production seems to be levelling out at 13.3 m barrels a day in the US, a number first seen in 2019. Slowing production growth should be bullish.

And a similar trend in Canadian oil production.

Shale oil production tends to produce natural gas, and well before US oil prices went negative during Covid, US natural gas prices would often be zero to negative (i.e producers would pay for someone to take away the gas - and would make enough just from the oil). Hence, I look at natural gas pricing to see if US shale producers are beginning to rationalise production. NGF28 below refers to January 2028 natural gas pricing, which changed dramatically in 2022. Forward pricing has held, up but not collapsed, which I see as bullish.

However, that being said, El Paso Natural Gas pricing (El Paso is near the Permian region - so area where production of oil and gas is still growing) has recently dropped back to negative spot pricing. So spot, and long dated forwards are telling a different story.

As it happens, the EIA no long produces a separate report on shale drilling, and includes the data in the DOE Short Term Energy Outlook. I am still trying to integrate the old data - but for our purposes, we can look at the Permian data. As suggested with other data, drilling in Permian has rationalised.

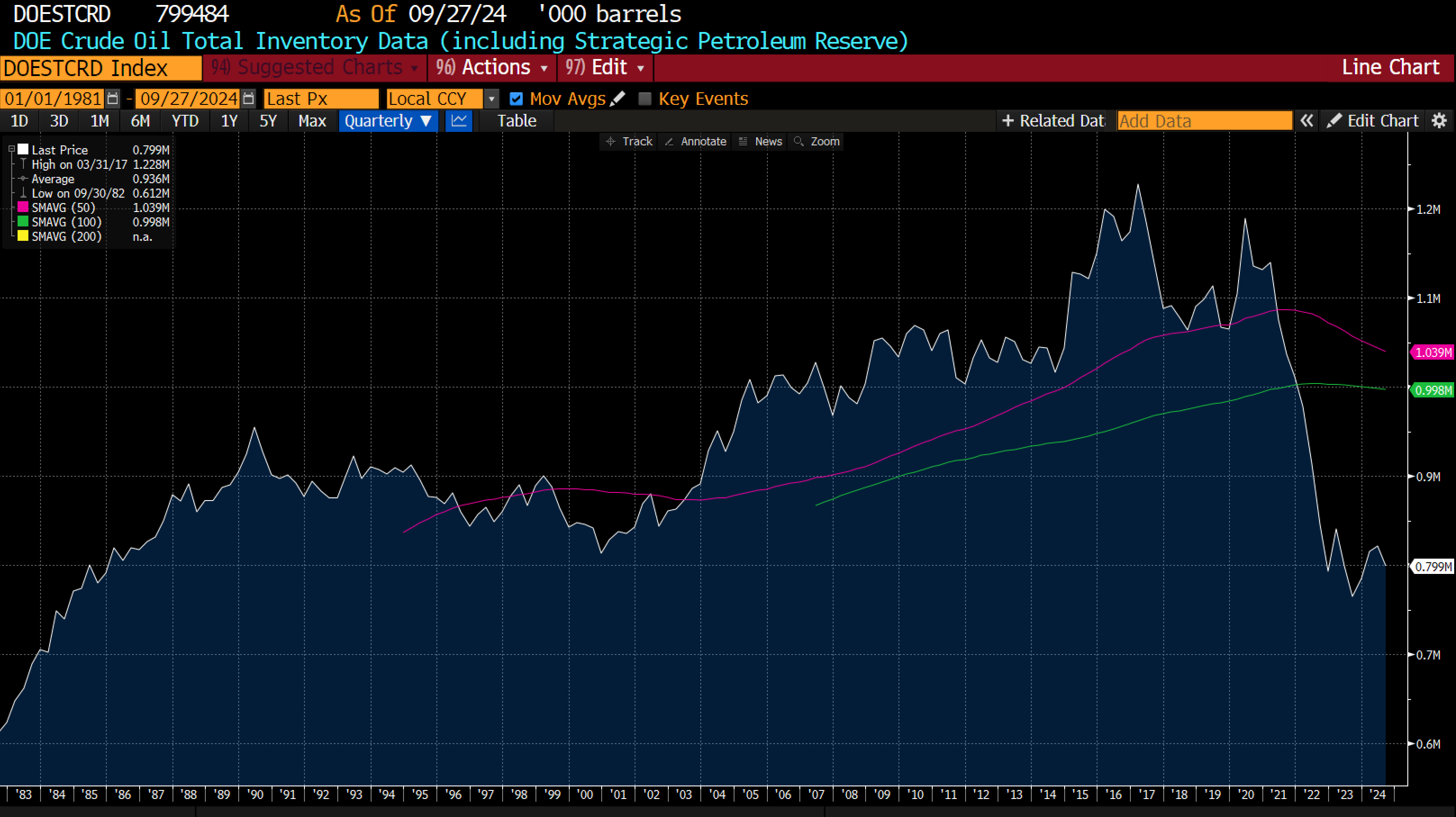

So why is crude oil so weak relative to gold? Inventory data is not useful - it shows US commercial crude oil inventory at lowest level in 5 year - which is bullish.

Even with the SPR beginning to increase inventory levels, we are still at very low levels.

It hard to find a good reason for the break between gold and oil, unless we start thinking in terms that energy consumption is ex-growth. Using the old BP Statistical Review numbers (now housed at the Energy Institute) Energy consumption per capita is falling in the developed world, and Asia and South America are already at 50% of European levels. Africa offers the potential for growth in consumption, but there is little sign of change at the moment.

When you add in collapsing solar power and other renewables fossil energy could be on the way out?