The founding idea of Iran is conflict with the US. In some ways, it has been surprisingly successful. The Soviet Union only became enemies with the US post World War II - if you mark the beginning of outright hostilities as the beginning of the Korean War in 1950, to the collapse of the Soviet Union to 1991, this was only 41 years. Modern Iran was founded in 1979, and survives today, 47 years later. This is despite far less industrial might, and population. Why has Iran survived so long? Well for most its life, the US needed to import oil, and confrontation with Iran was just not worth it. But in 2020, the US became a net oil exporter and the calculation changed.

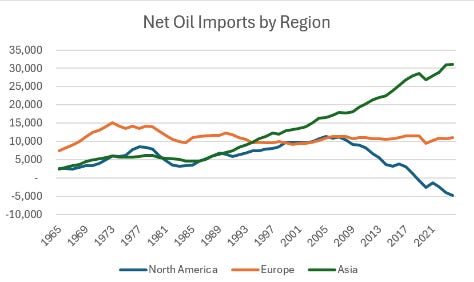

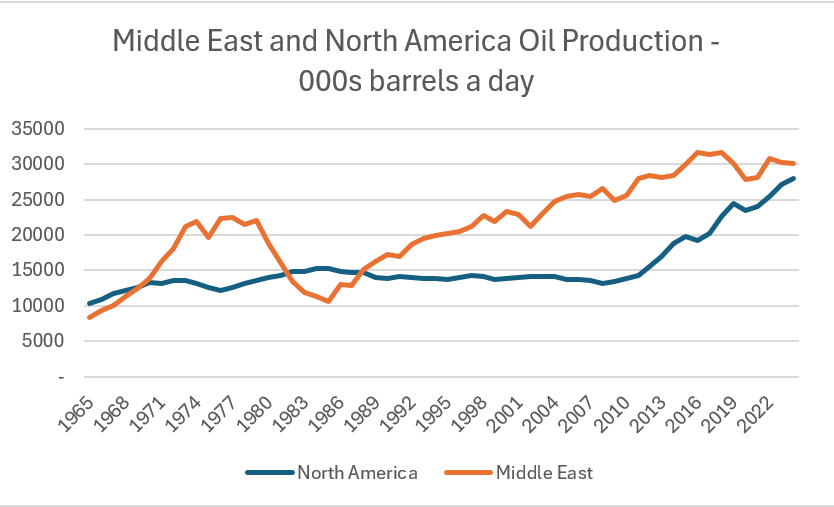

Of course Iran survived because it threatened all Middle Eastern oil and gas production. But with surging US production, it has been losing market share. North America is nearly a larger producer than all of the Middle East.

Closing the Strait of Hormuz was supposed to be so traumatic, that this would stop the US or anyone else attacking Iran. But with changing energy dynamics, the US has called the Iranian bluff here. The problem Iran has is that Russia already tried using energy as a weapon and failed. When it stopped sending gas to Europe, natural gas prices in Europe surged from EUR/MWh 20 to 350. This is well over USD 400 a barrel equivalent.

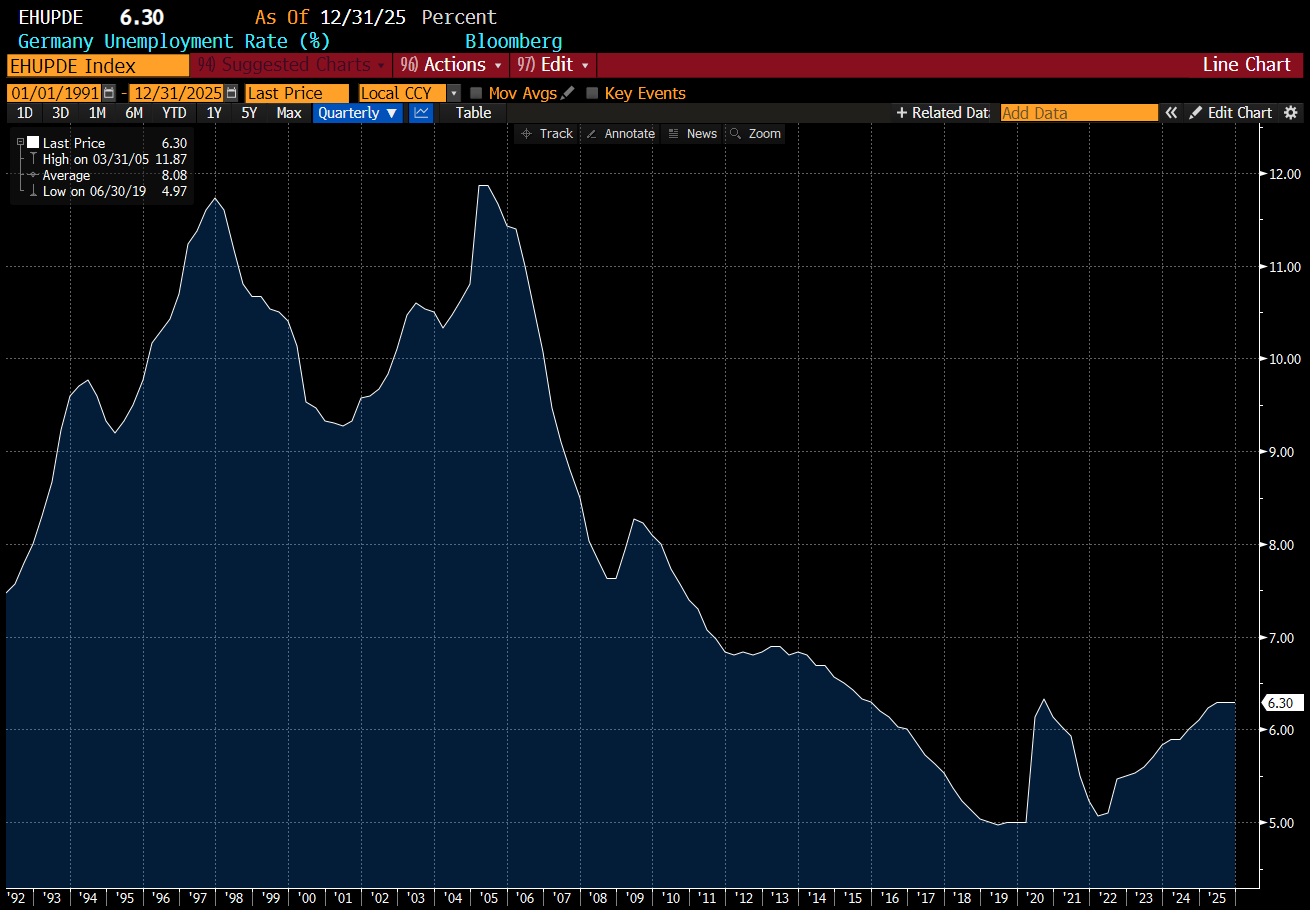

Germany, which has built an economic model on cheap Russian gas, has seen unemployment stay at levels on part with boom times. That is the energy weapon did not work.

What is extremely problematic for Iran is that surging oil prices only affect nations that are diplomatic allies of a sort (Europe and Asia would prefer a peaceful resolution). At least the Russians use of the energy weapon was directed at the nations funding Ukraine. The Iranian energy weapon can only cause collateral damage. In fact, by drawing in other regional players, it makes the Iranian endgame of regime change even more likely. If they cannot be relied on to keep the oil flowing, the Saudi and other nations will also come to see the need for regime change. Generally speaking the markets are saying the same. When I look at long dated US natural gas futures (January 2030 in this case), you can see when the Russians turned off the gas in 2022, but you struggle to see the closing of the Strait of Hormuz in this price graph.

While it is easy to think the US is heading into a quagmire like Iraq or Afghanistan, in this case other regional powers are also keen on regime change. What exactly is going to stop Israel from attacking Iran while the IGRC are still in charge? How can Saudi tolerate a nation that closes the Strait of Hormuz? With Donald Trump, the IGRC have a US president that could cut a deal, and enforce a deal. The longer they wait, the more likely that US politics changes, and then they face a long war of attrition which they can not win. And all the time, the Middle East becomes seen as an unstable supplier of oil, and their market share fall further. All options now for the IGRC are bad - but there is an incentive to try and make things worse to get better terms on a final deal - but the outcome is the same - the end of the IGRC has a regional power. Either this happens through regime change, and the Iranian people are finally allowed to prosper, or IGRC digs in, and leads the nation to be destroyed as happened in Syria and Afghanistan.

From an investing perspective, this makes things tricky. The short term outlook gets messier and messier, but the long term outlook gets better and better. No matter what happens, the energy market will become more stable. If Iran capitulates, then the region becomes safer. If Iran does not, then more and more energy production will move to politically stable regions like the US or Australia. But what the War in Iran does do, it accelerate the trends that were already clearly visible - a rising cost of capital. 30 Year JGBs have resumed their sell off, with yields back to near highs.

Maybe oil goes to USD 200 a barrel, or maybe it doesn’t. That is in the hands of the Iranian leadership, who probably know the gig is up, but don’t know what else to do. But for me, rather than bet on an unknowable actions, I think I would rather focus on a rising cost of capital - a trade that is driven by western politics - and much easier to track and follow.