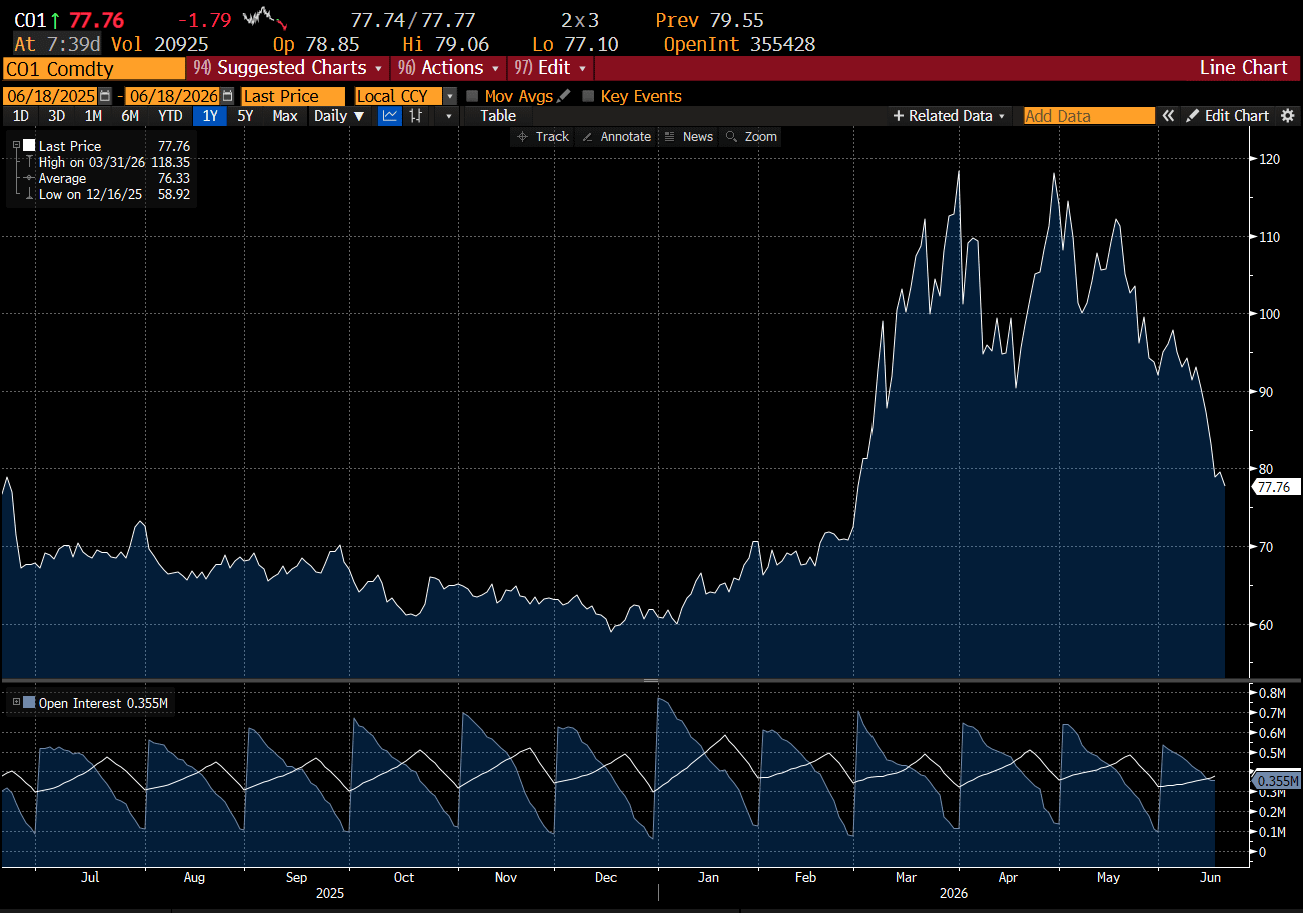

Generally speaking, I have gotten most of the big calls right. Unlike the vast majority of the "macro community”, I did not think closing the Straits of Hormuz was going to be a massive problem (see my Gays of Hormuz note). In essence, I argued that closing the Straits only really hurt China as an oil importer, and would just accelerate the development of alternative energy sources. That is chasing the oil trade in March looked like a good way to lose money - which has proven correct.

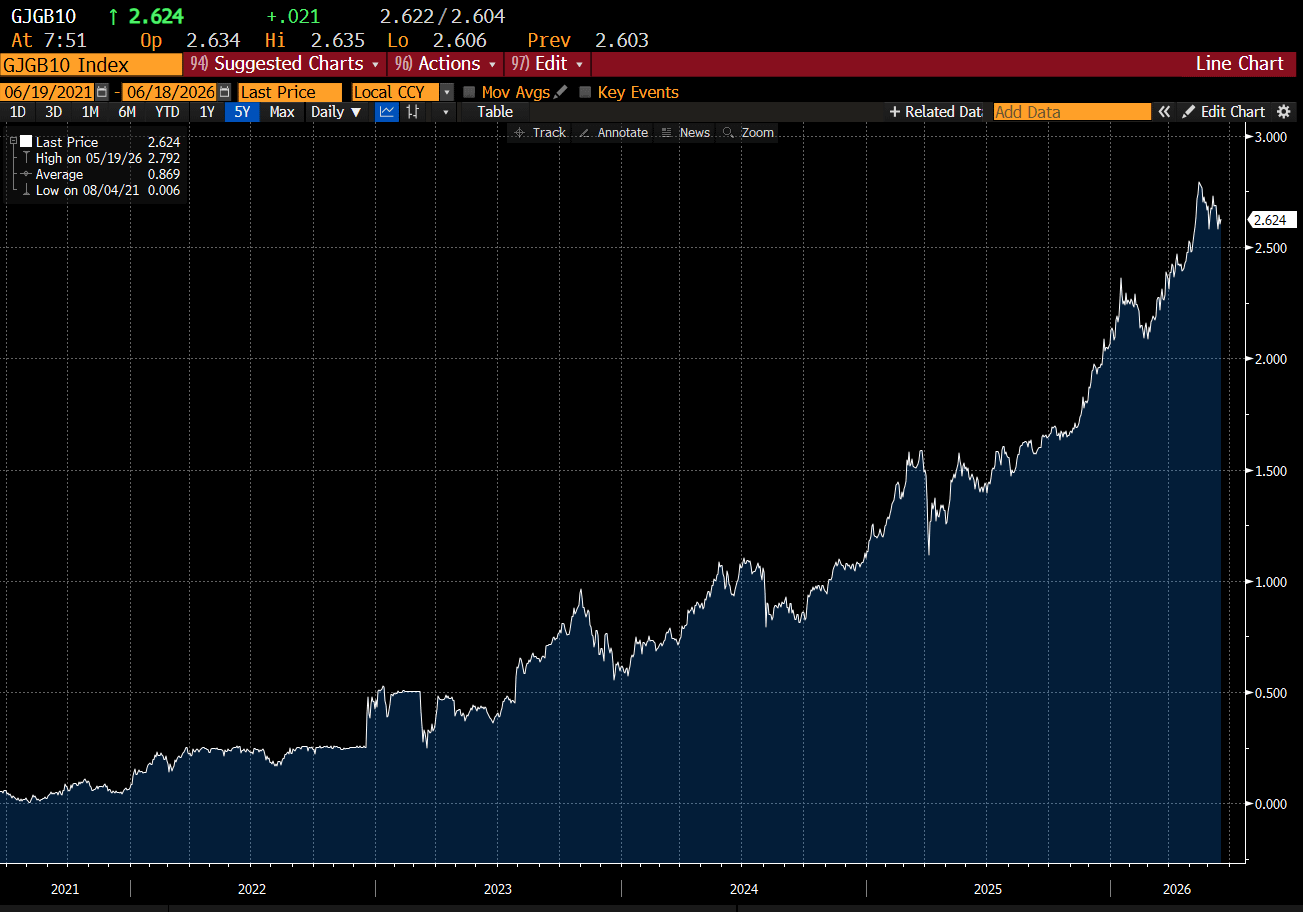

I have expected yields to keep rising - and 10 year JGBs are now at the 2.6% - a level that would have been unthinkable not that long ago.

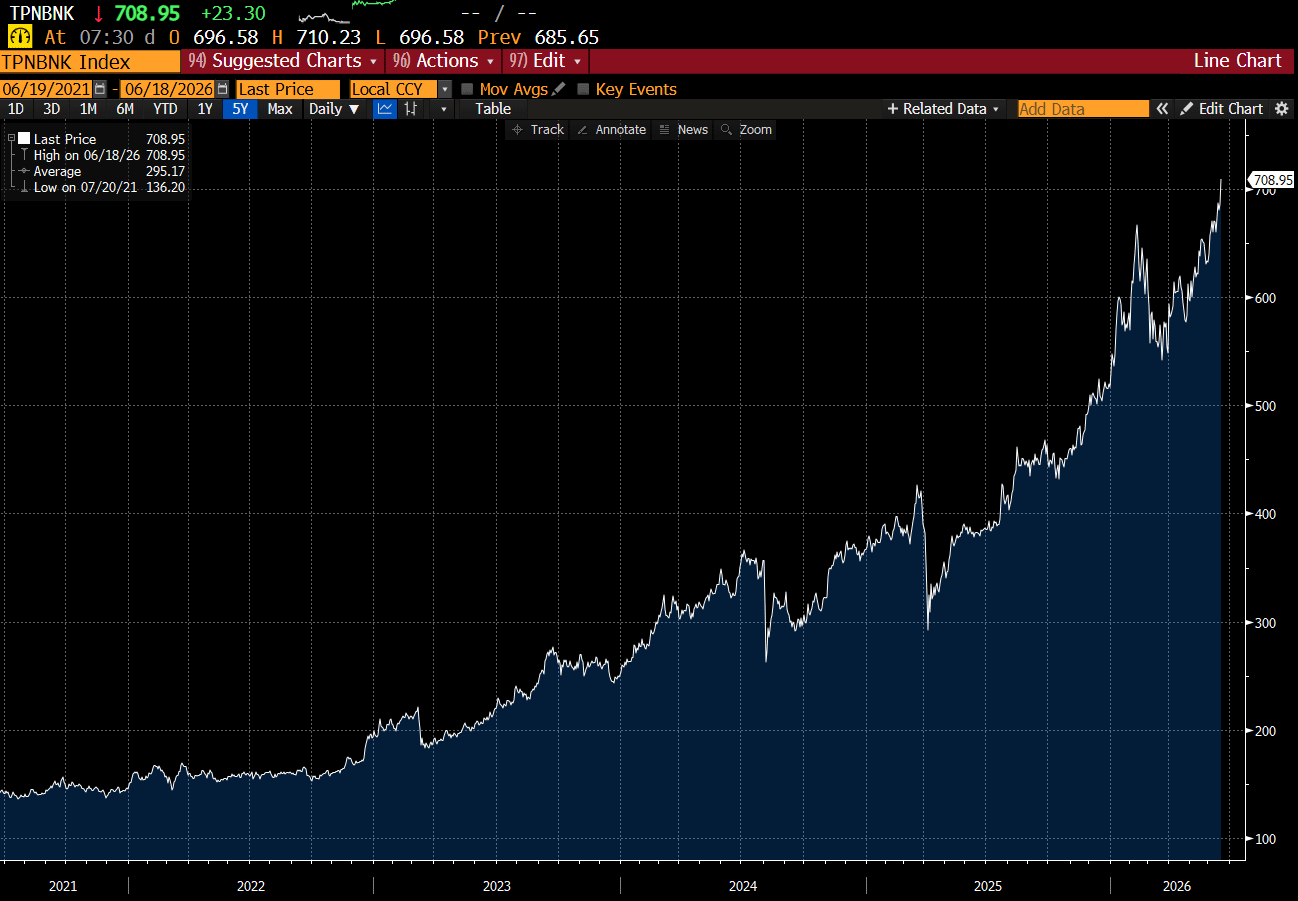

And this has played out well in my preferred expression of JGB bearishness, bullishness on Japanese banks. Topix Bank Index continues to trade well.

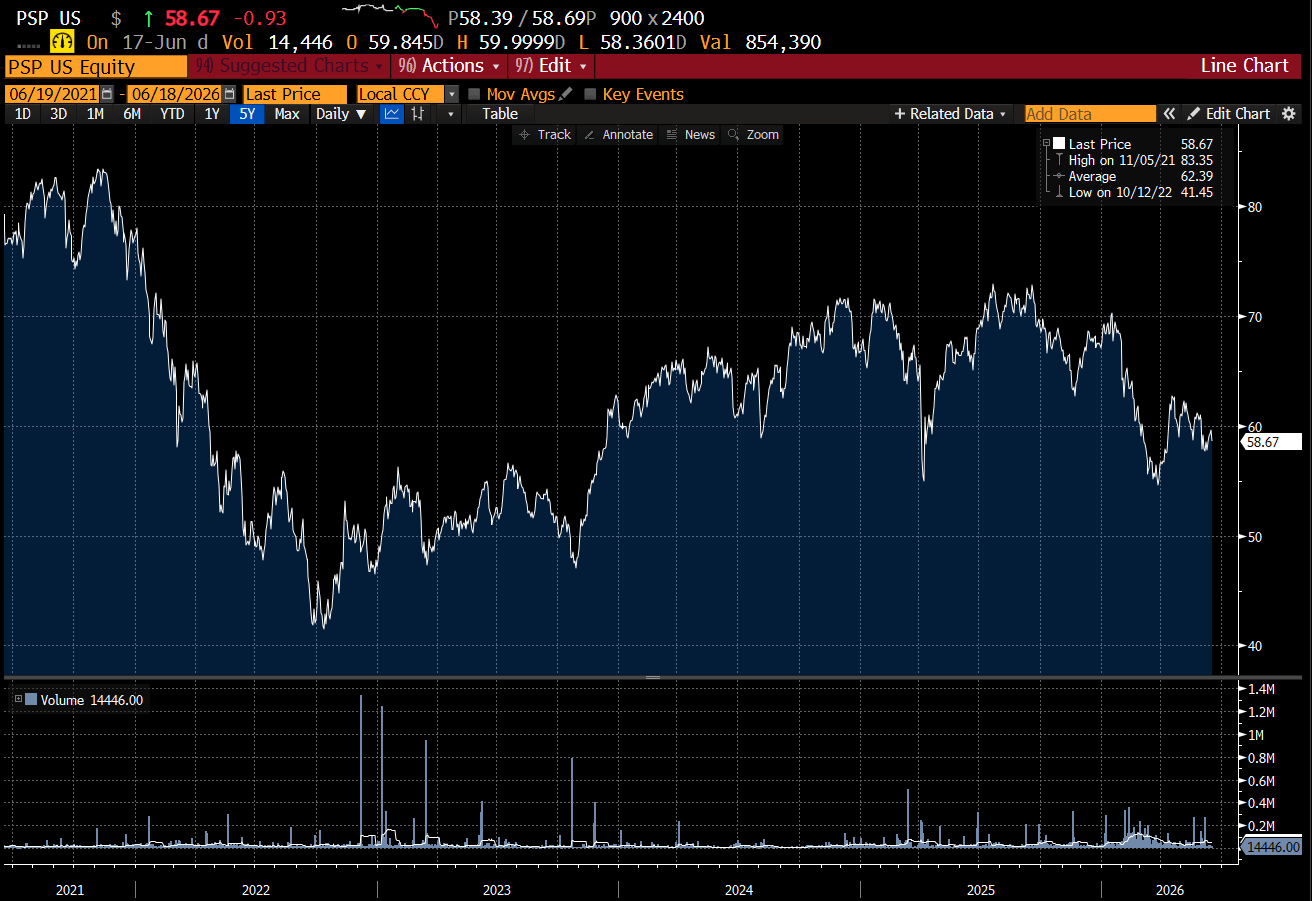

I also thought that rising rates would make like difficult for private equity/private credit. This has been correct. Invesco Global Private Equity ETF is a good proxy for their travails.

I did start to get bearish parts of the AI market, as it seemed like credit markets were not willing to fund the AI spend anymore. But with SpaceX IPO, it looks like retail investors will take over the capital baton. But there ARE mixed signals from this space. Meta, Microsoft and Oracle both have traded relatively poorly this year. But just when it looked like it might unwind, SpaceX, OpenAI and Anthropic are all rushing for the IPO door. This makes things more difficult, and I think it is right to have a more nuance outlook.

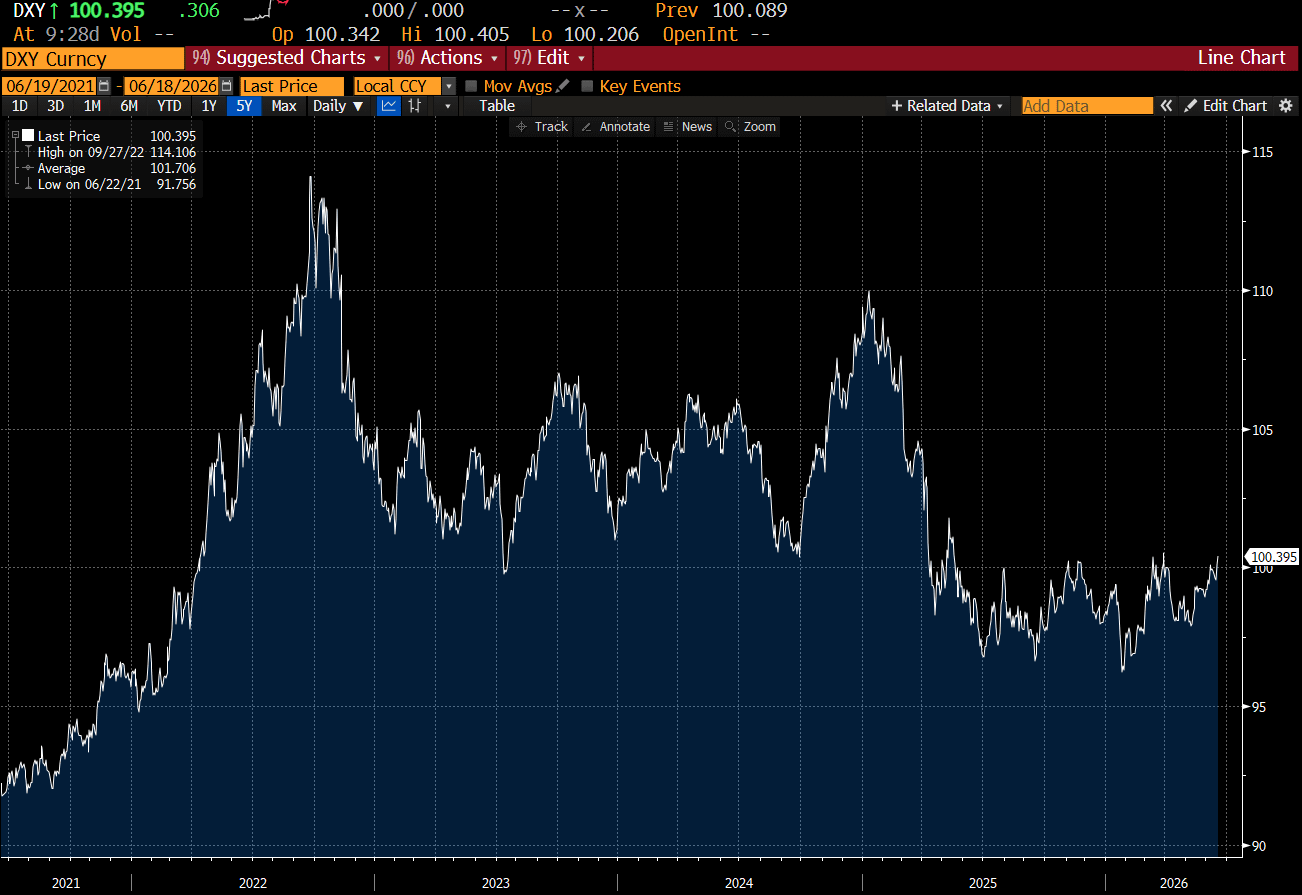

Generally speaking, I have a bias towards weak dollar, but not aggressively so. If we look at the dollar index - its has gone nowhere this year.

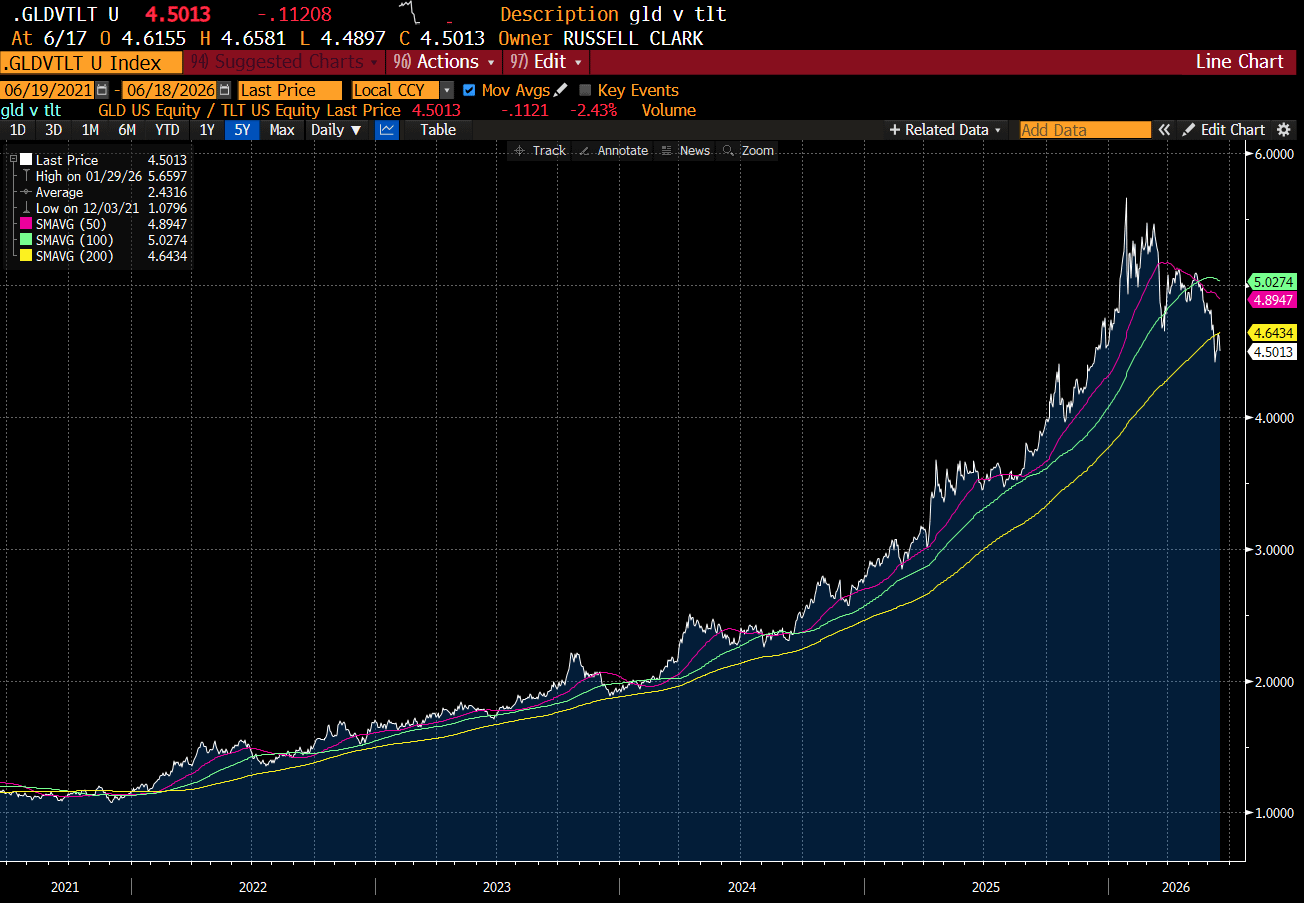

Coinciding with dollar strength, my key recommendation, GLD/TLT, has taken a long breather, and corrected back to the 200MDA.

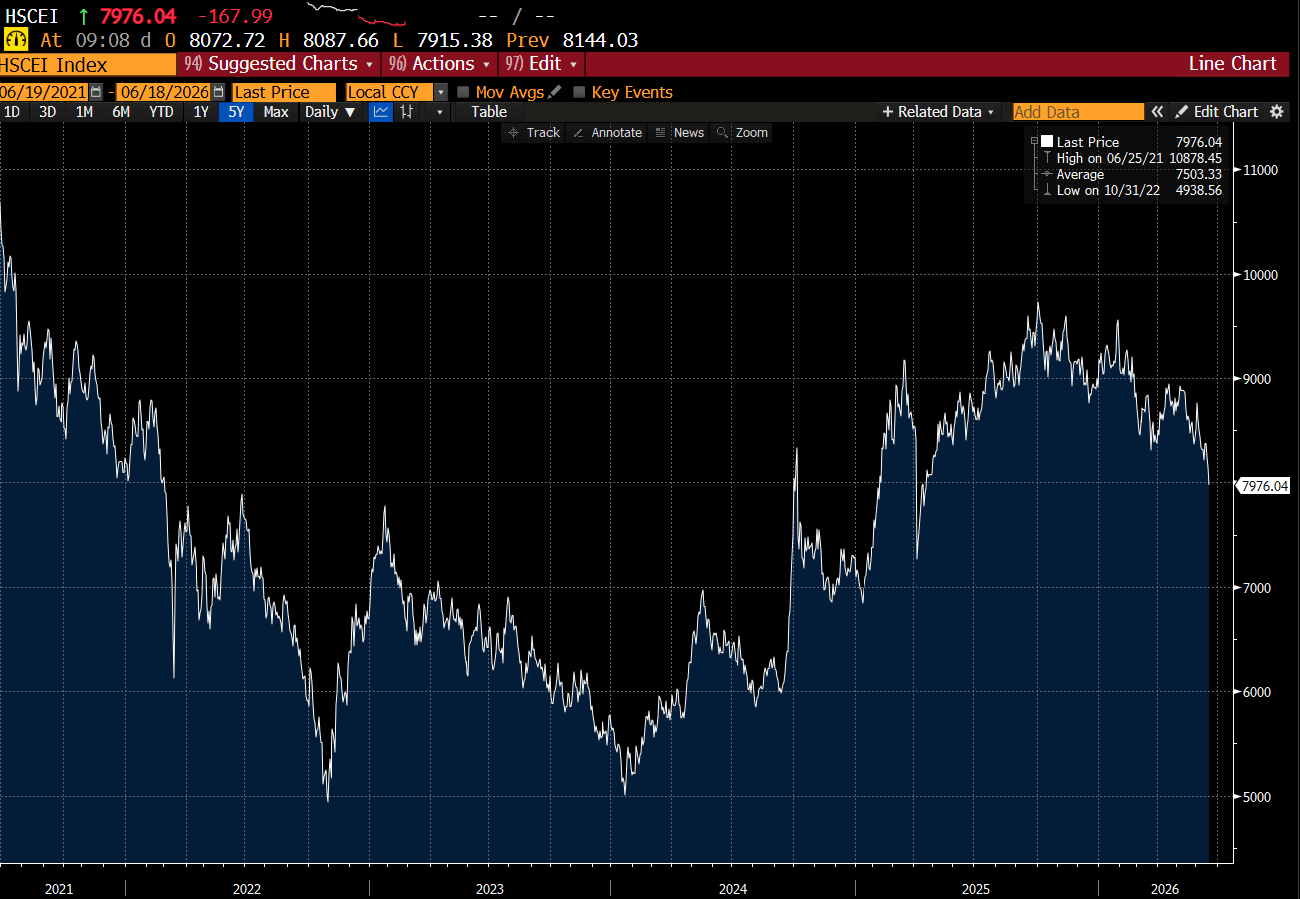

While I have been tempted to buy China shares from time to time, the politics has been ugly for China, and I would consider it more a “trading market”. This has been borne out this year. Bullish calls on China from the macro space has proved premature again.

While I was bullish on European defence stocks for a while, there were signs of the capacity build out being more than sufficient. Leading defence stock Rheinmetall has fallen some 41% this year.

One of the big positives I take from this year has been the primacy of politics over economics. And in general, inverting my investing process to take account of politics first has, I think, put me closer in tune with market moves. My current feeling on markets is that we are getting closer to a bearish washout - if purely to clean out the leverage that has built up in the system. I will discuss further in part II.