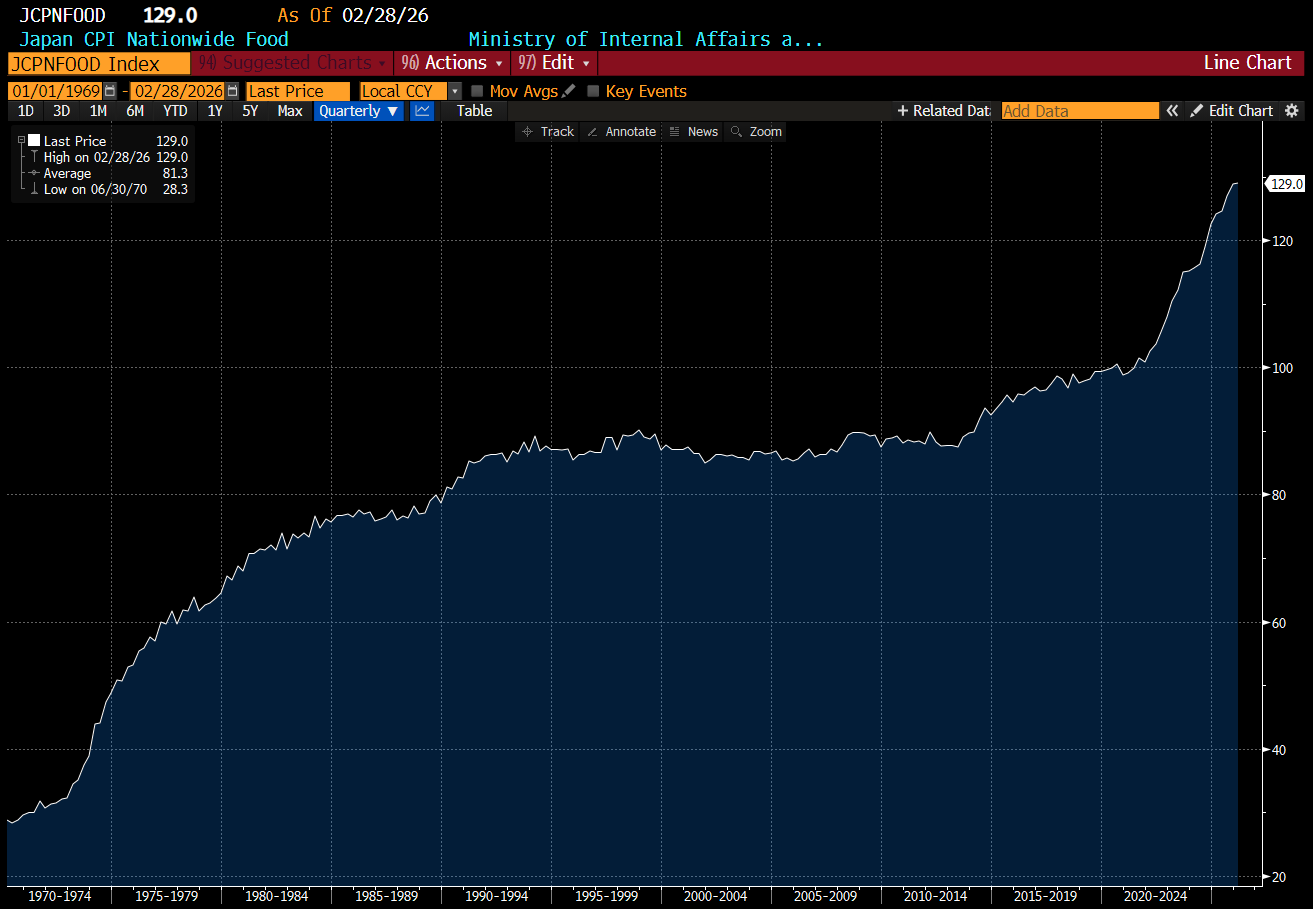

The say the key to happiness is low expectations. I thought my expectations of central bankers were low enough - and yet I still find myself unhappy with them. There have been many reasons for central banks to tighten monetary policy over the years - rampant asset prices (Bernanke would argue it better to cut rates to cause this outcome - moron), surging oil prices, rising wages, collapsing currencies (again Bernanke thinking is a falling currency is a good thing - moron). So market thinking is that no matter what, central banks will want to cut rates it they get the chance. And it is hard to disagree with market thinking - central bankers are a pretty sad bunch of losers. But there is one think that does seem to wake this group of bureaucrats from their slumber - food inflation. If we take Japan, a nation that introduced the world to QE and ZIRP, it had no food inflation for nearly 20 years, but is now dealing with severe food inflation.

The BOJ has responded to this inflation push with the higher interest rates since the early 1990s - although overnight rates are barely 0.7%.

And the 30 year JGB market has correctly noted, this is not enough. Rising food prices guarantees rising wages, which guarantees rising inflation. You don’t need a PhD from MIT to understand this.

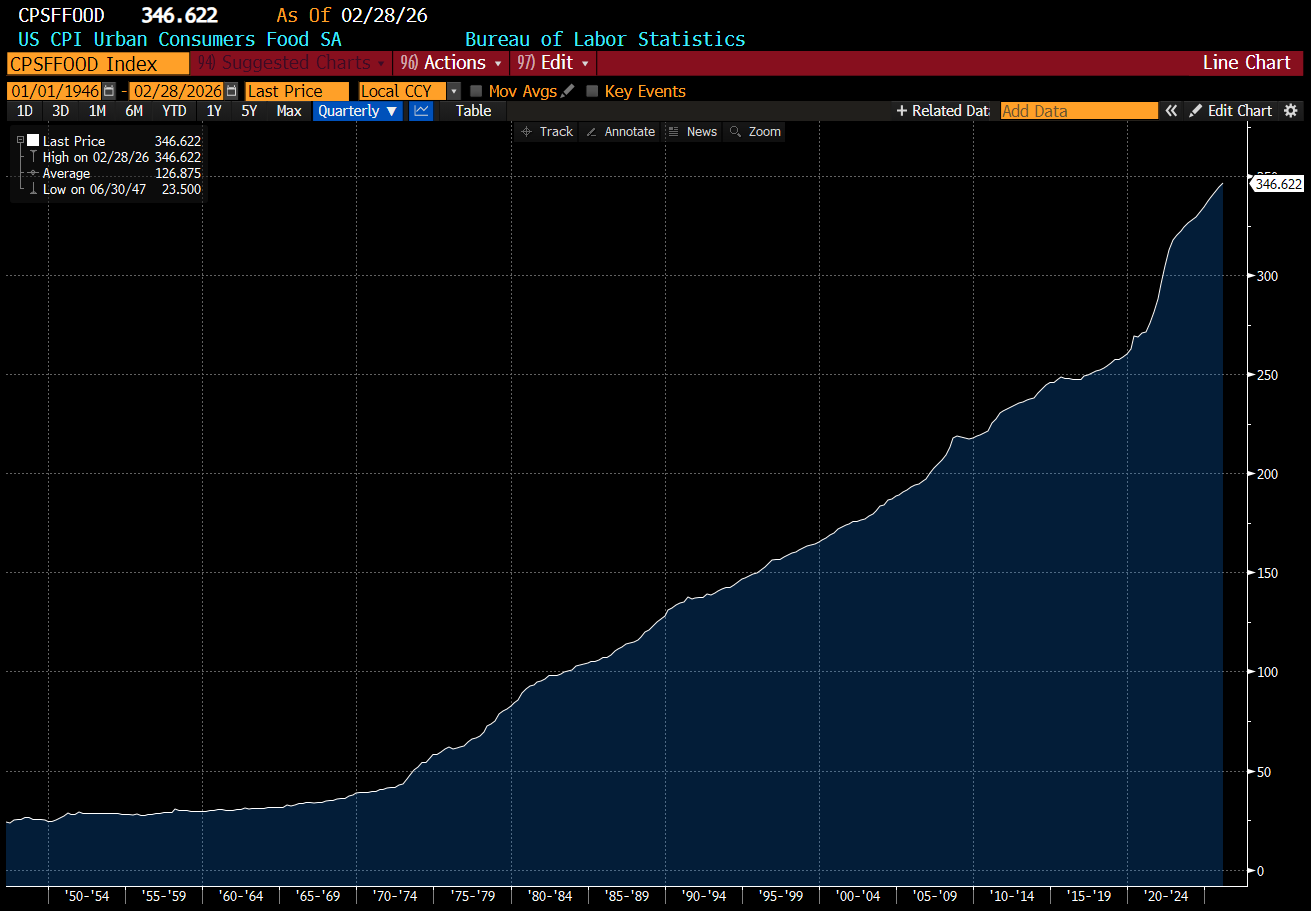

If that is the Japan story - the US is even more egregious. Unlike Japan, the US has never had stable or falling food prices since leaving the gold standard - except briefly after the GFC. Or in other words, QE and ZIRP never made any sense in the US - except to the deranged mind of Ben Bernanke.

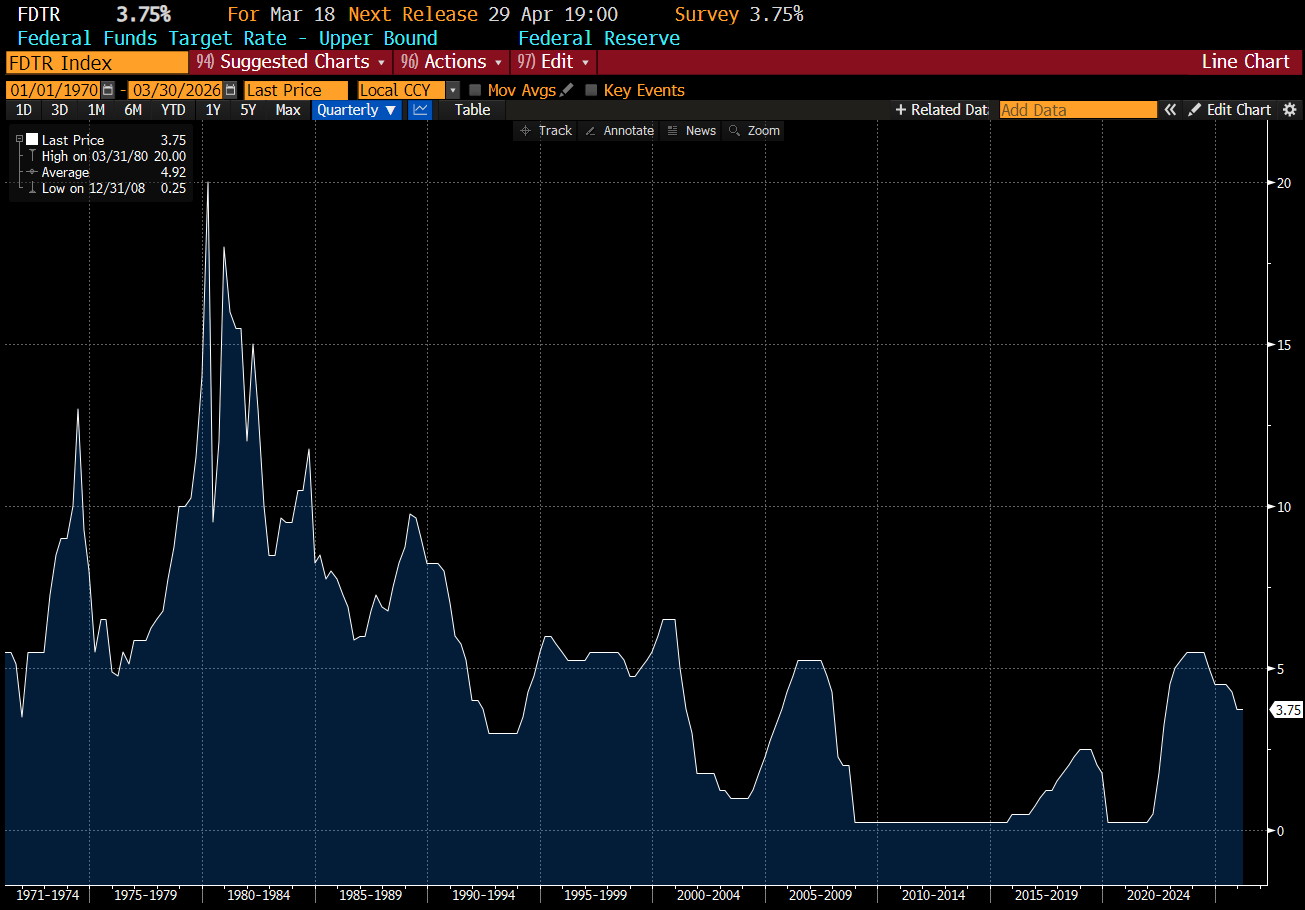

Even with my low expectations of the Federal Reserve, I have been surprised at the keenness to cut interest rates.

A lot of my surprise of central bank dovishness stems from the fact that agricultural commodities, which have deflationary trends, have not fallen like they did during the 1980s and 1990s, or in the 2010s. Agricultural commodities spiked in 2022, and have stayed high. For me, this would point to the need for much tighter monetary policy.

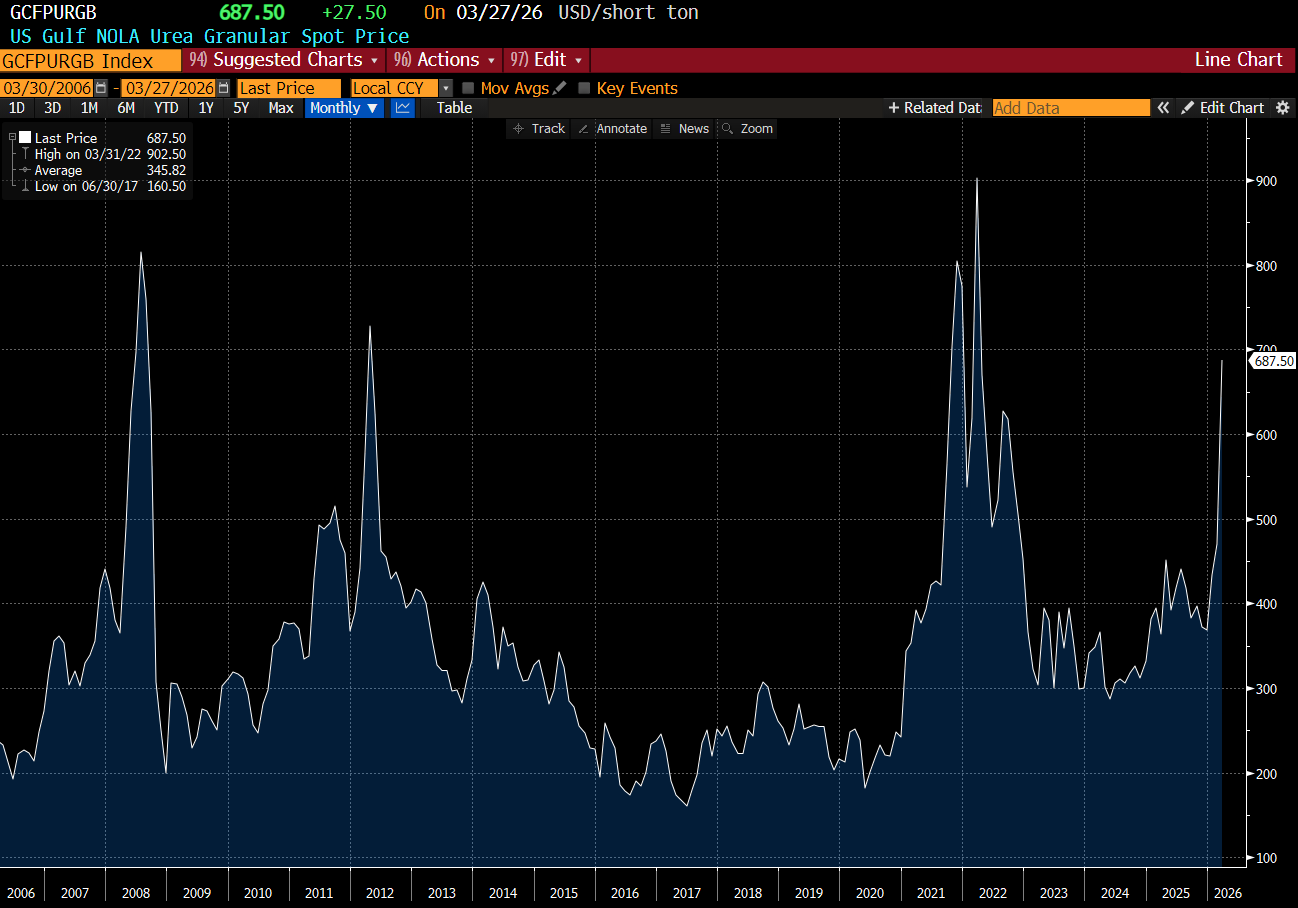

As many of my fellow substack writers have pointed out - closing the Strait of Hormuz does affect the price of fertiliser - namely Urea. US Urea prices are up a lot.

Even if there is some resolution to the Iran War, which remains my base case, it seems pretty apparent to me that ANOTHER round of food inflation is coming down the pipe. One thing about food inflation is that it directly feeds to rising wages. You can car pool or get the bus when oil prices are high - but when you have to cut back on food - people get angry. When we look at the US 2 year v the Fed Fund Rate, its starting to think the Fed might need to raise rates.

Best place to look might be the wheat market. The movement in wheat seems to offer a good guide to monetary policy. In simple terms, the 2 year yield moves above Fed fund rate when wheat is going up, and 2 year moves down when wheat is falling. Today wheat is going up.

Where urea prices are now, wheat looks like a buy. And if wheat is a buy, I would expect yields to rise. Will the Fed raises rates or not? Well I am going to lower my expectations further and assume they cut into a food price spike. That would be on a par with the uselessness of this institution since Ben Bernanke showed up. But if history is a guide, the bond market will not like this at all.