Unlike almost anyone else I know, my route to finance was via a currencies. I was working in HK in 1998, when the currency peg came under attack, and was fascinated by the way it affected interest rates and stock markets. I went back to university and wrote my thesis on private currencies (HK is last place in the world where private banks issue banknotes) and applied for a job at UBS. I then built a successful hedge fund business basically arbitraging currency risk via equities, and at the time I imagined the crowning glory was to be heavily short into a massive Chinese devaluation in 2016 - but this was not to be - and ever since currencies have traded in ways that they did not do previously. I will give some examples, and then go into how I think the riddle has been solved.

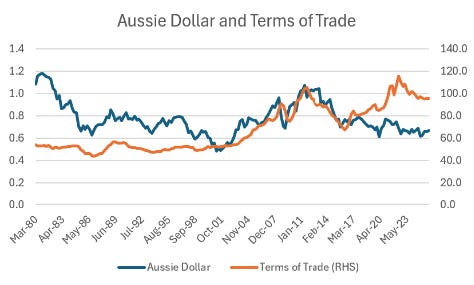

The Australian dollar used to follow its terms of trade pretty closely. Commodity prices up, Aussie dollar up. From 2016 this relationship has broken down.

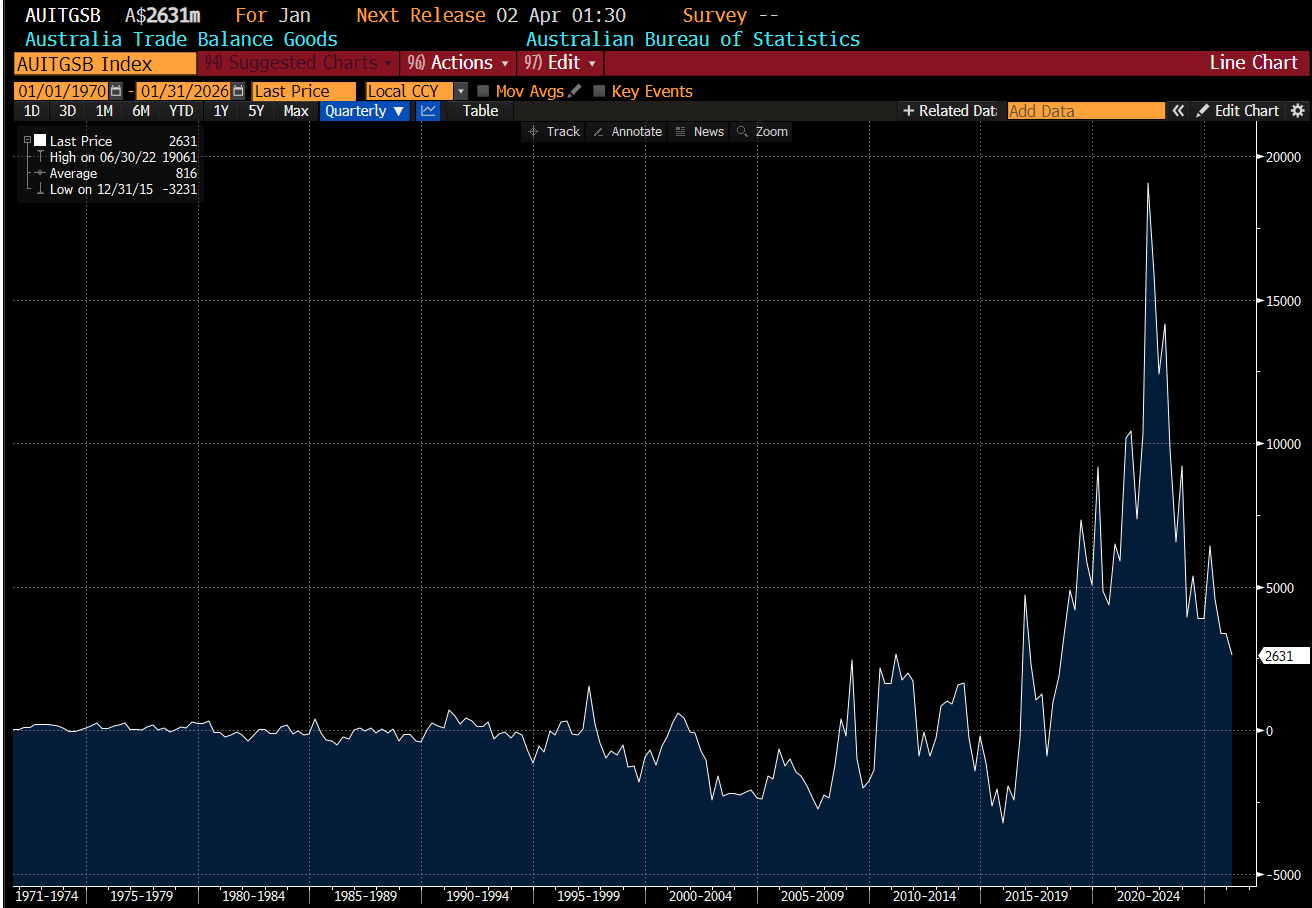

This breakdown between the currency and terms of trade led Australia to book huge trade surplus - something never really seen in Australia before.

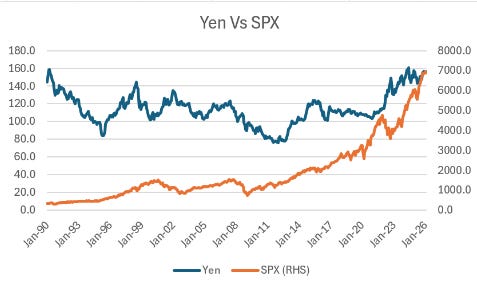

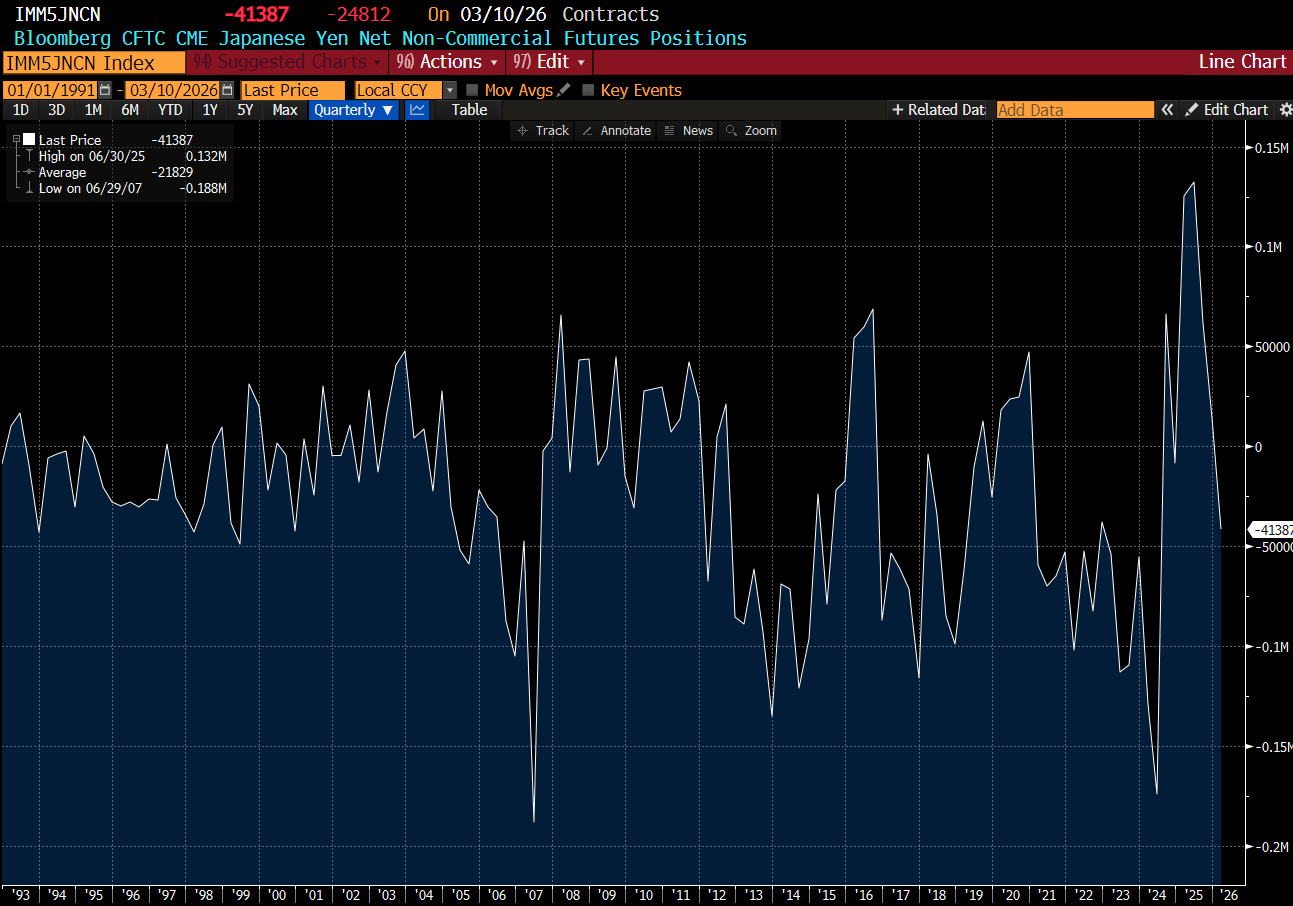

For many years, Yen was seen as a safe haven currency - doing well as when the S&P 500 was weak - but in 2022 it weakened ever as the S&P 500 fell.

The market was so convinced of this relationship, this led them to record long positions in Yen last last year, which has disappointed again. I refer to long Yen as the new widowmaker trade.

Korean Won used to be highly correlated to SOX Index (a measure that tracks the performance of semiconductor stocks), but in recent times Korean Won has weakened even as semiconductor shares have been on an astounding bull run.

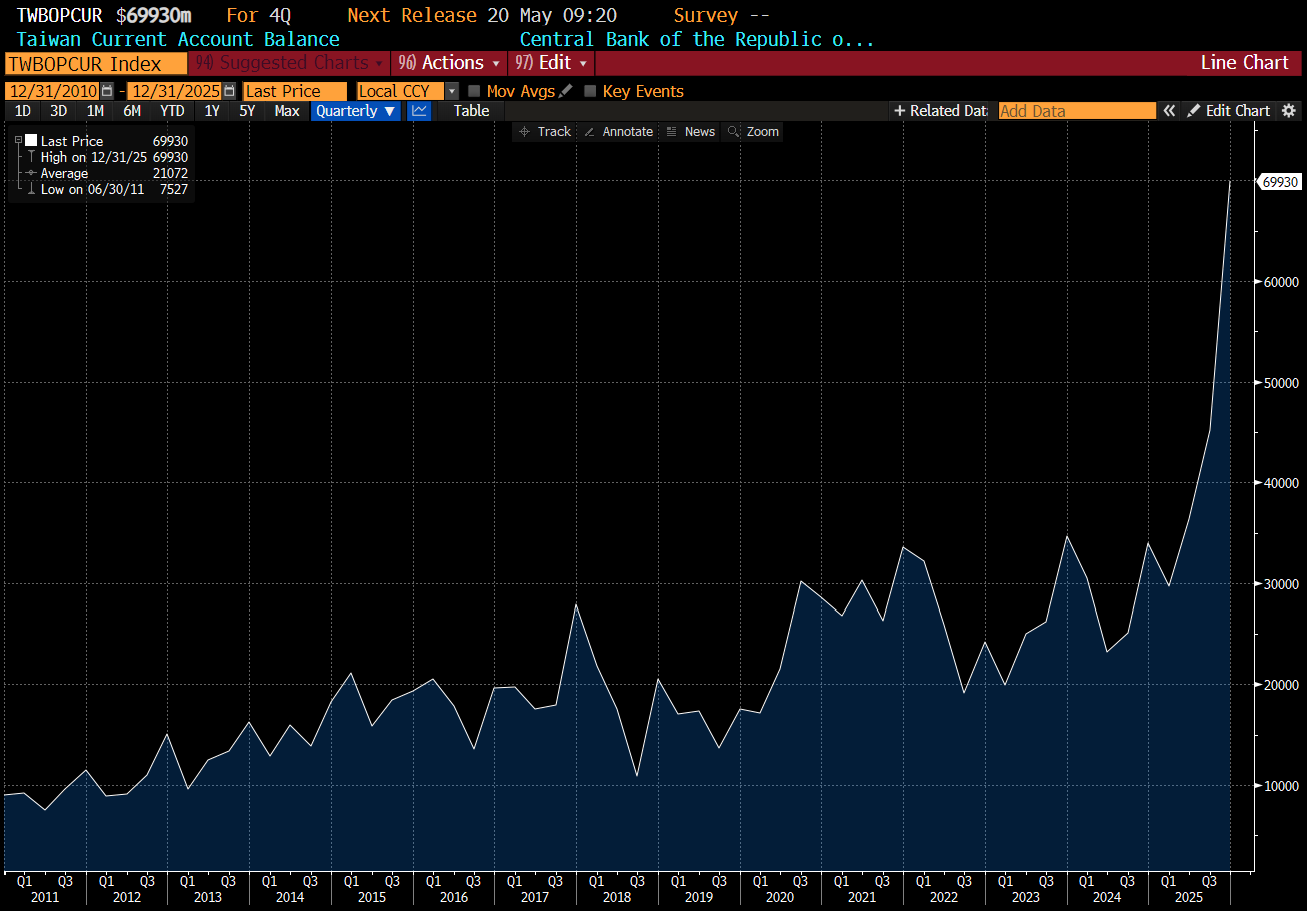

Similarly, Taiwan current account surplus has ballooned.

And yet the Taiwan dollar remains unmoved.

I have been brooding over the markets for the last few days. Something that always happens when I my hedges don’t work quite as expected. And I think I have an answer of sorts. I have previously described the period from 1980 to 2016, as a pro-capital era, when “globalisation” policies - free movement of capital, labour and technology did much to create pools of capital, and a broadly deflationary environment. Politically, was this a grand bargain between the West (Europe, Japan and the US) who were all major oil importers. They all agreed to disinflationary (pro-capital) policies to bring about lower oil prices. By the late 1970s, all three regions were large importers of oil, so politically this was possible.

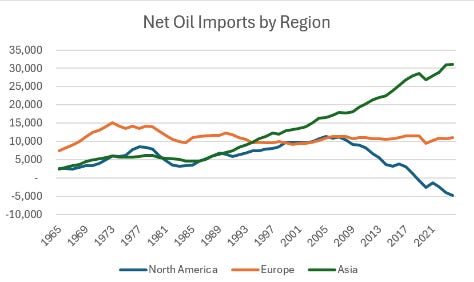

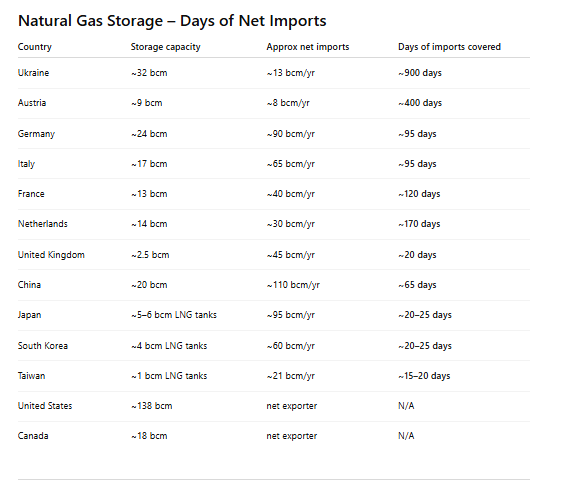

But around 2016, the US became energy exporter as shale production surged. Currencies stopped working the same way. If pro-capital globalisation policies were designed to give the US access to cheap energy but shale made cheap energy possible, then the US no long needed pro-capital policies, which is exactly where US politics has moved to. The problem, which the Iran War makes clear, is that while oil and natural gas prices are problem for the rest of the world, is it not such a big deal for the US. This is particularly true for natural gas. If you start thinking about currencies as a play on energy security - it gets very hard to be bullish on Yen, Won or Taiwanese Dollar. They are all exposed to natural gas supply issue.

This also answers another currency riddle - while Japanese Yen no longer acts as a safe haven - Switzerland does. Switzerland generates a substantial amount of energy from hydro electricity and nuclear power plants. The Swiss Franc has been very strong.

Thinking about currencies from an energy/geo political point of view also seems to work for currencies like Brazilian Real, which is now energy self sufficient. Historically this has not been a strong currency - but it has been surprisingly stable in recent years.

When I think about currencies politically - I see two outcomes coming. One is a bifurcation of the energy system - where Middle East and Russian output largely flows to China and India, while US and Australia output flows to Europe and American allies in Asia. The second is a huge focus on building domestic power sources - from renewables, batteries and nuclear. A secure energy system is now the route to wealth. Iran War makes this even more obvious. China probably leads most of its Asian peers in having a secure energy system - which probably explains why its currency is is much better shape than anyone else’s in the region.

This probably explains why the “weak dollar” trade has been such a bust. The big currencies like the Euro, Yen, Won and Pound have relatively poor energy security, making sustained dollar weakness difficult. But the relative lack of energy security in these nations probably also helps explain the strength of gold. Ultimately the implication is that Europe and East Asia need to launch huge investment programs to secure energy supply. Cost of capital should keep rising - but that does not mean the US dollar needs to fall.