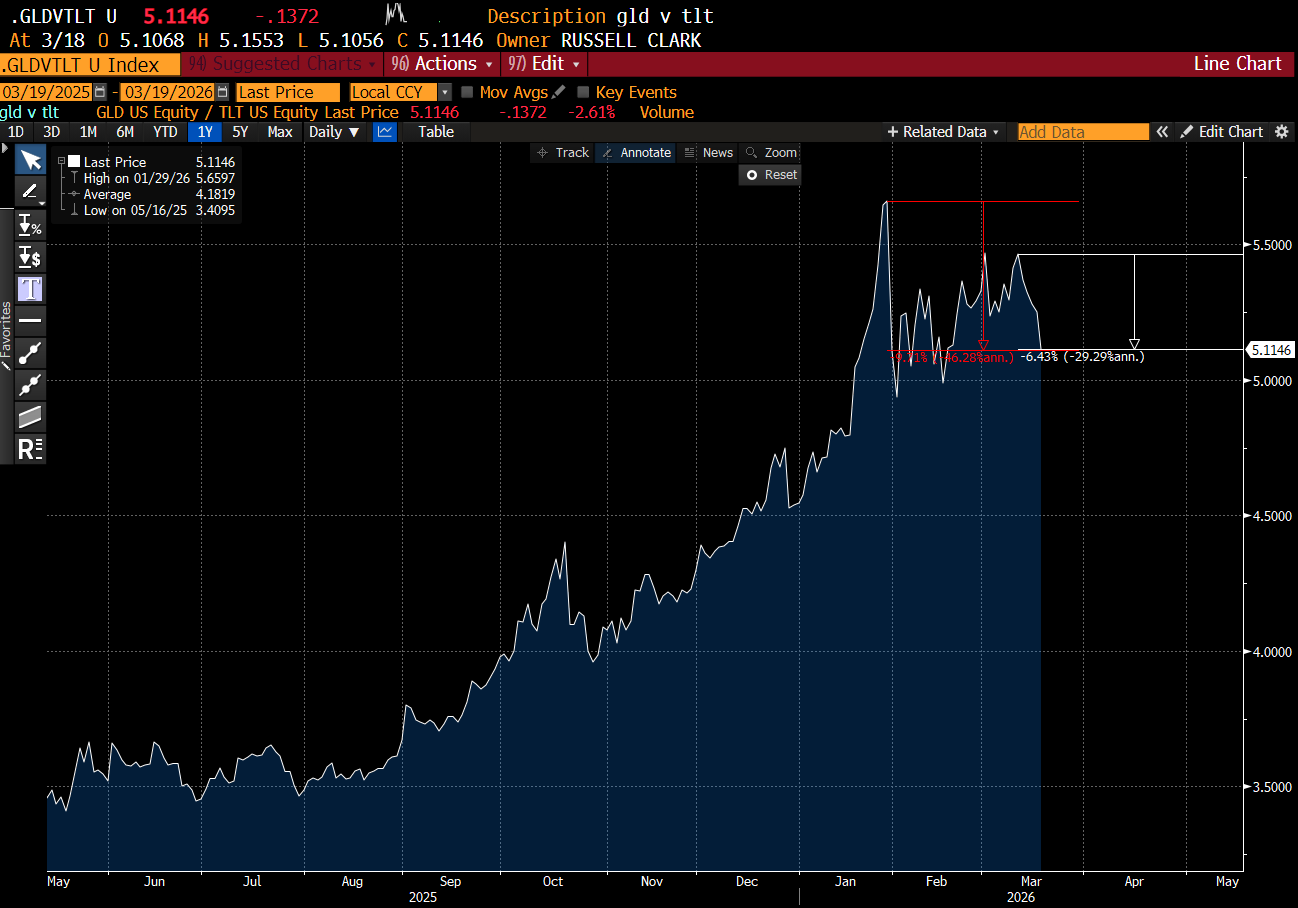

When I first started looking at the GLD/TLT trade, I really liked the long term graph. It suggest as some point a crisis would send gold to the moon, and treasuries into a tail spin. The peak in the late 1970s was around the time of the second oil shock.

Foolishly, I had assumed War in Iran, and a spike in oil prices would provide the same time of move. On the contrary, GLD/TLT is going to be down 9% this month when the US opens, and nearly 12% from the highs seen in January. I am surprised by this - and trying to work out what it means.

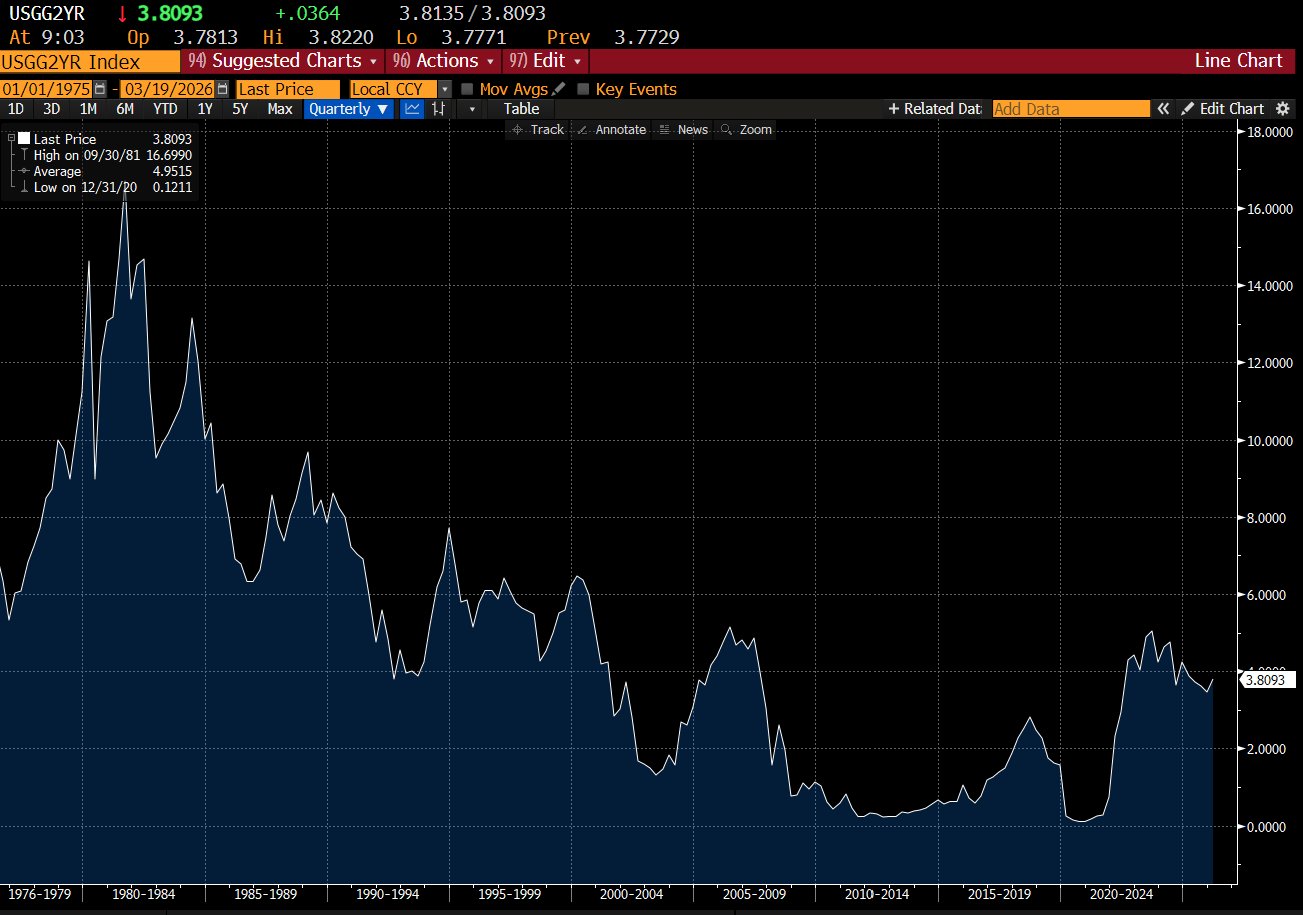

A weak gold price could make sense if short end bond yields in the US were soaring higher. They have had a pretty small move so far, and nothing like we were seeing in the late 1970s.

Maybe its just gold has done so well, it just needed a breather. And the shock of war meant that trend following funds de-gross which leads to gold selling. This is possible.

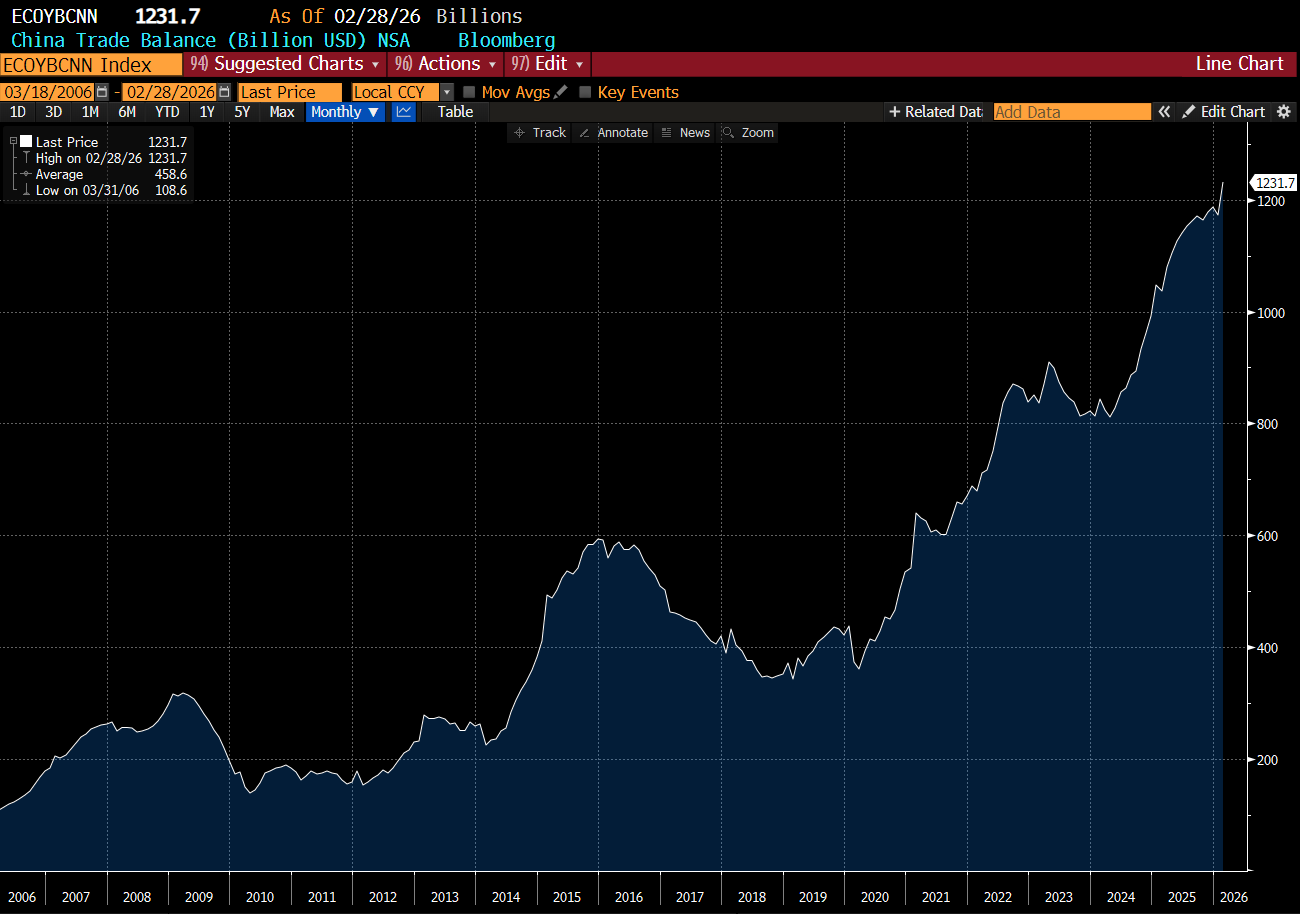

Another possible macro reason is that surging oil prices will reduce the buying power of China - that is it will cause its trade surplus to shrink - reducing the need for China to buy gold. The problem with that is back in 2022, spiking oil and gas prices did nothing much to reduce the trade surplus then. Energy prices would need to go much higher for this to come into play.

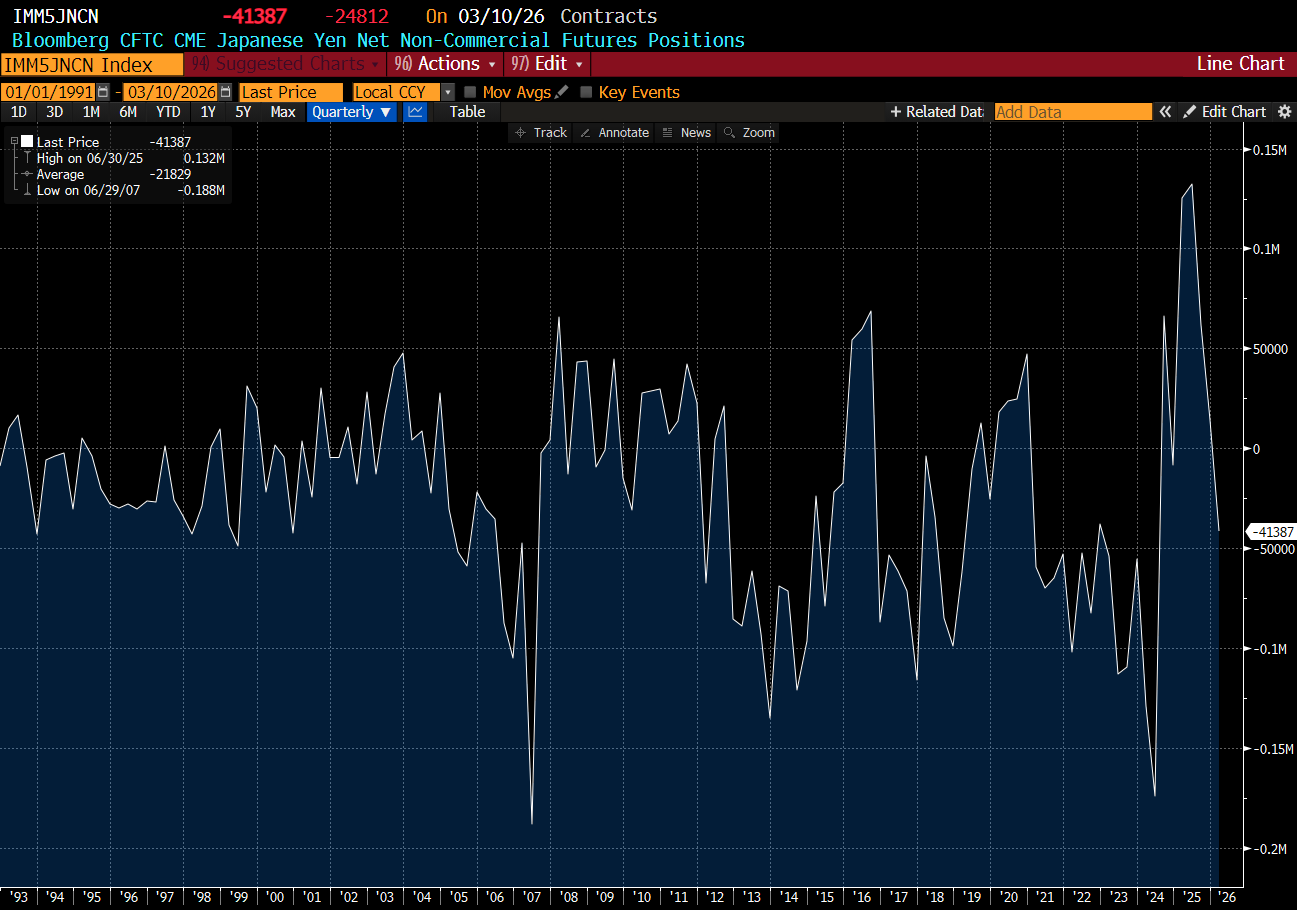

The best reason I can come up with for the failure of GLD/TLT to perform during the Iran War is that soaring energy prices have much obviously affected Europe and Japan more than the US, which has led to dollar strength. In 2025 and early 2026, short US dollar seemed like a slam dunk trade - with President Trump demanding it, and also attacking the Federal Reserve, this was a very popular trade. In mid 2025, according to CFTC data, the market had never been longer Yen than at that time.

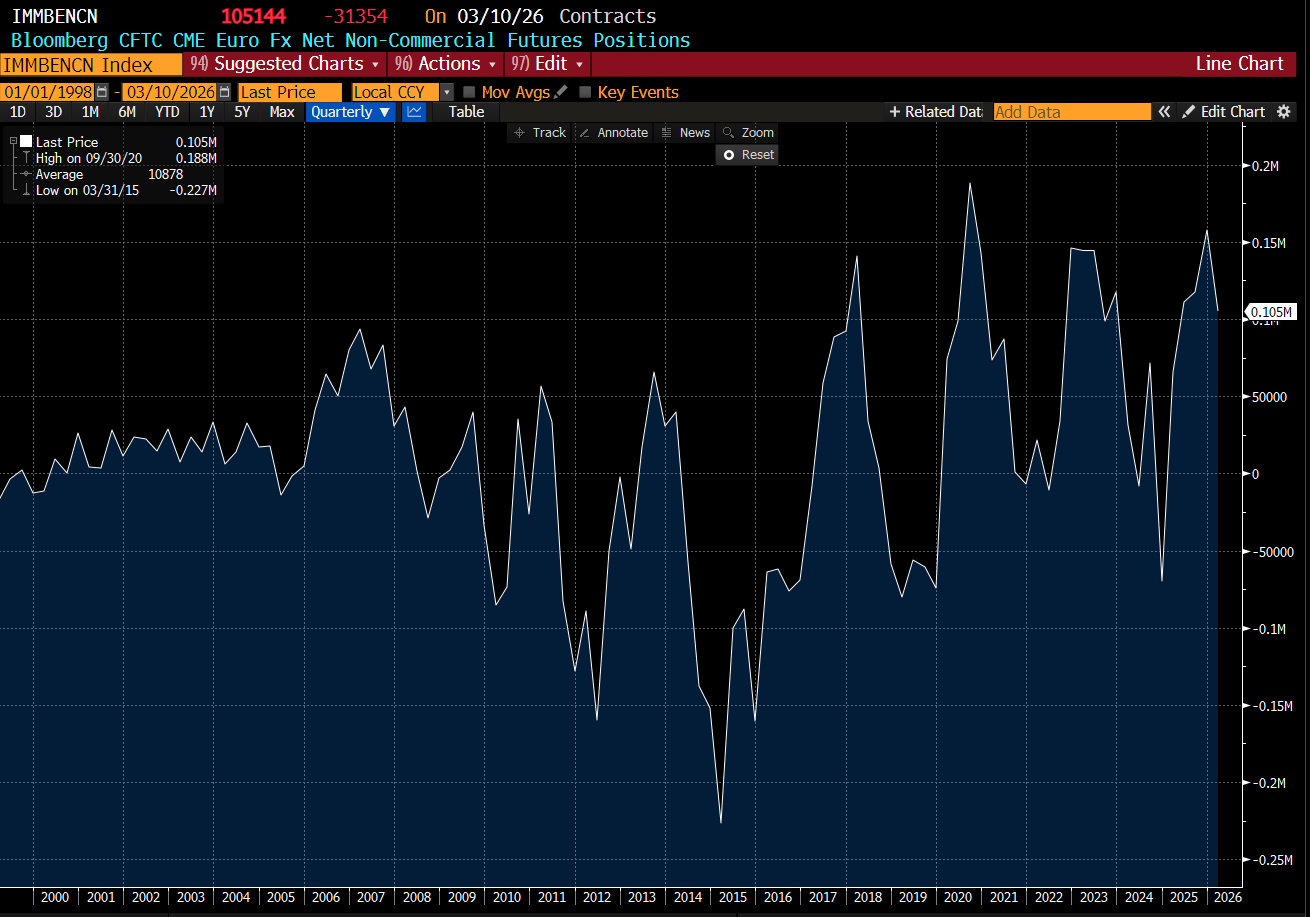

With the Euro, CFTC data still points to long position that has not washed out yet.

Most currency trades are a version of “tomorrow will look like today”, and with the Euro only just breaking through its 200MDA, trend following strategies will be selling Euro positions aggressively now. That is weak dollar trades will be getting replaced with strong dollar trades now - obviously bad for gold and other similar trades.

The big question is will 2026 look like 2022 when Russia turned off the taps? Tricky - as most of the middle East wants to sell its oil and gas, but they are being stopped by Iran. Back in 2022, both Russia and Europe knew the relationship was over. Is this going to be the same? Can Iran indefinitely stop the oil and gas trade? Politics would suggest not, but as the US and Israel kill more Iranian leaders, I wonder if their is still a political infrastructure than can actually cut a deal in Iran anymore. Against that, the temptation for a ceasefire, to cool prices and allow for a possible uprising in Iran must also be a factor in political calculations.

It is easy to see GLD/TLT as a weak dollar trade - although at its heart it is not - not the way I understand it. I see GLD/TLT as the breakdown of the US led economic system - and the Iran War seems very much in line with that. I also see it as governments willing to spend whatever it takes to keep growth going - which is a political observation - which I also think it correct.

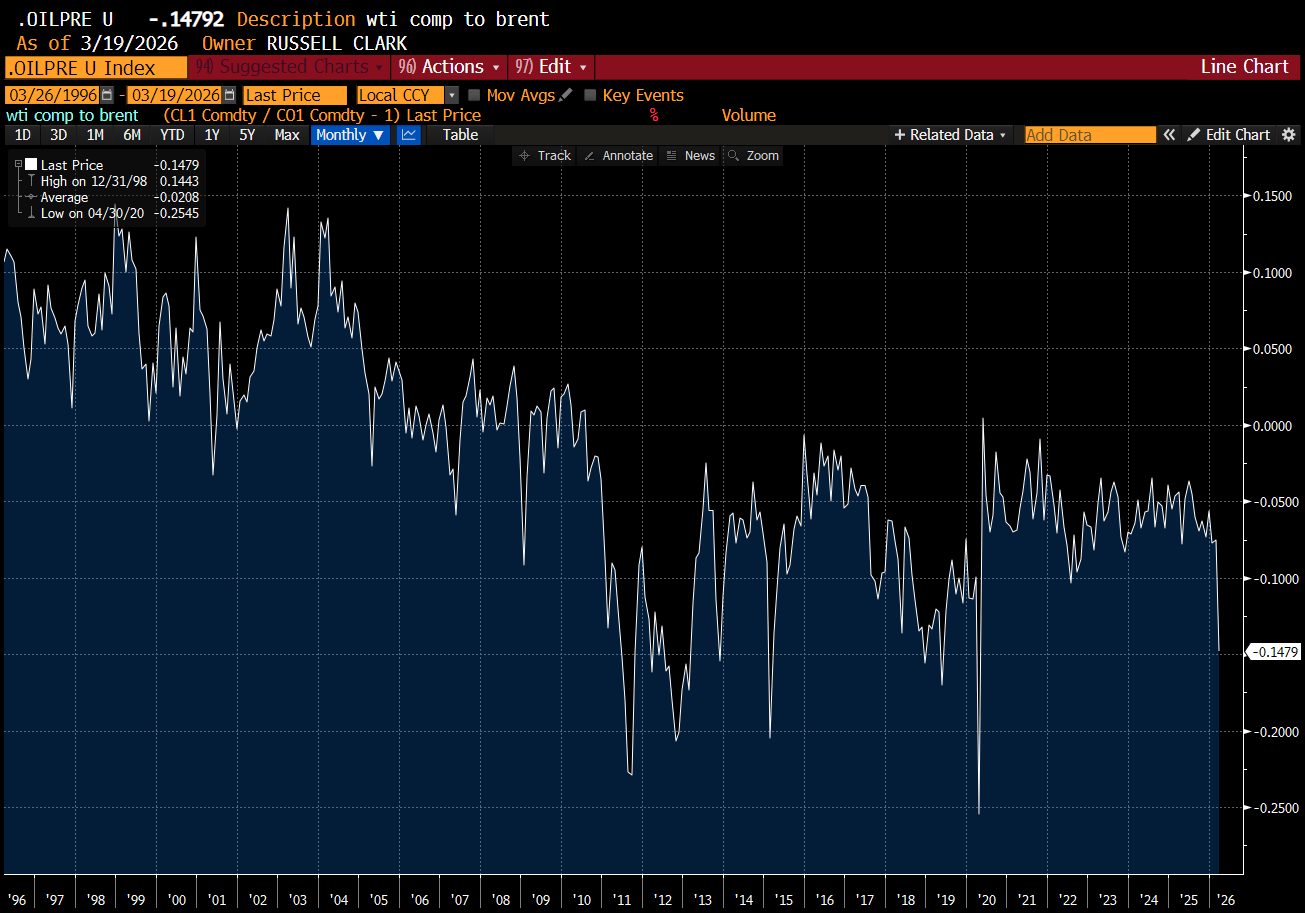

The more I think about the Iran War, the more I think we are heading for another huge macro economic change. Back when shale production started to get going, for decades US oil priced above Brent (European) oil. Below is a simple chart of the percentage difference between WTI and Brent - which now trades at a significant discount. This big macro change was a precursor to the political changes we have seen in the US.

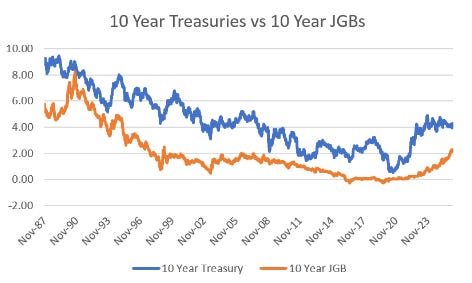

What the Iran War, the Ukraine War and the Liberation Day Tariffs has made clear is that the US will no longer act as a guarantor of energy, peace or trade. Obviously, the mainland US is unattackable, can survive on domestic trade alone, as it is energy self sufficient - so we (the rest of the world) are cast off to fend for ourselves. China is obviously by far the most self sufficient having never fully trusted the Americans, perhaps followed by the French. The defeated powers of World War II, Germany and Japan, are by far the most exposed, as politically they had no choice but to be vassal states. The big macro change that I think is coming is that German Bund yields and Japanese JGB yields need to price above US yields. Both nations cannot afford to not spend anymore - but to build, build, build. As above, the oil market gave a hint that change was coming, with spread between WTI and Brent falling between 2003 and 2009, before inverting, bond markets are also giving warning of such a change. JGB yields have been rising as US treasury yields have gone sideways.

With Japanese wages maybe one third of the US, a severe energy shortfall, a need to build out a defence capability and the need for data centre buildout, the outlook for Japanese inflation would seem to me to be far above that of the US, which is what bond markets are saying.

GLD/TLT is not working, in part because it was caught up in a weak dollar trade that the War in Iran has disrupted. But the politics of the War in Iran makes rising bond yields even more likely in my mind. But one of the ways I work is always to have two parts to any trade - Long Gold and Short Treasuries. I have had many clients over the years who always take the winning side of the trade (long gold in this case) and ignore the hedge (short Treasuries), because they just see it as a cost. But as I always say, the hedges are there for a reason!