Most, if not all, of my big thinking is based on watching the markets, and wondering why something you expect to happen does not happen, and what does that mean. In the earlier part of my career, I looked at JGBs, and wondered why they never sold off despite every major macro thinker being bearish on them. I made a career out of working out why JGBs were strong.

When JGBs did start to trade bearishly during COVID, I knew something had changed, so in the end I took a break to work out why that was, and then used those ideas to set up Brumby. A changing political view of the world let me to invest with the idea of GLD/TLT, and the rising cost of capital as the driving principals behind the fund. Exceptional performance of the fund has been in no small part driven by the exceptional performance of GLD/TLT. This month will likely see the first meaningful weakness in this trade since late 2023.

I have a strong incentive to brush off the weakness in GLD/TLT as positioning led. That is the oil shock has meant winning trades get sold to raise cash. The problem is that even if that was true, an oil shock really should be bullish for this trade, not bearish. And even now, three weeks into this shock, gold is still negative correlated to oil price.

I think the “problem” with this trade this month is that TLT is focused on the long end. The reality is that the cost of capital is rising again. The US 2 Year treasury yield has risen nearly 60bps in March so far.

The long end, where short TLT would make money, has moved a tamer 30bps - to be back where it was in January. If the 30 year had sold of 60bps, then the drop in GLD/TLT would have been far less precipitous.

What I am saying is that GLD/TLT worked, but the oil shock has been more pronounced in the short end rather than the long end, which means the short book has not made as much as the long book has lost this month. But I could also say, I over earned in the preceeding months, as short TLT did not hurt me as much as it would have if has been short the shorter end of the Treasury market.

So where to from here? What this whole episode has made clear is that European and Asian allies of the US need to spend, and spend aggressively. Japanese and German inflation outlooks (to me) are much much higher than the US, and yet their bond yields are below US yields.

This of course reflects the much more savings focus of European and Asian investors, but the market knows this as well. I have bored people with JGB graphs for years, so will use the German 30 year graph to tell the same story. It is at cycle highs.

Everywhere I look, the demand for capital is rising. AI investing, energy investing, defence spending. The cost of capital is rising. And this has become apparent in problems with private credit. When capital was free, no problem. But put a cost on that capital, and its not so great.

The temptation and advice I get from markets is that short Europe and Japan as a trade on higher energy costs. I feel like this is foolish. The time to short is when people DO NOT know they have a problem. Once a problem is known, its normally better to be long. It contrary to human instinct, but very typical of human experience.

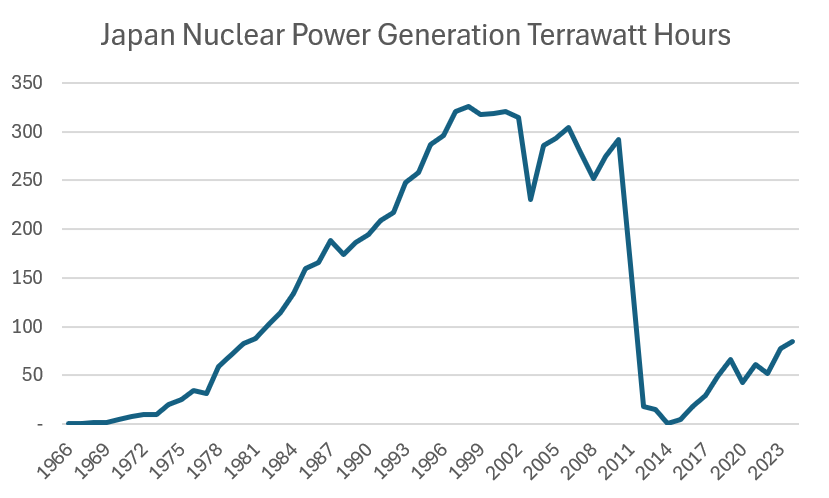

Japan knows it has an energy problem. Japan closed down most of it nuclear power after Fukushima in 2011. This is when its problems began. But Japan has come to realise this is creating an energy insecurity problem, and is trying to switch is back on. Japan probably will not get back to is 1993 highs, but maybe 200 Terrawatt hours.

What is curious about this chart, is an energy secure Japan used to have a strong yen, and energy insecure Japan now has a weak yen. If Japan gains energy security again should we expect a strong Yen?

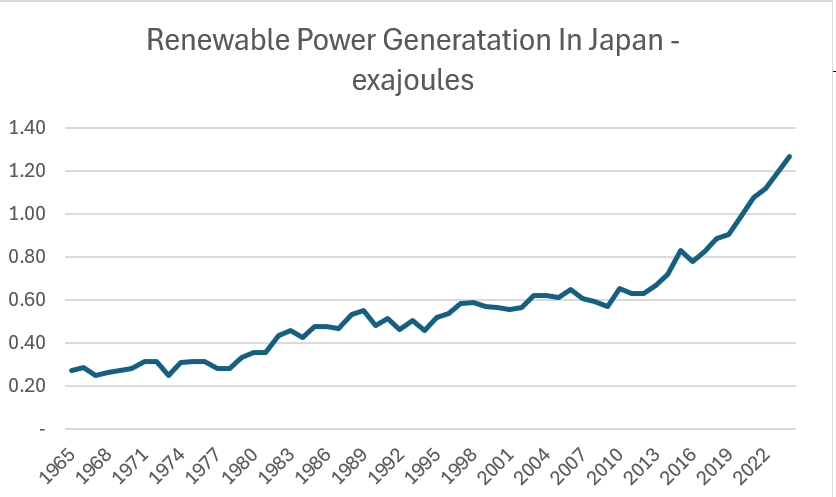

Japan has been slow to restore nuclear energy, for understandable reasons, but the direction is clear. And as we are all aware, renewable energy is also much more feasible than it used to be. The step change from 2022 is obvious. This equates to about half of peak nuclear generation.

In reality, I am turning more bearish on fossil fuel. Once you weaponize it, you reduce demand for it. This is the same argument for gold over treasuries - once you weaponize US payment systems, you naturally kill demand over time. All of this may seem overtly political to you - particularly for a fund manager. But as we should all know now, politics is everything. Politics makes me think GLD/TLT is still good, and its makes me think the relative outperformance of the rest of the world versus the US is likely to continue. Why? Well I suspect energy security will return to Asia and Europe, but at the cost of a rising cost of capital. And a rising cost of capital should be bearish for the US. Or in other words, I am long Japan, which knows it has a problem, and short the US, which is oblivious to its future problems.