Soros was always the fund manager that I tried to emulate. For me, his mastery of currencies, interest rates and bonds was much closer to how I thought about the world than Buffett. Whenever I took a close look at Buffett, I had to admit he was a good stock picker, but an even better business operator. I preferred the Soros style as it fitted in with my ethos that government policy can be largely ignored. Classic examples of this were the various currency devaluations of the 1990s, where Soros really made his name, most famously the Sterling devaluation of 1992.

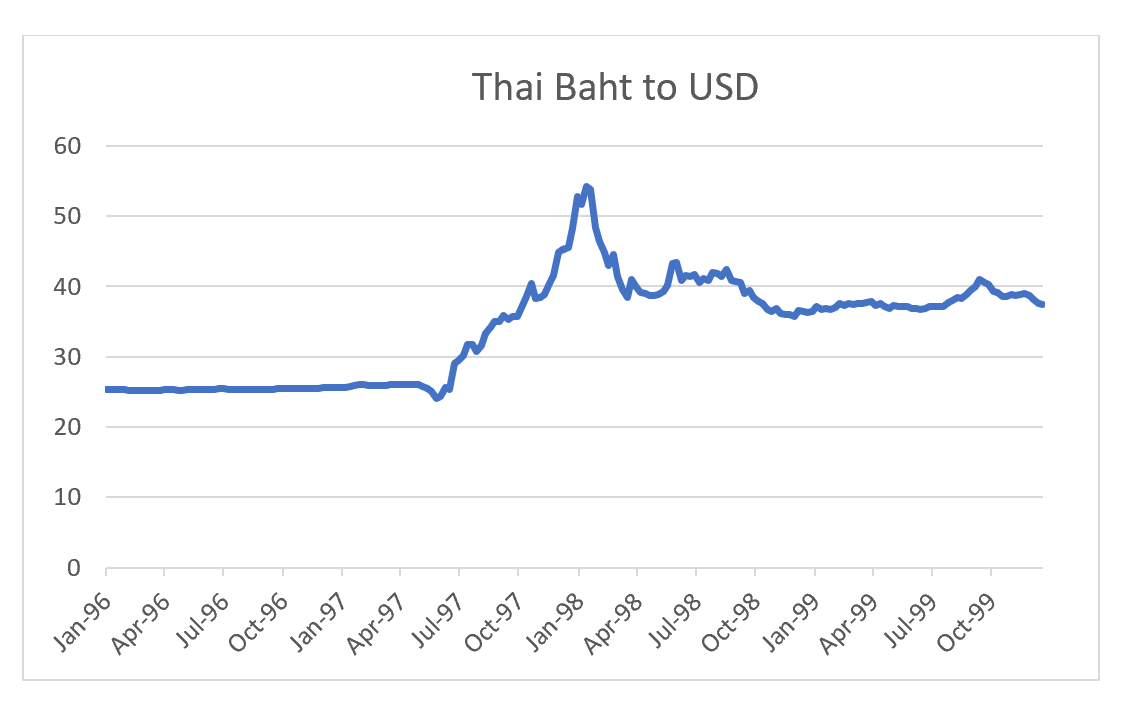

Soros was often name checked in various Asian currency devaluations in 1998 as well, starting with Thai baht in 1997. I was living in HK in 1998 during the failed speculative attack on the Hong Kong Dollar, and the episode sparked my interest in finance, and set me on finance track ever since.

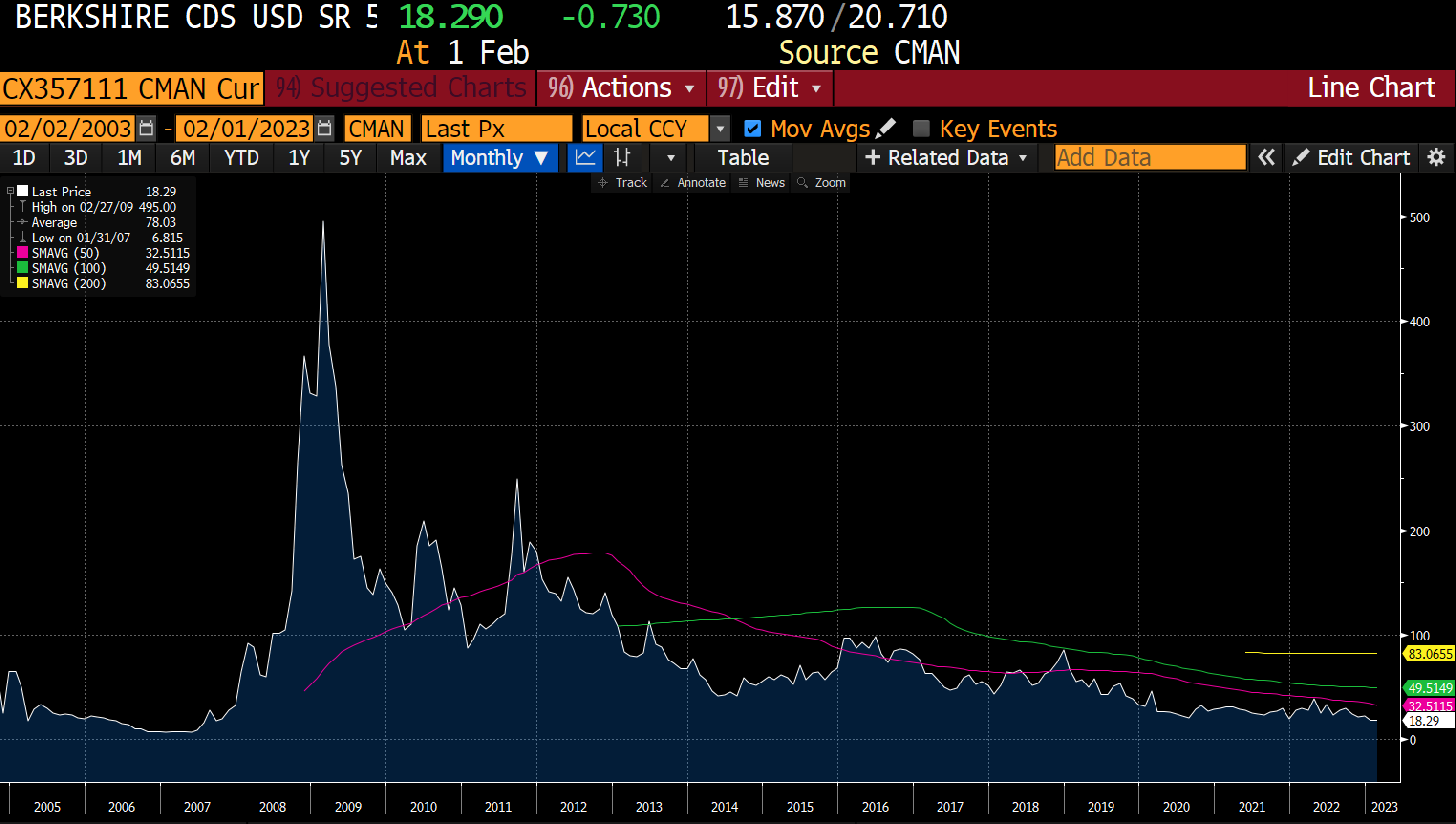

These days it would seem weird to most finance people to say that I knew about Li Ka-Shing and George Soros before I knew anything about Warren Buffett. The first time I started to think about Berkshire Hathaway and Warren Buffett in detail was during the GFC, when like most financials its CDS began to blow out. I wondered at his confidence that the US would recover, when the experience of Japan after its financial crisis in 1990s took nearly 30 years to recover, and land values still down 90% from the peak. From my perspective, Soros broke governments, while Buffett got bailouts from governments - which made Soros a far better investor in my mind, and a better one to emulate.

Starting out in Asia and emerging markets, currency fluctuations make a huge difference to returns, which led me to study Soros style techniques. Over the last ten years I have been looking much more closely at the US, and looking much more closely at Warren Buffett style investing. Many investors claim to be Buffet style investors, looking for value stocks with a large moat to protect margins. And yet very few seem to achieve the same returns. What I have learned from looking at Buffett investment style is that he has learnt to invest alongside US government policy. Knowing that he is the son of a four term congressman, made adding US government policy into his investment decisions a much easier to assumption to make. When I go back and look at the investment decisions that I am familiar with, all have a view of current US policy in mind. Buffett had a large investment in Petrochina, held from 2003 to 2007. In 2001, with US approval, China had joined WTO. US oil production was falling, and Chinese demand was rising, all leading to a perfect macro and political environment. By 2007, shale drilling was already leading to a changing oil industry, and the political environment was less supportive.

After selling Petrochina, Buffett took a position in BYD in 2008 which at the time was a lithium battery maker, with plans of entering the car market. Both the battery business and the auto business seemed to me businesses with limited “moats”, at least in the way I understood it. And for many years the stock when sideways, but in 2020, government policy in the US and China went extremely pro-electric cars. Buffett is now selling down the position.

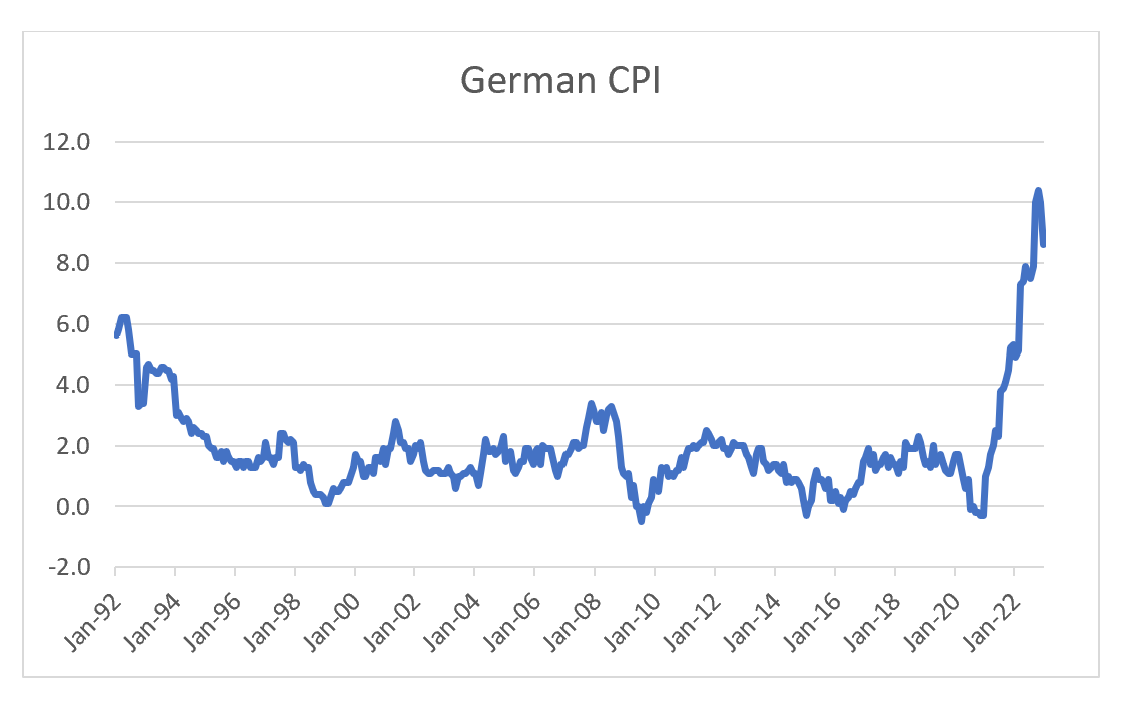

So how do long term equity bets by Buffett match up with Soros currency trades? Well US left a fixed exchange rate under Nixon, and then under Reagan was keen to move to a free floating exchange system. But politically, the big change was that devaluation was not seen a negatively before. Analysis of the depression led economists to label currency devaluation as “beggar thy neighbour” policies, and political pressure was applied to not devalue. When we look back at the the most famous Soros trade of all time, the breaking of the pound, politically this trade needed the support of the Germans. Specifically, he needed to Bundesbank to not cut interest rates to make it easier for the UK to maintain the exchange rate. At the time, a post unification boom in Germany meant that inflation was running at 6%, and so the German had no political interest in cutting rates to help out the Brits.

The failure of Eurozone to fall apart after the Eurocrisis can probably be linked to the fact that low inflation has allowed monetary policy to be very supportive. That is why very high inflation in Germany now makes investing in European assets very tricky.

Likewise with the Thai Baht trade, you needed to be sure the Federal Reserve was not going to cut rates for that trade to suffer. The period from 1994 through to 2000 was notable for the Federal Reserve keeping interest rates high (by modern standards).

Or what I am trying to say, is that politics is very important in both macro and equity investing, and both Soros and Buffett are masters of politics. There are two reasons I am talking about this. First the politics of pro labour policies are inflationary, which means capital destructive moves are more likely. This has been an underlying message of my research for awhile. Secondly and more interestingly, is that I am seeing a mega trade where the politics is lining up to be very supportive. I quite like it as Buffett is already making investments the market is not really pricing in the potential yet. I will talk about it more in a future presentation. But hopefully you can see that both Buffett and Soros benefitted massively by following US policy, but by trading different aspects of it. Investing in line with government policy is now what I plan to do with all my ideas, which happily enough is in line with my pro-labour over pro-capital ideas.