My observation on markets is that since 2016 onwards they have traded very differently to the past. Prior to 2016, I found that currencies, commodities, bonds and equities would trade in line with each other. Hence, if I had a strong view on any one of those asset classes, it would also inform my view on all the other asset classes. Furthermore, if the various asset classes starting trading disparately, it would be sign to be more cautious on my view. For many years, I wondered why this relationship broke down, with reasons ranging from central bank interference, to the invention of shale drilling and energy independence for the US. However, I now think the primary reason was regulatory reform that moved central clearinghouses to the centre of market pricing.

In financial terms, the dominant market pricing model when banks where the main clearinghouses was a Value at Risk (VAR) model. As risk started to increase, or was perceived to be rising, banks would cut their own risk exposure, and their exposure to other banks. This was forward looking, and also caused problems in one area to quickly cause risk to be pulled from all areas.

However, the new model, which uses initial margins is set by clearinghouses, who take no position in the market, but set pricing according to historic price action and liquidity. What this has meant in practice, is that risk is not repriced instantaneously through markets, but often with a lag. Tech offers a good example. Softbank is the largest VC investor in the world. It was also the premier Japanese dot com bubble stock back in 1999. As can be seen Softbank fell by nearly 50% in 2021, while Nasdaq continued to rise substantially. That is the risk that was being priced in Softbank was not being priced into Nasdaq. For an old trader like me, this makes me wonder if Softbank a buy, or is Nasdaq a short? This uncertainty made it difficult to hold any position.

My ongoing series on clearinghouses gives me the mechanics of understanding how this change in pricing system works. For those interested, I recommend becoming a paid subscriber just for the next month (£35) as I have at least another 4 posts on clearinghouses coming out describing in detail the problems with their risk pricing models. This will also encourage me to keep researching this area.

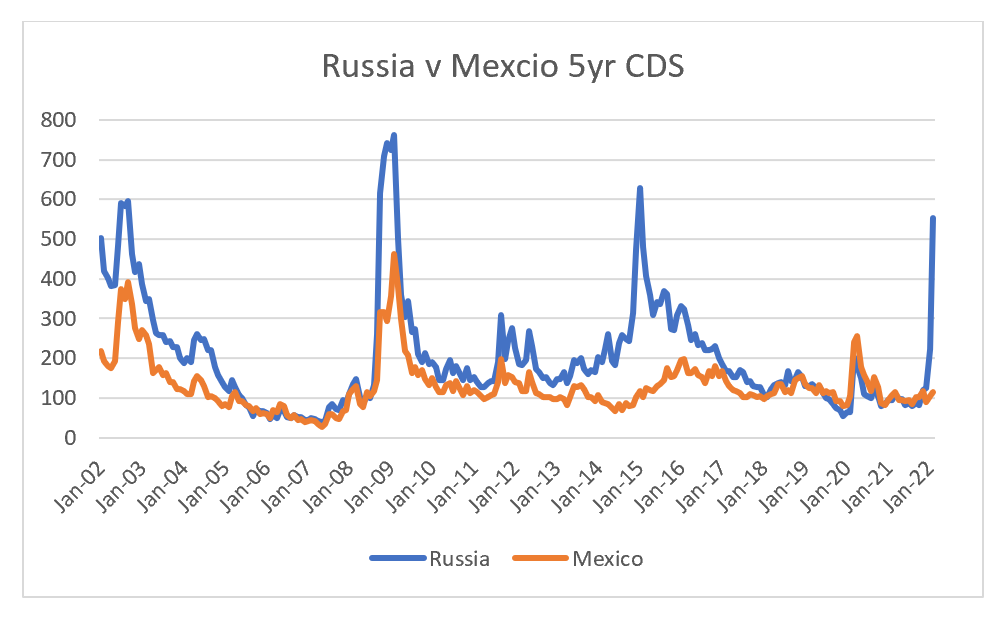

One very clear example of how risk pricing has changed from a forward looking model to a backward looking model is provided by Russia. Russia/Ukrainian issues first came to a head in 2014 coinciding with the Maidan Revolution. If we look at the CDS of Russia and Mexico, both commodity exporting nations with a chequered financial history, we can see that Russian CDS began to widen versus Mexico before the annexation of Crimea. That is markets were forward looking and already adjusting risk. However in 2022, despite the massing of troops on the border, Russian CDS failed to signal any risk, until the actual event happened.

What does that mean for markets today? Well in the US, before almost every bear market and recession, we have seen a spike in mortgage rates and a spike in oil prices.

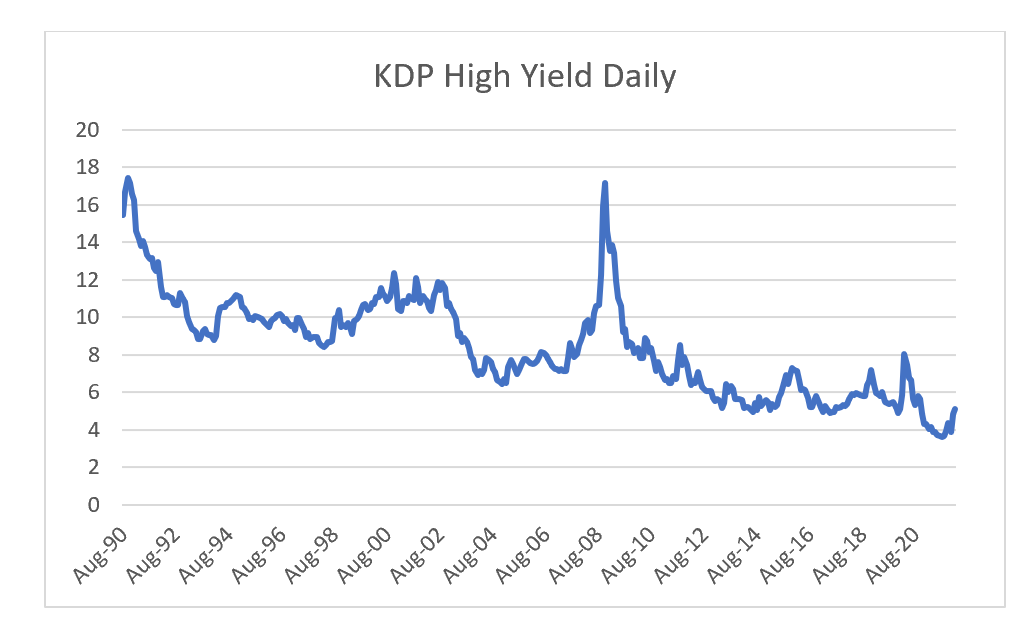

Normally, such negative moves would lead to weakness in corporate credit markets - but so far high yield is at levels still associated with bull markets.

High yield reminds me of Russian CDS, being priced of the experience of the last ten years, but missing the forward looking view of rising energy prices and mortgage rates. The clearinghouse model, with its backward looking pricing allows us to observe changes before it gets priced in. Markets will likely work out this mispricing soon, so in my view now is the time to short.